Hubbell is an ‘Electrification’ player you need to know

The COVID-19 pandemic upended years of consumer spending habits in a matter of months.

Lockdowns ushered in a new era of goods-buying as consumers spent more and more of their time in their homes. As hybrid work has become the norm, this so-called At-Home Revolution looks set to sustainably last far into the future.

The resulting pressure on good-manufacturers, many of which are struggling to meet this elevated demand, can in part be stemmed by upgrading quickly aging assets like factories and machinery.

As this investment occurs, management teams will focus on next-generation infrastructure that is ever-more connected and able to generate useful insights and efficiencies.

Today, we’ll highlight one name that provides the essential electrical components to allow this infrastructure revolution to take place.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Gross domestic product, or GDP, is composed of four key elements: personal consumption expenditures, government spending, net exports, and business investment.

Most of U.S. GDP comes from the first element. Consumer spending on finished goods and services accounts for 70% of the country’s GDP.

Meanwhile, government spending on public goods like defense and infrastructure typically accounts for somewhere between 15%-20% of GDP, and net exports typically offsets GDP because the U.S. imports more than it exports.

We have regularly talked about a potential surge in U.S. GDP growth in the coming years due to the fourth component: business investment.

For years, businesses across nearly all industries in the U.S. have seen their assets age considerably.

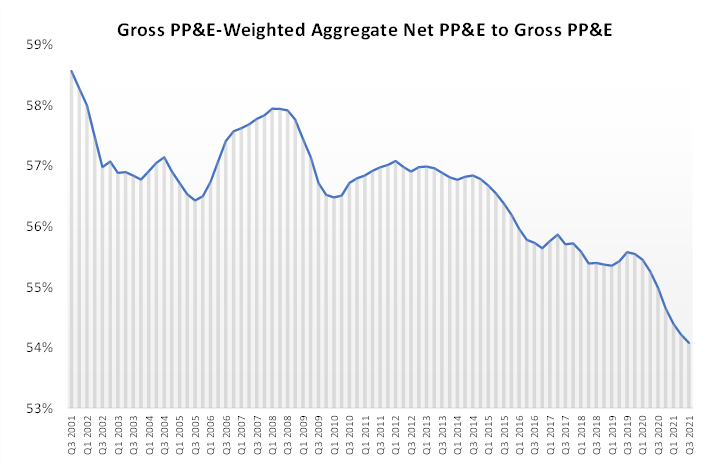

A good proxy to identify this trend is the Net/Gross Property, Plant and Equipment (“PP&E”) ratio, which shows how much essential business assets have been depreciated.

In the chart below, when Net/Gross PP&E ratios are falling, it signals underinvestment and older assets that management teams need to eventually replace to prevent production from breaking down.

Over the past several years, the downward trend has been quite persistent, and recently it has been exacerbated by the economic shock of the pandemic.

Now, with major transformations like the At-Home Revolution spurning massive demand for goods relative to pre-pandemic trends, many producers are in a difficult position.

As companies need to reinvest in themselves to meet heightened demand, which seems likely to last well into the future as we adapt to a post-pandemic world, we are likely to see the first significant capital expenditures (“capex”) cycle in the U.S. in over 20 years.

We expect this upcoming cycle to emphasise “smart infrastructure,” meaning factories, warehouses, buildings, and other infrastructure that are all connected electronically via Wi-Fi and 5G.

To actually create this smart infrastructure however, companies need to build out and adopt the critical components that power connections.

The so-called “electrification of everything” trend is taking off, meaning the key suppliers that can help manage this transition are going to benefit immensely.

One such company is Hubbell (HUBB), which makes components like durable electrical wiring products, connector and grounding components, and other vital electrical equipment that allows smart infrastructure to run smoothly.

The company sits right at the heart of the transformational smart infrastructure in electrification and Internet of Things (“IoT”) revolutions.

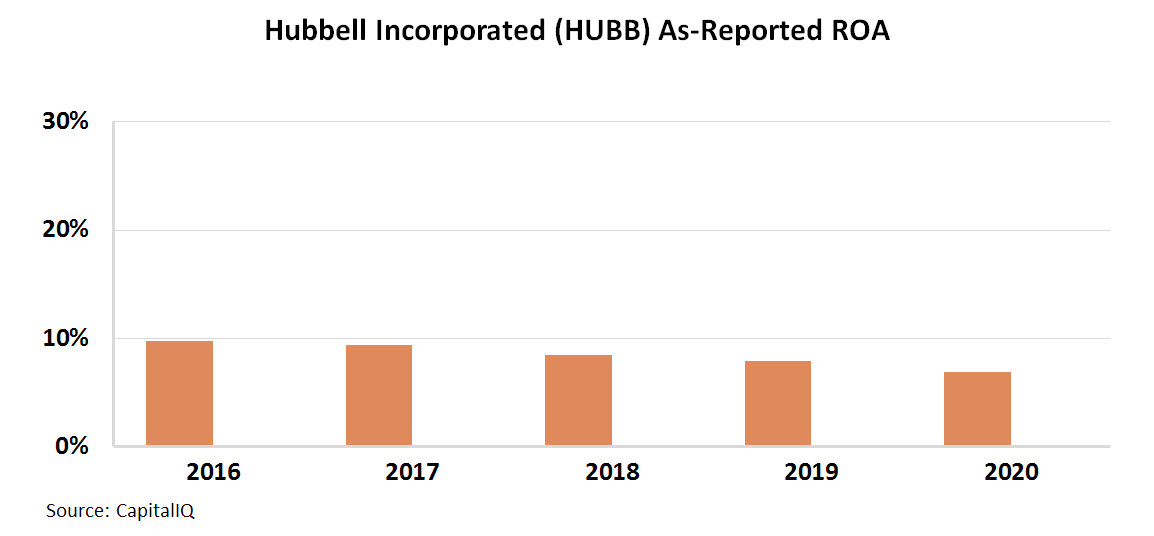

Yet, on an as-reported basis, it looks like Hubbell hasn’t benefited at all from these massive secular growth tailwinds.

The firm’s as-reported return on assets (“ROA”) has steadily declined from 10% in 2016 to 7% in 2020, suggesting a meaningful drop-off in profitability.

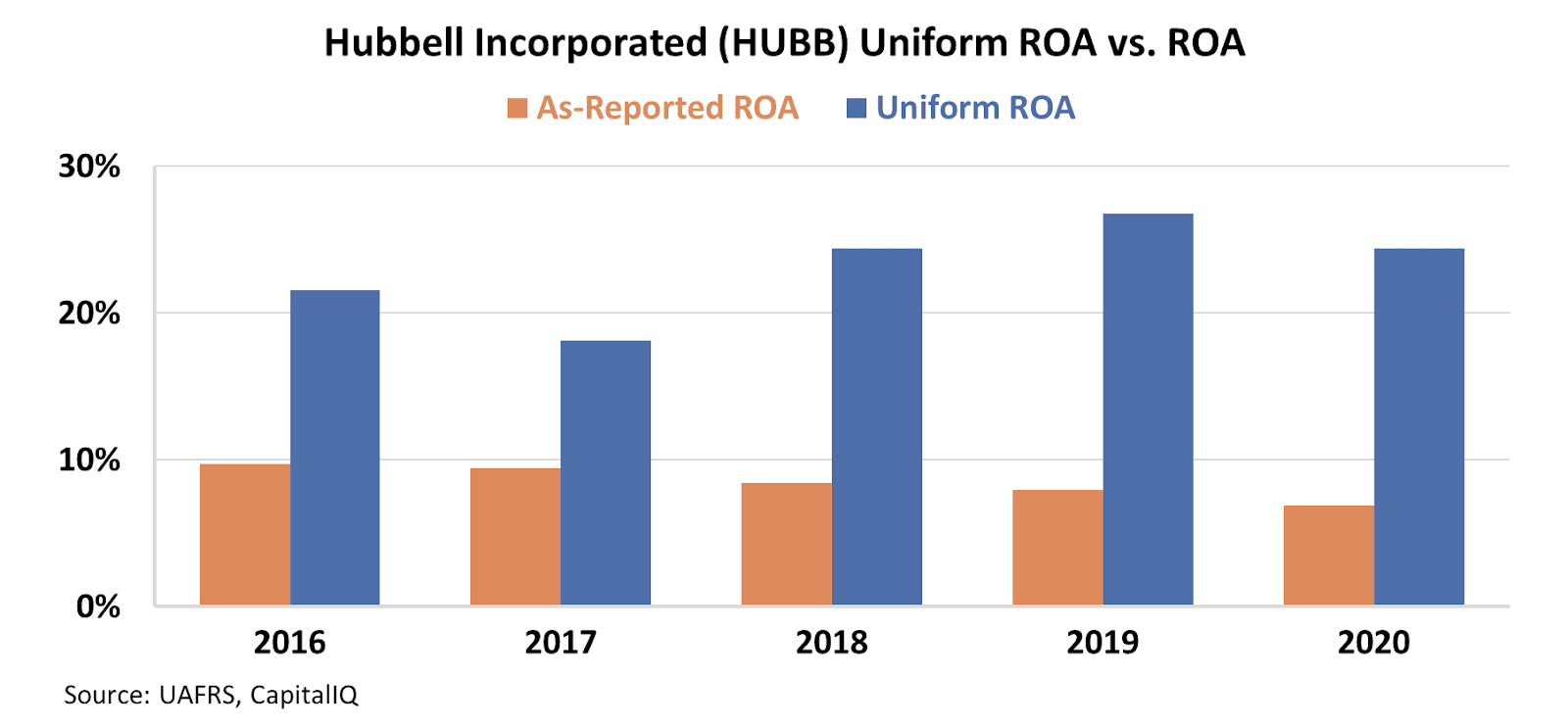

In reality, Hubbell’s exposure to three of the biggest secular growth stories of the next decade are quite clear after accounting for the distortions embedded in as-reported metrics.

Looking at the company through the lens of Uniform Accounting, we can see that its profitability has significantly expanded since 2016, not contracted.

In fact, in 2019, the fiscal year before the pandemic upended comparisons, Hubbell’s Uniform ROA reached record highs of 27%.

As Hubbell continues to ride the massive waves from smart infrastructure, electrification, and the IoT, which are only set to accelerate with the coming capex cycle, its returns are poised to keep on rising.

While as-reported metrics show a company with steadily falling profitability, Uniform Accounting shows the real story, highlighting its ability to spot companies benefitting from the biggest macro tailwinds.

SUMMARY and Hubbell Incorporated Tearsheet

As the Uniform Accounting tearsheet for Hubbell Incorporated (HUBB:USA) highlights, the Uniform P/E trades at 23.8x, which is in line with the global corporate average of 24.0x but above its own historical P/E of 19.1x.

Average P/Es require average EPS growth to sustain them. In the case of Hubbell, the company has recently shown an 8% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Hubbell’s Wall Street analyst-driven forecast is 3% and 14% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Hubbell’s $203 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 3% annually over the next three years. What Wall Street analysts expect for Hubbell’s earnings growth is in line with what the current stock market valuation requires in 2021, but above this requirement in 2022.

Furthermore, the company’s earning power in 2020 is 4x the long-run corporate average. Moreover, cash flows and cash on hand are above its total obligations, and intrinsic credit risk is 100bps above risk free rate, signaling low credit dividend risk.

Lastly, Hubbell’s Uniform earnings growth is in line with its peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research