Here’s how a fund of funds approach is performing this year

The financial markets are often difficult to maneuver and completely understand. Successful investors will dedicate endless hours to devising different strategies and methods to beat the market.

But not everyone has time for that.

Hedge funds and asset managers saw an opportunity to provide a solution. They create the funds and all you need to do is put money in them.

This has worked out great for many, but there isn’t much diversity in the investment management industry. These large institutional investors collect funds and allocate them around different portfolios, oftentimes offering no customizable solutions.

That’s where Lighthouse Investment Partners decided to step into the market and offer managed accounts to its clients.

Lighthouse has structured its company to give more power to its fund managers, ultimately allowing for more control over market fluctuations.

Let’s have a look at the firm’s top holdings using Uniform accounting and see if this different management technique and investment strategy could show promise in the upcoming years.

In addition to examining the portfolio, we include a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Also below is a detailed Uniform Accounting tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

The money manager market is quite static. The funds these companies create and monitor are common in style.

Look at BlackRock (BLK) or Vanguard. These funds are largely centered around a set investment style and don’t typically deviate from their original strategy, even if it’s not favorable.

Additionally, these massive institutional investors and asset managers are often structured in similar ways in terms of account management. It is not often in the space you see a hedge fund position themselves to offer managed accounts, this is quite rare among the bigger players.

This sentiment presented a gap in the industry. That’s where CEO/CIO Sean McGould and associates stepped in and created Lighthouse Investment Partners.

For context, managed accounts are investment portfolios that are managed by someone else besides the investor. The hired manager oversees the accounts and is able to execute trades, though there are some parameters that are agreed upon beforehand.

McGould saw the opportunity and went for it.

The company’s managed accounts are distinct, independent entities that are usually held by at least one Lighthouse fund and are controlled by the Lighthouse team. Each managed account’s assets may be traded by the hedge fund managers; they are given authorization by Lighthouse.

Much of this style of management is rooted in McGould’s start in the investment industry.

Lighthouse’s foundation is from Trout Trading Management, where the company originated as a spin-out from one of McGould’s previously managed funds.

McGould and associates entered its new chapter with great knowledge of the industry, as they had the opportunity to work with one of the first market wizards Monroe Trout.

Back then, Trout’s investment firm also utilized managed accounts for its clients.

His principles and management style remain relevant within Lighthouse Investment Partners today.

With current assets under management (“AUM”) at about $62 billion, Lighthouse primarily makes investments in actively managed hedge fund portfolios that aim to diversify exposure to traditional markets.

Often referred to as fund of funds investing. These types of investments pool their capital and invest in other funds, eliminating direct exposure to stocks and other securities.

With a similar structure, Lighthouse also follows a long/short equity strategy. This style consists of taking long positions on securities that are expected to appreciate and hedging them by shorting the securities expected to decline.

In light of this, let’s dig deeper and explore the top holdings of the firm.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It’s no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in real robust profitability and which may not be as strong of an investment.

See for yourself below.

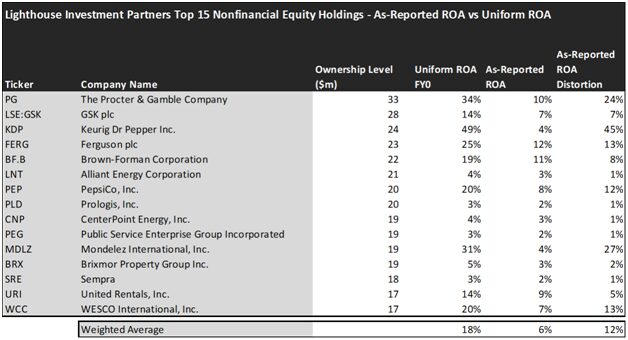

Looking at as-reported accounting numbers, investors would think that Lighthouse Investment Partners invests in below-average companies.

On an as-reported basis, many of the companies in the fund are poor performers. The average as-reported ROA for the top 15 holdings of the fund is 6%, which is significantly below the U.S. corporate average.

However, once we make Uniform Accounting adjustments to accurately calculate the earning power, we can see that the average return in Lighthouse Investment Partners’ top 15 holdings is actually 18%.

As the distortions from as-reported accounting are removed, we can see that Keurig Dr Pepper (KDP) isn’t a 4% return business. Its Uniform ROA is 49%.

Meanwhile, Mondelez International (MDLZ) seems like a 4% return business, but this massive packaged foods company actually powers a 31% Uniform ROA.

That being said, to find companies that can deliver alpha beyond the market, just finding companies where as-reported metrics misrepresent a company’s real profitability is insufficient.

To really generate alpha, any investor also needs to identify where the market is significantly undervaluing the company’s potential.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

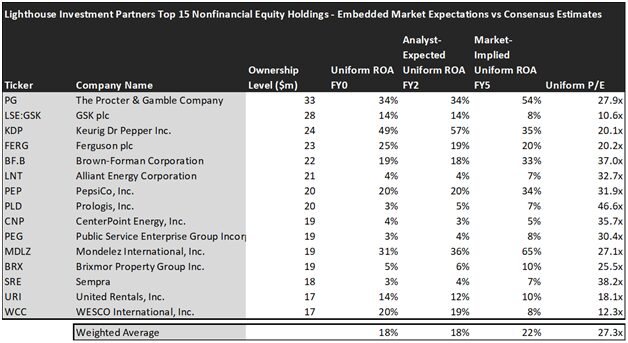

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The average Uniform ROA among Lighthouse Investment Partners’s top 15 holdings is actually 18% which is better than the corporate average in the United States.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here are 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, the average Uniform P/E across the investing universe is roughly 20x.

Embedded Expectations Analysis of Lighthouse Investment Partners paints a clear picture. Over the next few years, Wall Street analysts expect the companies in the fund to maintain the same levels of profitability. On the other hand, the market has a more optimistic view of the companies in the portfolio.

Analysts forecast the portfolio holdings on average to see Uniform ROA stay at the same levels of around 18% over the next two years. At current valuations, the market’s expectations are higher than analysts and it expects a 22% Uniform ROA for the companies in the portfolio.

For instance, The Procter & Gamble Company (PG) returned 34% this year. Analysts think its returns will remain flat at around 34%. And at a 27.9x Uniform P/E, the market expects profitability to significantly improve and is pricing Uniform ROA to be around 54%.

Similarly, PepsiCo’s (PEP) Uniform ROA is 20%. Analysts expect its returns will remain flat at 20%, but the market is more optimistic about the company’s future and pricing its returns to be around 34%.

Overall, we can see that Lighthouse Investment Partners has high-quality names in its portfolio. It’s also important to note that the fund is highly successful in diversifying its portfolio to align itself with changing market conditions.

With that being said, investors still reap the benefits of the managed accounts that Lighthouse uses.

However, due to high expectations of the market for the names in the portfolio, the upside may be limited for investors as the possible improvements for these companies are already priced in by the market.

At the end of the day, investors should carefully analyze the different strategies and management techniques offered and see if they are aligned with their own views of investing. Additionally, the current valuations are another important factor investors should consider before jumping on any investment opportunity.

This just goes to show the importance of valuation in the investing process. Finding a company with strong profitability and growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which has not been fully priced into their current prices.

To see a list of companies that have great performance and stability also at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of one of Lighthouse Investment Partners’ largest holdings.

SUMMARY and GSK Tearsheet

As one of Lighthouse Investment Partners’ largest individual stock holdings, we’re highlighting GSK (GSK:GBR) tearsheet today.

As the Uniform Accounting tearsheet for GSK plc highlights, its Uniform P/E trades at 10.6x, which is below the global corporate average of 18.4x, and its historical average of 13.2x.

Low P/Es require low EPS growth to sustain them. In the case of GSK plc, the company has recently shown 8% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, GSK plc’s Wall Street analyst-driven forecast is for EPS to grow by 1% and 8% in 2023 and 2024, respectively.

Furthermore, the company’s return on assets was 14% in 2022, which is 2x the long-run corporate averages. Also, cash flows and cash on hand consistently exceed its total obligations—including debt maturities and CAPEX maintenance. These signal low dividend risk and low credit risk.

Lastly, GSK plc’s Uniform earnings growth is in line with peer averages, and below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research