Here’s what sets Stephen Curry and Bill Ackman apart

As we find ourselves at the end of 2022, we are revisiting some of our Investor Essentials Daily articles from this year that stuck out for one reason or another.

For the final article of the year, we’re returning to a popular portfolio review of one polarizing hedge fund manager who reminds us a lot of one of the NBA’s all-time greats.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

3 seconds left on the clock.

Game 7 of the NBA Playoffs.

The baby-faced assassin has the ball in his hand.

There’s no one else you’d rather trust to take the big shot.

On a court filled with giants and broad shoulders, Stephen Curry’s lithe 6’3 frame and baby face stand in stark contrast to his peers.

Yet, there’s a simple reason Stephen Curry invokes fear every time he walks onto a basketball court.

Putting the basketball through the hoop is the most important skill on the court, and Curry is one of the greatest to ever do it. For even those that are casual basketball fans, it is undeniable that he is a show unto himself.

His mere presence on the floor is gravity-altering as defenders struggle to contain him and his lightning quick shooting trigger.

However, it isn’t just his 3-point shooting that sets him apart. There have been dozens of great shooters in NBA history.

It’s the fact that he takes shots that would be considered “bad shots” for anyone but him.

More nights than not though, he is a human flamethrower, capable of lighting it up the second he steps onto the floor.

Outside of his natural talent, there are two key factors for Curry’s success night-in and night-out.

The first is that he has an undeniably impressive work ethic, with one of the most rigorous conditioning and training programs in the league.

The second, and frankly more important reason, is that while he is as humble as can be off the court, he is stubbornly arrogant in his skills when playing.

But even the greatest shooter of all time will go through slumps where it feels like everything is missing.

Pershing Square’s Bill Ackman is no different. An imminently talented money manager, Ackman has the raw talent, the insatiable work ethic, and the headstrong arrogance to make big bets against the market.

Since inception, Ackman’s funds have given investors a net annualized return of 17.4%, nearly doubling the annual market return.

It has not always been a smooth journey up. His funds are known to have dramatic swings because he takes big bets, but he has proven to have a history of winning in the long run.

Ackman made a historically good call right when the pandemic shut down the U.S., placing a $27 million hedge in mid-February that netted his fund $2.6 billion just a month later.

Sometimes, his bets don’t pan out. Most recently, Ackman made a poor bet on Netflix (NFLX) in the past few months.

After a characteristically public endorsement of the streaming company, Netflix posted its first negative subscriber growth in a decade, and Ackman turned around and sold his stake for a $430 million loss.

Perhaps he has just learned to cut his losses early, after losing more than $3 billion on Valeant Pharmaceuticals in 2017.

With his history of making big bets that sometimes fall wayside, let’s take a look at his bets, using Uniform Accounting, to see if these are set to win or lose going forward.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It is no surprise that once many of these distortions are accounted for, it becomes apparent which companies are, in reality, robustly profitable and which may not be as strong of an investment.

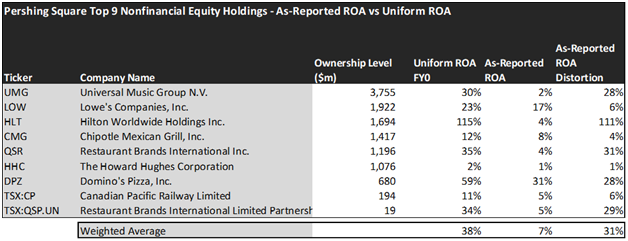

Just as one would expect from such an investor that has come out on big bets too many times, the Pershing Square portfolio is much stronger than the as-reported metrics dictate.

The average as-reported ROA among Pershing’s top 9 names is 7%, slightly above U.S. corporate averages. In reality, though, these companies are massively profitable on average, with a 38% Uniform ROA across the top nine.

Universal Music Group (UMG) for example doesn’t have average 2% returns. Rather, it has a 30% Uniform ROA.

Similarly, Chipotle Mexican Grill (CMG), isn’t an 8% business, the immensely popular fast casual food chain has produced a 12% Uniform ROA.

Some of Pershing’s other investments are also much stronger than they appear. For example, Domino’s Pizza (DPZ) isn’t your average pizzeria. It has taken its fair share of the pie when it comes to profitability with 59% returns which belie the technology that Dominos has implemented.

Largely, once we account for Uniform Accounting adjustments, we can see that many of these companies are strong stocks that have unfairly been beaten down by occluded accounting standards.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The Uniform ROA FY0 represents the company’s current return on assets, which is a crucial benchmark for contextualizing expectations.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here is 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, average Uniform P/E across the investing universe is roughly 24x.

Embedded Expectations Analysis of Pershing Square paints a clear picture of the fund. The stocks it tracks are strong, but the markets are already pricing them in much higher returns than even analysts are expecting.

While the fund has analysts expecting them to have a strong improvement in Uniform ROA of 53%, the market is pricing the fund in for significantly higher returns at 122%. While earnings can always compound beyond analyst expectations, it looks like in aggregate Pershing Square is overpaying for its current investments.

In particular, there are a couple of companies that are the most likely to cause disappointment with their future return expectations.

Hilton Worldwide Holdings (HLT) is the most likely culprit as the market is expecting them to increase to 621% as opposed to analyst expectations of a modest increase to 162%. However, this isn’t a sign that Hilton is a bad business. Rather as a holdings company, they have an asset light model that is sensitive to profitability changes.

Another company that may similarly disappoint is our previously mentioned Domino’s Pizza. While the market is pricing them in for 84% returns, analysts are expecting them to actually decline in profitability to 55%.

This just goes to show the importance of valuation in the investing process. Finding a company with strong growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which have not been fully priced into their current prices.

To see a list of companies that have great performance and stability also at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of one of the largest holdings in Pershing Square’s Portfolio.

SUMMARY and Lowe’s Companies, Inc. Tearsheet

As one of Pershing Square’s largest individual stock holdings, we’re highlighting Lowe’s Companies, Inc.’s (LOW:USA) tearsheet today.

As the Uniform Accounting tearsheet for Lowe’s highlights, its Uniform P/E trades at 24.7x, which is above the corporate average of 18.4x and its historical average of 20.0x.

High P/Es require high EPS growth to sustain them. In the case of Lowe’s, the company has recently shown a Uniform EPS growth of 27%.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lowe’s Wall Street analyst-driven forecast is for EPS to decline by 16% and grow by 25% in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lowe’s $206.14 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were flat annually over the next three years. What Wall Street analysts expect for Lowe’s earnings growth is above what the current stock market valuation requires through 2024.

Meanwhile, the company’s earning power is well above long-run corporate averages. Also, cash flows and cash on hand consistently exceed total obligations—including debt maturities and capex maintenance. Moreover, intrinsic credit risk is 50 bps. Together, these signal low dividend and credit risks.

Lastly, Lowe’s Uniform earnings growth is below its peer averages and its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research