Ackman’s obsession with real estate might prove costly once again

Bill Ackman is undoubtedly one of the most talented fund managers of the last 20 years. He has been on the right side of huge bets mostly, which made him a fortune.

However, even the greatest investors are at risk of having a blind spot. Ackman is known for his love of real estate, which comes from his family’s history in the industry.

He has been investing very heavily in The Howard Hughes Corporation (HHC), a diversified real estate company that owns everything from retail to multi-family, hospitality, and other types of buildings.

A look into our Embedded Expectations Analysis (“EEA”) shows that the market expects the company to reach all-time high profitability.

Given the macro environment, these expectations seem incredibly rosy, which might mean further downside for Ackman.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

As we have highlighted before, Bill Ackman is one of the most successful investors of the past 20 years.

He made a living by making big bets on the right investment positions. While there are many victory laps we could take for him, the most impressive is probably the trade he made at the beginning of the pandemic.

He correctly foresaw the potential disaster of the pandemic on financial markets in February 2022, even before the pandemic was officially recognized by the World Health Organization (“WHO”).

Instead of dumping the stocks he had and being seen as a corporate raider, he bought credit default swaps on the debt of Hilton and various other consumer exposed companies to hedge out his position.

He saw his portfolio boom as soon as the next month. WHO recognized Covid-19 as a pandemic, and the stock market fell 30% in the blink of an eye.

It’s said that Ackman turned $27 million into $2.7 billion with that trade. It’s arguably the single most successful trade in history.

However, like all the other investors, he doesn’t get every investment right. And sometimes he lets his heart rule his head.

In particular, it appears he might have a blind spot with his love of real estate thanks to his family’s history in the industry.

His pitch to turn Target (TGT) into an insurance-hedged real estate investment trust (“REIT“) in the late 2000s was mocked for years after.

Even as real estate has continued to be a looming crisis for the past year or two, he has kept growing the fund’s ownership in the industry.

He has done that with one of his favorite companies: The Howard Hughes Corporation (HHC). The diversified real estate company owns everything from retail to multi-family, hospitality, and other types of buildings.

Pershing Square’s ownership surged from below 10% in 2010 to just above 32% now, with most of the investments being made after the pandemic hit in 2020.

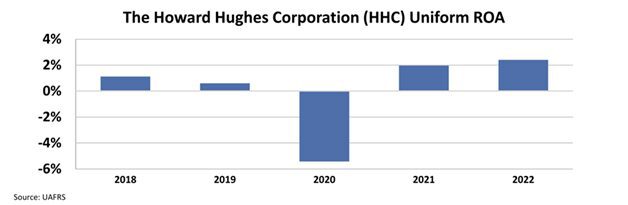

And the interesting thing is that it was the worst year Howard Hughes has ever had. Its Uniform return on assets (“ROA”) fell from just above 0% in 2019 to below -5% in a year.

The company had a fast recovery with its ROA reaching 2% in 2021, before slightly surpassing that level in 2022.

This might seem like he bought the company at the dip but that is not the case at all.

The stock never recovered after the pandemic. Even though it doubled from March 2020 to April 2021, it could not reach pre-pandemic levels.

One might think that the company’s valuations were cheap when he bought the stock, but this can only be understood by knowing the market’s expectations.

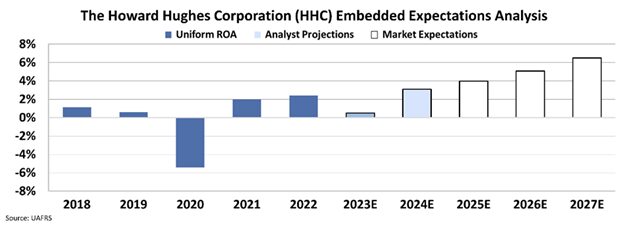

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

The stock price is at around $75, still lower than pre-pandemic levels. Despite that, the market prices the ROA to surge to above 6%, which would be an all-time high.

The outlook of the real estate industry does not look good with interest rates rising and house sales and commercial real estate prices falling.

Considering the macro environment, these expectations look overly optimistic, implying that there is still room to fall for the stock.

Ackman might be a talented investor, but his love for real estate may be giving him a blind spot with this company.

SUMMARY and The Howard Hughes Corporation Tearsheet

As the Uniform Accounting tearsheet for The Howard Hughes Corporation (HHC:USA) highlights, the Uniform P/E trades at 295.3x, which is above the corporate average of 18.4x and its historical P/E of 186.6x.

High P/Es require high EPS growth to sustain them. In the case of Howard Hughes, the company has recently shown a 413% shrinkage in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Howard Hughes’ Wall Street analyst-driven forecast is a 333% EPS and 182% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Howard Hughes’ $76 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 24% annually over the next three years. What Wall Street analysts expect for Howard Hughes’ earnings growth is below what the current stock market valuation requires through 2024.

Furthermore, the company’s earning power is below its long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 350bps above the risk-free rate.

All in all, with no dividends, this signals average credit risk.

Lastly, Howard Hughes’ Uniform earnings growth is below with its peer averages but above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research