This company missed the chance of a lifetime, and the credit rating agencies completely overlooked it

Companies around the world seized a crucial opportunity to lighten their debt loads…but some missed their chance.

Today, we are looking at a company that was once great, and is rated by the credit rating agencies as if it is still a rock-solid name. However, the real picture is not so pretty.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

One of the reasons we’ve been so bullish on the market since March 2020 has been our healthy respect for and deep understanding of credit cycles.

You will frequently hear us saying “the buck stops with debt” because the sudden and dangerous collapses we’ve seen at various times in the stock market stem from companies’ inability to support the weight of their own debt when economic conditions worsen.

Today, we think the overall credit picture looks great coming out of the pandemic. Not only do companies have loads of cash to pay their obligations well into the future, but aggregate year-to-year cash earnings alone are enough to cover any debts.

We’re particularly encouraged to see that management teams have been acting responsibly and refinancing as central banks around the world have been pumping liquidity into the market in the months after the pandemic panic.

With interest rates so low, most companies were smart enough to refinance any of their debt that might come due in the next 2-3 years. This means that even if the economic situation were to worsen again, companies won’t be caught flat-footed, unable to pay their debts.

However, whenever we draw a macroeconomic conclusion, we need to remain mindful of the laggards that may slow things down. We’ve come across a few companies whose debt profiles are far riskier now than they used to be.

One great example of this is the former technology institution that is Hewlett Packard Enterprises (HPE), which is a remnant of Hewlett Packard’s corporate business after it was spun off from its consumer business.

As we frequently say, the major ratings institutions move rather slowly and often miss the mark. This is just one consequence of bad GAAP accounting standards that make it difficult to get a fair sense of how a company is doing without looking at their past as-reported metrics.

S&P rates Hewlett Packard Enterprises as a BBB. This signals to investors that the company’s debt is investment-grade and faces little default risk.

Credit rating agencies see Hewlett Packard to be as safe and high-quality as its long-time legacy before the spinoff. But in reality, the sailing is not so smooth.

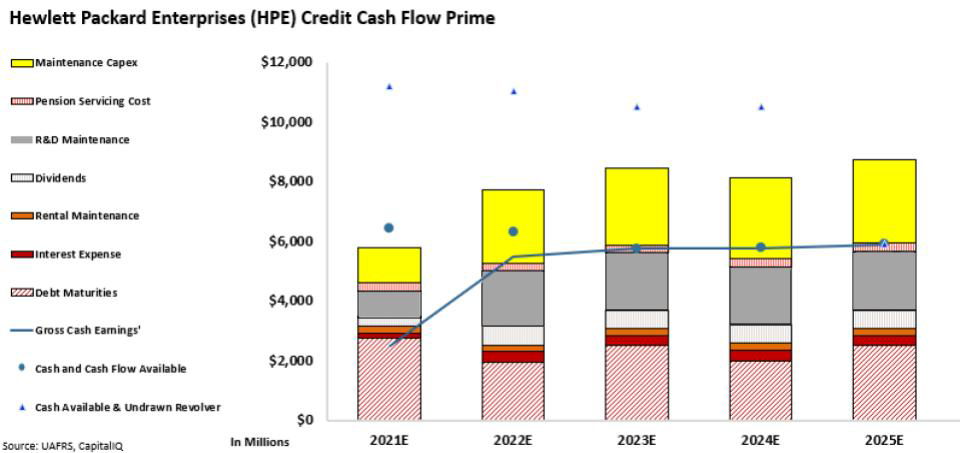

Our Credit Cash Flow Prime (CCFP) framework, which leverages Uniform accounting to correct for the deficiencies of GAAP and soberly evaluate the credit picture for any company, shows that Hewlett Packard Enterprises is staring straight into a collapse under its own debt.

See for yourself below.

The blue dots represent the cash available to the company, while the blue line represents Uniform earnings. The bars represent the set of obligations the Company must pay off in each subsequent year, with the most easily divertible obligations like maintenance capex stacked towards the top, and unbreakable contractual obligations like debt maturities sitting near the bottom:

When looking at the CCFP, we can see that management has not been as responsible as most in managing the company’s capital structure. Unlike many of their corporate peers, Hewlett Packard Enterprises didn’t refinance, and it still has billions maturing each year for the next 5 years.

If credit dries up amid another economic downturn, the company will be stuck in a position where it must choose between refinancing at unsustainable rates, or filing for bankruptcy. Both are losing propositions for both shareholders and bondholders.

Hence, we rate it as an HY2-, a grade given to companies that are in serious trouble. When rating companies, we look only at the data, not a stale reputation.

This approach is not only more intellectually honest, but also yields higher returns for bondholders.

Every month, we distribute our conviction credit list, which uses the CCFP to find the bonds that are most inaccurately priced based on their issuers’ actual abilities to pay their obligations. To see how you can use this information to get ahead of the bond market, click here.

SUMMARY and Hewlett Packard Enterprise Company Tearsheet

As the Uniform Accounting tearsheet for Hewlett Packard Enterprise Company (HPE:USA) highlights, the Uniform P/E trades at 24.1x, which is above the global corporate average of 21.9x and its own historical average of 18.2x.

High P/Es require high EPS growth to sustain them. In the case of Hewlett Packard Enterprise, the company has recently shown a 1% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Hewlett Packard Enterprise’s Wall Street analyst-driven forecast is a 50% EPS decline in 2021 and a 8% EPS growth 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Hewlett Packard Enterprise’s $15.45 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 7% over the next three years. What Wall Street analysts expect for Hewlett Packard Enterprise’s earnings growth is below what the current stock market valuation requires in 2021 but above the requirement in 2022.

Furthermore, the company’s earning power is 2x the long-run corporate average. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. Also, intrinsic credit risk is 150bps above the risk-free rate.

All in all, this signals high dividend and credit risk.

To conclude, Hewlett Packard Enterprise’s Uniform earnings growth is above its peer averages, and the company is trading above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research