Uniform Accounting helps reveal this medical device supplier’s rebound

The pandemic has dealt a major blow to the business of elective procedures, with waves of infection leading to a delayed return to hospitals for elective procedures.

However, as we look to the future with hopes for a receding Delta wave and a return to more normal hospital operations, the medical device companies that provide hospitals with the equipment and technologies they need to operate stand to benefit from a strong rebound in demand.

Yet, for one of the industry’s leading players, as-reported metrics both distort the direction and understate the magnitude of historical profitability.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Last year during the height of the pandemic, elective procedures, which like the name suggests are planned ahead of time, came to a screeching halt as the virus spread and people avoided going to hospitals and doctors’ offices.

There was a well-placed sense of fear about catching the virus, and many believed non-critical surgeries and aesthetic procedures could be put on hold until the situation improved.

Even emergency surgeries saw a material decline, as car accidents and other related injuries trended down with fewer people willing or able to leave their homes due to the pandemic.

While this has all hit hospitals quite hard, the impact to the medical device manufacturing companies that supply hospitals and doctors with the equipment they need to operate has been just as severe.

Globus Medical (GMED) is exposed to the orthopedic space for both emergencies and elective procedures, as well as degenerative and genetic disorders for muscular skeletal issues.

The company makes a variety of implants and other healthcare products to help people deal with issues ranging from spinal pains and joint discomfort to deformities and tumors.

Using as-reported metrics, one might easily look at a medical device company like Globus and declare that its tailwinds and competitive moat have been in decline long before the pandemic even started.

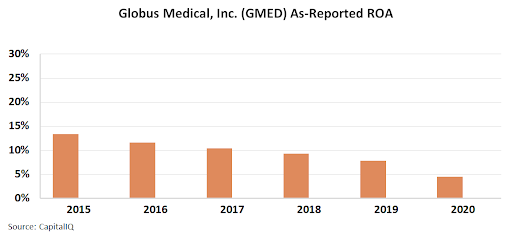

With as-reported return on assets (ROAs) in a secular decline over the past 10 years, the recent drop from an already lowly 9% in 2019 to cost-of-capital levels in 2020 only seems to reinforce this thesis.

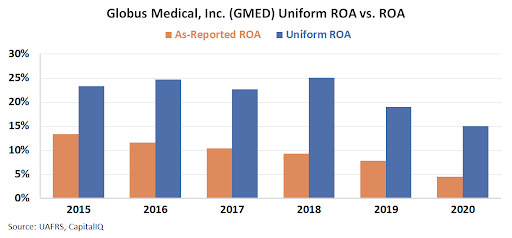

However, it’s only when one digs deeper and looks at the real economic reality of the business with Uniform Accounting that they can begin to realize this decline story is misleading.

This is because over the past 6 years, Uniform ROA has been remarkably stable at around 20%-25% levels, before declining in 2019 and 2020 to 15%, due to headwinds around the pandemic.

In fact, from 2015 to 2018, while as-reported ROA steadily declined, Uniform ROA actually expanded from 23% to 25%.

See for yourself below…

This presents an entirely different picture of Globus’ profitability trends, and shows how, based on its strong historical returns, the company enjoys a wide economic moat that will help it see a strong rebound in demand as hospitals begin to fully recover once the Delta wave is behind us.

Without using Uniform Accounting, one would be led to believe this powerful player in the medical device space was heading to the dustbin. Instead, it may be a name to investigate as the world is reopening.

SUMMARY and Globus Medical, Inc. Tearsheet

As the Uniform Accounting tearsheet for Globus Medical, Inc. (GMED:USA) highlights, the Uniform P/E trades at 34.8x, which is above the global corporate average of 21.9x and its historical average of 30.5x.

High P/Es require high EPS growth to sustain them. That said, in the case of Globus, the company has recently shown a 12% Uniform EPS contraction.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Globus’ Wall Street analyst-driven forecast is an EPS growth of 41% and 15% in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Globus’ $83 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 20% annually over the next three years. What Wall Street analysts expect for Globus’ earnings growth is above what the current stock market valuation requires in 2021 but below that requirement in 2022.

Furthermore, Globus’ earning power is 2x the corporate average. Also, cash flows and cash on hand are more than 6x above its total obligations—including debt maturities, capex maintenance, and dividends. This signals a low credit risk.

To conclude, Globus’ Uniform earnings growth is in line with its peer averages and the company is also trading in line with its peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research