This med-tech company helps provide care to one of the most underserved markets in healthcare

Drug trials often fail to test women as frequently or rigorously as men. This can lead to serious consequences for drug distribution.

Today’s company is a healthcare firm that develops and supplies diagnostic and surgical products to serve the healthcare needs of women. Using Uniform Accounting, it becomes clear how successful the firm has been.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

It’s an unfortunate fact that most pharmaceutical treatments are tested far more robustly on men than on women.

Many companies have shied away from conducting thorough studies on women, fearful that factors like pregnancy and monthly cycles could lead to adverse health effects.

After scares like the thalidomide tragedy in the 1960s, which led to mass birth defects, drug researchers have become more hesitant to include women in drug trials.

With lives at stake and the risk of bad data, it’s easier, though certainly not more accurate, for drug trials to be made up of predominantly men.

This has led to unexpected reactions from drugs that have only been thoroughly tested on men being used with women. For example, there have been cases of women who, after taking medication such as ambien and cisapride, have suffered life-threatening side-effects.

By and large, the healthcare industry continues to overlook women’s healthcare needs, and women as a whole represent an underserved market. This is the social need Hologic (HOLX) is trying to fill by focusing specifically on women’s health.

Hologic produces both diagnostics and surgical products, ranging from breast health, OB-GYN surgical needs, and diagnostics for fetal health. Recently, the firm debuted a successful test for the coronavirus, which has put the firm in the spotlight.

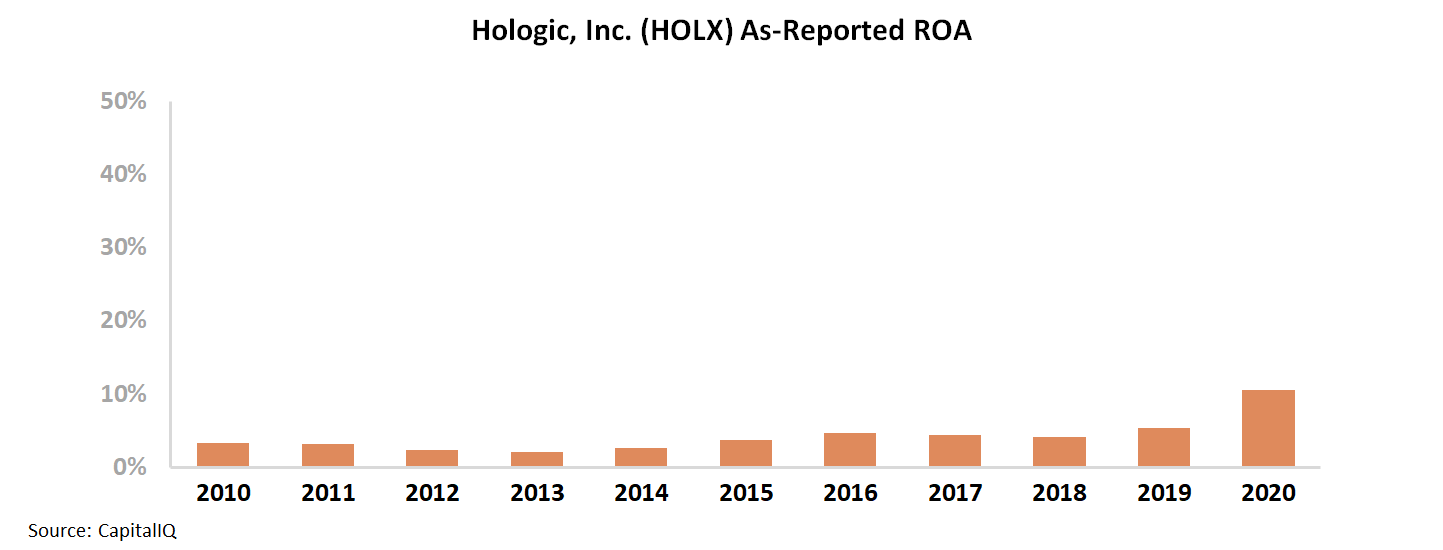

Using as-reported metrics, investors couldn’t be blamed for thinking of the company as simply another struggling healthcare firm. As-reported metrics signal the company was unable to earn any premium return for its strategy.

Over the past eleven years, it appears that Hologic has seen returns stagnate below the corporate average profitability of 12%. Only in 2020 have returns broken this pattern, which might indicate the firm is only now gaining a competitive advantage from its coronavirus testing.

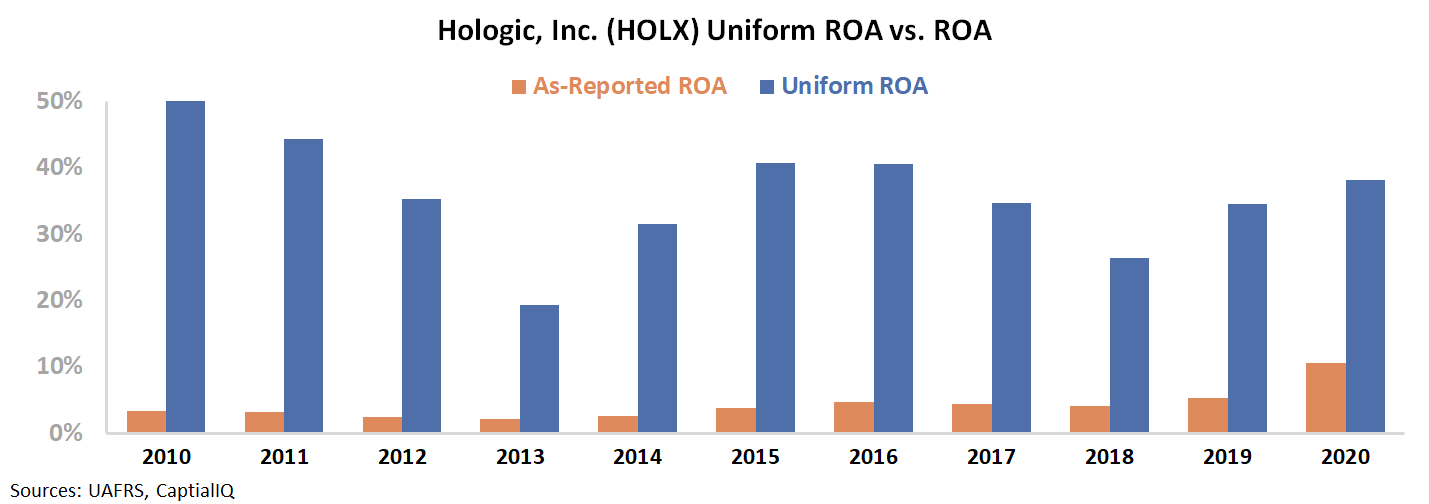

In reality though, this story is just another example of bad accounting.

Hologic’s ROA was never stagnant in the past eleven years. When as-reported accounting distortions are removed, it becomes clear that the company has seen profitability consistently above averages.

Uniform ROA remained above 19% for the last decade, recently expanding back to 38% levels. Hologic has been able to fill an important niche in the healthcare industry for years by focusing on women’s needs.

Investors looking only at as-reported returns may assume the firm was only able to see profitability from producing a testing solution for the pandemic, and avoid the name after the need for testing has passed.

However, when a Uniform Accounting lens is applied to the firm, it becomes clear this would be a huge mistake. Hologic has been profitable for years paying attention to a space others should be operating in. Only through using Uniform Accounting can investors see the complete picture.

SUMMARY and Hologic, Inc. Tearsheet

As the Uniform Accounting tearsheet for Hologic, Inc. (HOLX:USA) highlights, the Uniform P/E trades at 12.8x, which is below the global corporate average valuation levels, but around its historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Hologic, the company has recently shown a 50% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Hologic’s Wall Street analyst-driven forecast is a 54% EPS growth in 2021, followed by a 43% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Hologic’s $76 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 1% per year over the next three years and still justify current stock prices. What Wall Street analysts expect for Hologic’s earnings growth is above what the current stock market valuation requires in 2021, but below its requirement in 2022.

Furthermore, the company’s earning power is 6x the corporate average. Also, cash flows and cash on hand are almost twice its total obligations—including debt maturities and capex maintenance. Together, this signals an average credit risk.

To conclude, Hologic’s Uniform earnings growth is significantly above its peer averages, but the company is trading well below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research