Credit investors are pricing this company to be a casualty of retail armageddon, TRUE uniform earning power data says this may present an opportunity

The bond market has consistently been overly pessimistic about this company’s outlook, pricing it for its business to be wiped out.

Recently, as-reported metrics appear to confirm that pessimism, but TRUE uniform UAFRS-based cash flow analysis shows the company’s situation is not nearly as concerning as GAAP accounting would have investors believe.

Below, we show how Uniform Accounting restates financials for a clearer credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company…

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

In fiscal 2016, GameStop reached its highest ever Uniform Gross Earnings: over $1 billion. The company had consolidated the video game retail market, and was starting to diversify from solely video games to phone distribution in the face of the wave of gaming offerings coming out for iPhones and other smartphones. It was also starting to offer digital download offerings to customers to defend against online competitors.

Contrary to as-reported P/E, which made the company look like it was trading at historically cheap P/E, at 7x, Uniform P/E highlighted the market was growing bullish on GameStop. GameStop was trading at a historically high 14.7x. It hadn’t traded at these levels since 2008.

However, the company’s 2021 bonds, due 5 years out, were trading with an over 7% yield to worst. The average high-yield bond at the time was trading at around a 4% yield to worst, for context. Creditors were pricing this company for a decent amount of distress.

It’s often said that equity investors are focused on upside, on what a company is going to do, and the opportunity a company has for growth. Equity investors generally default to optimism.

On the flip side, credit investors are viewed as not focused on opportunity. Credit investors are generally risk focused. They’re not thinking about how the company’s cash flows could multiply, but rather how they could vanish and the creditors could be left holding the bill.

Equity investors were looking at GameStop and saying it was successfully navigating the challenges in the industry. It was diversifying its revenue base. It was also directly responding to the digital alternatives like Steam, Xbox Live, PlaysStation Network, and Nintendo eShop for game sales with its new solutions.

Equity investors saw a company that was seeing a short-term dip in profitability, but potential for fundamentals to reaccelerate. They were focused on the optimistic outlook.

Credit investors saw a company that was about to be disintermediated. The gaming platforms were offering direct sales to customers, disrupting GameStop’s used and new gaming platform. Steam was offering the same for PC gamers. And GameStop’s digital add-on solution was cumbersome.

GameStop’s collapse was imminent according to creditors.

But Uniform Accounting credit analysis highlighted something very different. Seeing through the accounting noise, even if GameStop had some cash flow weakness, thanks to their forecast cash build, and significant cash flow buffer over obligations, there was no reason for the company’s bonds to trade at such pessimistic levels.

Creditors quickly realized that while GameStop did have competitive headwinds, the company wasn’t an imminent risk. By late 2017, the 2021 bonds had dropped from a 7% yield to a 5% yield, as the credit markets realized the company’s real cash flow and obligation profile gave them room before any decline threatened the company.

But the issues the market was spooked about for GameStop had only gotten worse since. Both Uniform and as-reported ROA have dropped significantly since 2016 as those online offerings have continued to assault GameStop’s legacy business.

Credit investors appear to have had their worst fears confirmed in 2019. In 2019, the company’s earnings dropped from basically $0 in 2018 to -$670 million. The competitive pressures had finally caught up to GameStop.

But once we make our Uniform Accounting adjustments, we realize that GameStop’s profitability, while not great, has not been completely wiped out. In fact, Uniform Earnings was roughly flat from 2018 to 2019.

Credit investors panic has again caused bond yield to rise well above high yield averages, above that 7% threshold. But Uniform Accounting gives us the ability to understand that even though cash flows aren’t as strong today as they were in 2016, they can still handle all the company’s obligations, meaning credit investors are again doing what they do best, be too pessimistic.

Material liquidity and a robust recovery rate indicates that ratings agencies and cash bond markets are overstating credit risk

Cash bond markets are materially overstating credit risk with a YTW of 7.325% relative to an Intrinsic YTW of 5.325% and an Intrinsic CDS of 367bps. Furthermore, Moody’s is overstating the firm’s fundamental credit risk, with their Ba2 rating, four notches lower than Valens’ IG4+ (Baa1) rating.

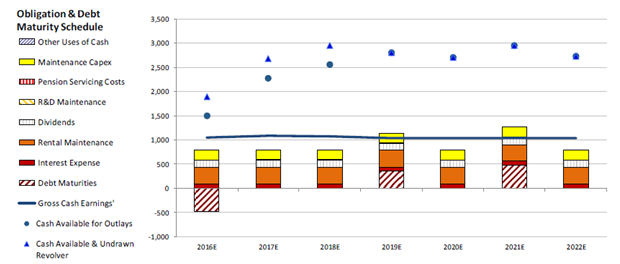

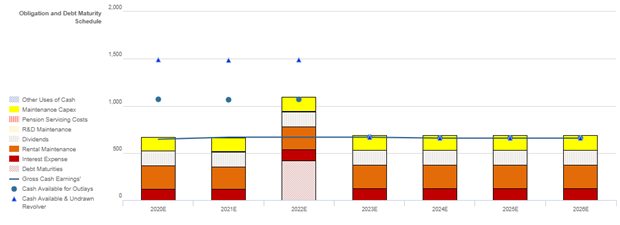

Fundamental analysis highlights that GME’s cash flows will nearly match operating obligations going forward, with an annual deficit of 0%-5% through 2026. However, by trimming maintenance capex, GME’s current liquidity should be sufficient to cover all obligations going forward, including their $469mn debt maturity in 2022. Furthermore, their robust 325% recovery rate should allow them access to credit markets, should they choose to refinance their debt obligations.

Incentives Dictate Behavior™ analysis highlights mostly negative signals for creditors. GME’s compensation framework should drive management to focus on growth and margin expansion, but does not punish management for taking on excess leverage or overspending on assets to drive growth. Moreover, management members are not material owners of GME equity relative to their average annual compensation, indicating they may not be well aligned with shareholders for long-term value creation. That said, as a positive, management members are not well compensated in a change-in-control, indicating they are unlikely to seek a sale or accept a buyout of the company, reducing credit event risk.

Earnings Call Forensics™ analysis from Q2 2019 (9/10) highlights that management may lack confidence in their new cloud platform to improve ROI and in their ability to grow their collectibles business. Furthermore, they may lack confidence in their ability to streamline their digital sales process, and they may be exaggerating the impact their ThinkGeek divestiture had on gross margin. Finally, they may lack confidence in their ability to continue driving down their debt.

Given the firm’s significant liquidity and robust recovery rate, cash bond markets and Moody’s are overstating the firm’s fundamental credit risk. As such, a tightening of credit spreads and a ratings improvement are likely going forward.

GameStop Tearsheet

As our Uniform Accounting tearsheet for GameStop highlights, GameStop trades well below market average valuations. The company has recently had a 13% Uniform EPS decline. EPS is forecast to continue to fall, dropping 21%, in 2019, followed by a 47% drop in 2020.

At current valuations, the market is pricing the company to see earnings shrink by 21% a year going forward.

The company’s earnings growth is forecast to be below peer averages in 2019, and the company is trading well below peer average valuations. The company has average returns and moderate cash flow risk going forward.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research