How cryptocurrencies and banking combine to make the next fintech revolution

Investors and speculators are loving the recent boom in the cryptocurrency space. With the upcoming public offering for Coinbase, investors are looking for other angles to be exposed to the crypto space.

Today, we highlight another way investors can be making money from holding cryptocurrencies. With cryptocurrency trading still in its infancy, we will break down the opportunities and risks for investors interested in this alternative space.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Coinbase, the cryptocurrency trading platform, is set to go public later this month. It won’t be doing so through an IPO or a SPAC–instead, it will be a direct listing.

This means instead of working with banks to create new shares, Coinbase will be cutting out the middleman to list existing shares of the company on the open market themselves.

Investors looking for a bargain at the ground floor may be sorely disappointed. Coinbase was valued at $90 billion when it last raised capital, a huge value for service in the competitive world of crypto brokerages. As the company isn’t even one of the largest players operating today, this goes to show the staggering value investors see in the nascent cryptocurrency market.

Analysts may be looking at the business model of Coinbase and scratching their heads as to how the company is worth so much. The traditional business model of an exchange is earning a small fee on each transaction. While this can be asset efficient, it isn’t necessarily a booming business, as it is tied entirely to the growth, or lack thereof, of transaction volumes.

Anyone looking at Coinbase and other exchanges this way is missing the big opportunity here though. These exchanges are turning themselves from traditional marketplaces into something that resembles a bank as much as an exchange.

As anyone who has looked at a savings account the last ten years will tell you, it doesn’t pay to save if you’re putting money away in a normal account. Even “high yield” accounts at places like Goldman Sachs’ Marcus don’t beat inflation with a 0.50% APR for a savings account.

This has been one reason investors are on the lookout for high-yield investments, as we have highlighted multiple times before. Despite this, large swaths of the high-yield debt space only offer sub 3% loans. As inflation is rising, even that doesn’t offer much real yield.

So, many people desperate for yield have been attracted to a new way to get their money to work for them and earn them an income. While many people spend their time figuring out which of the latest alt-coins should be bought that might rocket higher, living in the world of speculation, in the shadows a world of crypto income investing has emerged.

Some of the exchanges are now offering customers an interest rate on cryptos they keep at the exchange. If investors are willing to allow the exchange to lend out their cryptos, they can make a 6%, 12%, or even 17% APY by just leaving their cryptos “in the bank.

In such a low interest rate environment, it may look like a compelling opportunity for many.

Coinbase doesn’t yet have this feature. If and when it does roll the feature out, and it is working with regulators to approve its own interest paying arm, that could be a booming growth opportunity that could justify the valuations the company trades at.

Some investors look at these interest rates skeptically. They are right to be thinking a savings account with these kinds of yields is too good to be true. Those looking for a standard, FDIC-insured savings account are sorely mistaken.

By letting an exchange borrow your cryptocurrency, there is no insured amount in case of bankruptcy. Rather, you are acting as an unsecured creditor to a nascent bank and its creditors.

If someone borrows in cryptocurrency, converts it into dollars, and then the cryptocurrency rises significantly higher thereafter, they may not be able to pay off their debts, and the people who lent to them would stand to lose.

This is a risk investors need to be compensated for. That being said, this isn’t necessarily the main reason interest rates are so high.

The other driver of such a luxurious rate is the simple phenomenon of supply and demand.

If an investor is lending out cryptocurrency, it is because another investor is looking for cryptos to borrow. Currently, there is not a large use case for cryptocurrencies in everyday transactions, barring the standouts like Tesla (TSLA) accepting bitcoin as payment. This means most borrowers are looking for liquidity.

Most crypto borrowers are doing so because they already have crypto assets. They are looking to hold onto their assets but need liquidity now. They might be crypto miners, crypto exchanges who accept payment for transaction fees in crypto, or companies who have raised capital in an ICO. Their money is tied up in crypto, but they need to pay employees, suppliers, and partners in real world currencies.

They may even just be sitting on massive capital gains from the cryptos they’ve owned, and don’t want to realize those gains by selling the cryptos.

They are borrowing cryptocurrencies, like ether or bitcoin, from someone else to exchange these coins for a different currency usable in the real world, like U.S. dollars.

As we mentioned above, considering that much of this borrowing is eventually converted to another currency, if the borrowers see the cryptocurrency they borrowed appreciate, it might be hard for them to repay.

To help combat this, along with controlling the volatility of many cryptos, many exchanges require anyone borrowing to have material reserves at the exchange, often at least 50% of the value of the loan in the same crypto. This helps reduce the risk that they won’t be able to pay back the loan.

Unsurprisingly, the supply and demand of different cryptocurrencies impact the interest rates that individuals lending coins out can stand to make.

We had one of our interns from our new Eurasia office prepare a presentation for us to dive into the intricacies of the new crypto banking market. There is huge upside potential for the first few banks or exchanges that figure out crypto lending.

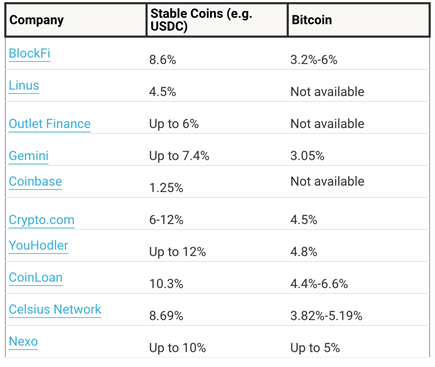

During this research, her data showed the interest rate cryptocurrency exchanges will pay on “stable coins,” or coins whose value is tied directly to the U.S. dollar like USDC and USDT, is much higher and more available than for leaders in the space like bitcoin.

Once we understood the “why” of why people are borrowing cryptocurrencies, this made a lot of sense.

The reason why comes back to supply and demand. If borrowers are borrowing in a coin so they can get short-term cash liquidity, they want to make sure the value of their debt won’t skyrocket against that cash.

Therefore, they borrow in a less volatile coin like USDC or USDT. This drives up the lending rate for stable coins on the back of heightened demand.

Below is a table of the example of some interest rates that crypto coin owners can earn on different exchanges from a week or so ago.

This is just another example of how crypto assets behave just like other financial assets, contrary to what some pundits may have you believe. And importantly, it’s one way that those struggling to understand why they might want to invest in cryptocurrencies might see an economic reason to do so.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research