While operational disruptions may concern investors, this firm demonstrates that substantial liquidity can alleviate bankruptcy concerns

Bankruptcy risk goes beyond just examining short-term operational solvency. A prudent credit investor also has to take into account a firm’s liquidity.

While the coronavirus has severely impacted this firm’s operations, likely causing its cash flows to fall well short of its operating obligations, the firm’s substantial liquidity, driven by recent debt issuances and significant cash on hand, should allow it to weather near-term headwinds without bankruptcy concerns.

Below, we show how Uniform Accounting restates financials for a clear credit profile to confirm this counterintuitive view.

We also provide an equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

When looking at whether or not a company is a bankruptcy risk, the first question is generally around operational solvency. Is the company bringing in more cash than it spends?

After that, investors look at whether the firm can service debt obligations, and what kind of asset backing there is for refinancing.

Reports from firms like Moody’s and S&P refer to metrics such as debt servicing ratios (cash flow relative to costs) and leverage ratios (debt relative to equity backing, or how easily you can access markets if needed).

The last consideration, possibly the most important one at times, is a company’s liquidity. That is, how much cash does the company have on hand to service cash flow shortfalls or keep itself afloat if lending dries up.

In the middle of the oil and gas disaster of 2015, most of the companies in the oil and gas industry were major cash flow risks. We talked about them in a prior report.

It’s hard to generate any cash flow when your whole business revolves around a commodity whose value drops by 50% seemingly overnight.

But those companies that had liquidity, like the names we talked about in that report, had a very valuable asset—time.

Those companies that had the cash available to navigate short-term cash flow issues, and had time before material debt headwalls came due, could survive just long enough to get operations back to normal.

This time around, not only is oil and gas in trouble again, but other industries, such as retail, are also facing major headwinds related to the coronavirus.

Finding those names that have liquidity, and time, can be key to finding compelling investments in this market. The Gap (GPS) is one of those names.

The Gap was able to issue a good deal of debt recently to bolster its liquidity position and buy itself time. While the company has effectively operated with no revenues over the last few months, it has the liquidity to survive.

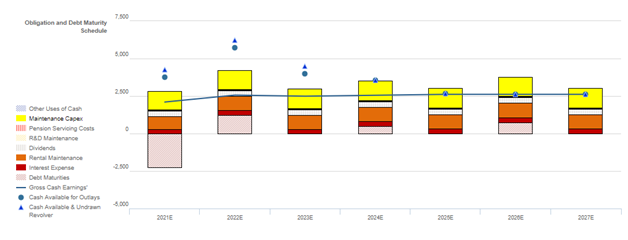

Looking at a picture of the firm’s cash flows and obligations, things clearly aren’t pretty:

Cash flows are going to fall short of obligations this year, and probably the next, and potentially other years going forward.

But the firm does have several billion dollars in cash sitting on its balance sheet, and that means it should be able to survive at least through 2024 without having to refinance once more.

That means there are four years, at least, before the firm would face a real credit crunch. As a result, current yields on the firm’s debt are likely much too high, suggesting that prices on its bonds are likely to improve soon, once the market recognizes this cash cushion.

GPS’ Sizeable Cash Flows and Robust Recovery Rate Warrant Rating Improvement

Credit markets are grossly overstating GPS’ credit risk with a cash bond YTW of 8.374% and a CDS of 615bps, relative to an Intrinsic YTW of 2.124% and an Intrinsic CDS of 186bps. Furthermore, Moody’s is overstating the firm’s fundamental credit risk, with its Ba2 credit rating two notches lower than Valens’ XO (Baa3) credit rating.

Fundamental analysis highlights that GPS’ cash flows would roughly match operating obligations in each year going forward with slight reductions in capex spending.

In addition, following the firm’s recent issuance of three series of bonds, GPS’ expected cash flows plus cash on hand should be sufficient to cover all obligations including debt maturities until 2024.

Moreover, the firm’s robust 220% recovery rate on unsecured debt and moderate market capitalization should allow it to access credit markets to refinance, as evidenced by its recent large-scale debt restructuring.

Incentives Dictate Behavior™ analysis highlights mostly negative signals for credit holders. GPS’ management compensation framework should drive them to improve their margins and grow the top-line. However, this may come at the expense of debt holders, as there is no punishment for taking on excess leverage and overspending on assets to achieve compensation targets.

Furthermore, GPS is a family-controlled firm, where the Fisher family owns substantial amounts of GPS’ stock, and may push the management team to manage the firm in a way that benefits their legacy, with less of a focus on shareholder value.

Moreover, most management members outside of the Fisher family are not material owners of GPS equity relative to their annual compensation, indicating they may not be well-aligned with shareholders for long-term value creation. That said, as a positive, management has low change-in-control compensation, indicating they are unlikely to seek or accept a buyout or takeover, limiting event risk for credit holders.

Earnings Call Forensics™ analysis of the firm’s Q4 2020 earnings call (3/12) highlights that management is confident Banana Republic had an acceleration in Q4 comp sales, that they generated a three-year average free cash flow of $700mn, and that they have accumulated a database of about 60 million known active customers.

Furthermore, they are confident women’s apparel margin expansion outpaced the brand average and that their investments should take excess costs out of the system.

In addition, they are confident that there are opportunities to improve inventory allocation based on channel demand and that the events of the last several years can serve as a positive catalyst for the company.

However, management is also confident that their overall 2019 performance was disappointing, that they had several marketing executional issues, and that they lack the clarity necessary to evaluate their brand position. Additionally, they may be exaggerating their operating discipline.

GPS’ sizeable cash flows, substantial cash on hand, and robust recovery rate suggest that credit markets and ratings agencies are overstating GPS’ fundamental credit risk. As such a tightening of credit spreads and a ratings upgrade are both likely going forward.

SUMMARY and The Gap, Inc. Tearsheet

As the Uniform Accounting tearsheet for The Gap, Inc. (GPS:USA) highlights, the company trades at a 35.1x Uniform P/E, which is above the global corporate average valuation levels and its historical average valuations.

High P/Es only require high EPS growth to sustain them. That said, in the case of The Gap, the company has recently shown a 3% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, The Gap’s Wall Street analyst-driven forecast projects a 77% decline in earnings in 2021 followed by a rebound of 186% growth in 2022.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $9 per share. These are often referred to as market embedded expectations.

The Gap can have Uniform earnings shrink by 12% each year over the next three years and still justify current prices. What Wall Street analysts expect for The Gap’s earnings growth is below what the current stock market valuation requires in 2021 but above requirements in 2022.

Meanwhile, The Gap’s Uniform earnings growth is below peer average levels, but the company is trading above its peer valuations.

In addition, the company’s earnings power is near corporate averages. Furthermore, intrinsic credit risk is only 70bps above the risk-free rate, signaling low risk to its dividend or operations.

To summarize, The Gap is expected to see above average Uniform earnings contraction in 2020, which is expected to rebound massively in 2021, fulfilling market expectations. However, the company is still trading above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research