How Garmin shifted from a standalone GPS manufacturer to a high-tech specialty business

The last fifteen years have seen a tech frenzy in which we went from equipping luxury cars with clunky boxed GPS units to seeing entry-level SUVs with built-in TV-sized GPS units.

While these early units were often not as precise, they were a game changer compared to printed MapQuest directions.

In the following years, GPS tech was enhanced for accuracy and user convenience. More recently, smartphones have followed by being equipped with built-in map applications that made external GPS units nearly obsolete.

As needs evolved along with technology, the competition left some stagnant businesses behind which were unable to adapt to the changing needs.

That’s why we are going to look at Garmin (GRMN) today under a Uniform Accounting lens to see if they were able to successfully transform their business in order to save it.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We originally recommended Garmin to our Conviction Long List subscribers in May 2017 because we could see a unique insight about the company that was only visible using Uniform Accounting.

Prior to 2017, we saw the GPS company’s returns slowly erode. Escalating competition for its legacy GPS business, by the likes of Google’s (GOOGL) phone-based Google Maps app, had slowly withered away demand for its standalone GPS units.

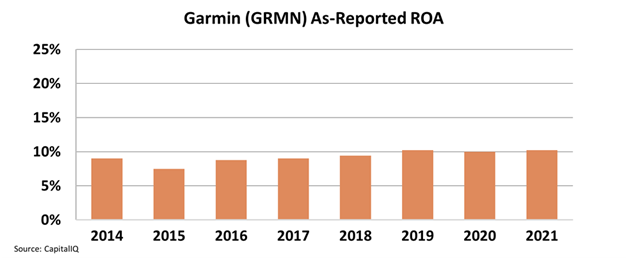

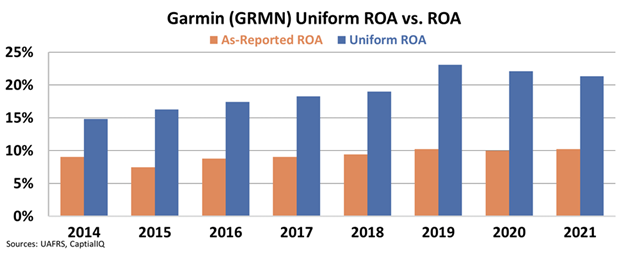

Looking at as-reported returns, which showed Garmin hovering around 9% ROA since 2014, it looks like the company’s returns stayed at flat, uninspiring levels.

Garmin looked like an uninteresting business on the surface, but using Uniform Accounting, we saw an inflection building.

Garmin has had success pivoting from a mainstream brand to specializing in wearables by manufacturing high-tech Aviation and Marine products.

Furthermore, it has developed strong relationships with athletes and those working in rugged conditions by creating smart watches and other outdoor products.

By pivoting to more niche markets, Garmin managed to stay competitive.

Now, it offers a wide range of specialty products with advanced GPS and satellite communication devices.

Consequently when we look at Uniform metrics, Uniform ROA actually bottomed out in 2014 at 15%, and by 2017, Uniform ROA had already expanded to 18%.

We saw this expansion as a catalyst that could drive equity upside, which is why the company was on the Conviction Long List until the end of 2020 when returns plateaued.

During that time, the stock more than doubled, but since taking it off the list, Garmin’s stock is roughly flat.

Unlike as-reported financials that missed this pivot and subsequent recovery, we were able to capture this story and subsequent upside by looking at Uniform Accounting insights.

If you’re curious to see what’s on the Conviction Long List today, click here to learn more.

SUMMARY and Garmin Ltd. Tearsheet

As the Uniform Accounting tearsheet for Garmin Ltd. (GRMN:USA) highlights, the Uniform P/E trades at 15.1x, which is below the global corporate average of 24.0x, but around its own historical P/E of 15.9x.

Low P/Es require low EPS growth to sustain them. In the case of Garmin, the company has recently shown a 13% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Garmin’s Wall Street analyst-driven forecast is a 3% and 7% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Garmin’s $117 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 5% annually over the next three years. What Wall Street analysts expect for Garmin’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power in 2020 is 4x the long-run corporate average. Moreover, cash flows and cash on hand are almost 3x its total obligations—including debt maturities and capex maintenance—including debt maturities, capex maintenance, and dividends.

Together, this signals low credit and dividend risk.

Lastly, Garmin’s Uniform earnings growth is below its peer averages and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research