The government might pull the plug on solar

The U.S. Senate’s proposal to phase out wind and solar tax credits by 2028 poses a major threat to the solar industry.

First Solar (FSLR), which benefited significantly from the Inflation Reduction Act’s production tax credits, has built its U.S.-focused business around these incentives.

Without them, its profitability could return to pre-IRA levels, where it struggled to meet its cost of capital.

Despite a 17% drop in First Solar’s stock and headwinds, the market still assumes the company will maintain returns higher than its historical norm.

Meanwhile, other energy sources like nuclear and geothermal are keeping their tax advantages longer, signaling a shift in legislative support.

If these subsidies disappear, First Solar risks becoming just another low-margin player in a tough global market.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

The future of the solar industry has been cast into serious doubt following a new spending proposal from the U.S. Senate Finance Committee.

This proposal calls for an accelerated and complete phase-out of the crucial wind and solar tax credits by 2028.

The market’s reaction to this news was immediate and severe, reflecting deep investor concern about the profitability and stability of the entire sector.

The plan strikes at the heart of the industry’s financial structure, which has become heavily reliant on government incentives.

For companies like First Solar (FSLR), the implications are particularly significant.

First Solar presents a unique business case, standing out as a vertically integrated, U.S.-based manufacturer with a focus on utility-scale projects.

The company has centered its business on high-volume, long-term supply contracts with independent power producers and commercial clients, providing a degree of stability against the industry’s cyclical nature.

A key differentiator for First Solar is its proprietary Cadmium Telluride, or CdTe, thin-film panel technology.

This technology offers distinct advantages in its manufacturing process, resulting in a lower cost per watt and a smaller carbon footprint compared to the dominant crystalline silicon panels produced primarily in China.

However, this technology has a significant drawback: lower field efficiency, meaning a First Solar project requires a larger land area to generate the same amount of energy.

The financial performance of the company is closely tied to U.S. government policy, specifically the Advanced Manufacturing Production Credits, also known as the 45X tax credits, introduced by the Inflation Reduction Act.

When the Inflation Reduction Act passed in 2022, First Solar quickly became one of the biggest beneficiaries.

The legislation offered production tax credits not only for the installation of solar systems but for each watt of solar panel produced domestically. That meant First Solar could make money before a single panel left the warehouse.

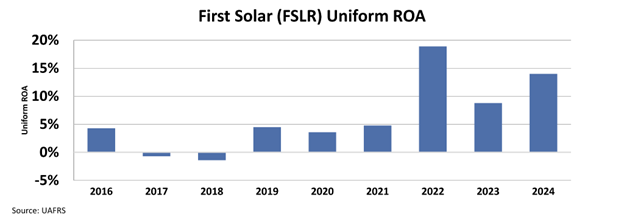

Before the Inflation Reduction Act, the company often found it difficult to operate at its cost of capital.

The tax credits provided by the act were instrumental in changing this dynamic, enabling First Solar to generate a Uniform return on assets ”ROA” between 9% and 19% in recent years.

The potential removal of these subsidies threatens to return the company, and many others like it, to a far more challenging operating environment.

The details of the legislative proposal reveal the extent of the challenge. The subsidies would be cut by 60% in 2026 before being eliminated entirely by 2028, a dramatic acceleration compared to the current law’s phase-out beginning in 2032.

This proposed shift triggered a significant sell-off, with the Invesco Solar ETF experiencing a sharp 9% decline and shares of First Solar falling over 17%.

Despite the headwinds and the market’s reaction to the news, the company still doesn’t appear to be a bargain even after the selloff.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s Uniform ROA will fall to just around 9%, above levels before the tax credits were introduced.

Adding to these concerns is the contrasting treatment of other energy sources.

Tax credits for energy storage, nuclear, and geothermal energy are not scheduled to begin phasing out until 2033. This suggests a strategic pivot in legislative priorities away from wind and solar.

While First Solar has pursued an aggressive and costly expansion of its U.S. manufacturing footprint to capitalize on domestic production trends, the potential removal of the credits that make its domestic products financially viable creates severe headwinds.

The core value proposition of First Solar was always that it could thrive under U.S. policy meant to promote clean energy manufacturing.

If that policy is rolled back, then First Solar is back to being a thin-margin manufacturer in a hypercompetitive global industry.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research