Horizon Therapeutics’ strategy for developing drugs for rare diseases is more profitable than rating agencies realize

When trying to value a company, we frequently think about the TAM – the total addressable market – as a crucial datapoint.

Yet in the pharmaceutical business, the companies that develop drugs for the rarest of diseases are surprisingly profitable and stable in their cash flows. But for today’s company, the credit rating agencies don’t seem to agree. Let’s use the Credit Cash Flow Prime analysis to prove them wrong.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

When compared to other industries, the world of pharmaceuticals is particularly cutthroat.

This is because drug development pipelines often take five or more years to complete, can cost billions of dollars, and have little guarantee of FDA approval and any return on investment.

Last month’s outrage over the FDA’s questionable approval of Biogen’s (BIIB) new Alzheimer’s drug, Aduhelm, reinforced just how important it is for companies to cross their T’s and dot their I’s during the drug development process. It also showed the crucial role that the FDA plays in balancing the interests of pharmaceutical companies, insurers, and patients.

When we let our analyst team loose on the case, we noticed something interesting about the situation. Biogen was concurrently facing a number of expiring intellectual property protections on their cash-cow drugs. It is quite possible that Aduhelm was pushed through so aggressively because of the looming threat of generics flooding the market and destroying Biogen’s profits.

This just goes to show the important role that patent protections and exclusivity rights play in the pharma world.

Alzheimer’s Disease is one of the leading causes of death in the country. Any company to exclusively sell a drug that works will make unimaginable amounts of money.

But what about diseases that are far less common?

The economics of developing drugs for rare illnesses – called orphan drugs – is unique because it takes so much longer for companies to get paid back for their research and development investments.

For instance, there are about 20 people born with Chronic Granulomatous Disease (CGD) in the United States each year. The total addressable market is 25,000 times smaller than Alzheimer’s disease, which gets about half a million diagnoses each year.

The pipeline cost, however, isn’t 1/25000th of an Alzheimer’s drug.

For this reason, a regulation passed in 1983 granted certain tax rebates and FDA processing cost advantages to orphan drug developers. More importantly, it mandated far longer exclusivity rights than for other types of drugs.

This tends to mean that when a treatment is successful, it produces steady income for some time. Hence, these companies have steady cash flows.

Horizon Therapeutics (HZNP) is one such orphan drug developer. Horizon sells drugs that address the needs of those impacted by rare, autoimmune, and severe inflammatory diseases, including GCD.

Eight years ago, it only offered two treatments. Now, it offers twelve. Moreover, the growth has been accompanied by robust profitability, as Horizon saw returns on assets (ROA) in excess of 40% for four of the past five years.

However, we are once again astonished by how the credit rating agencies underestimate great companies. S&P rates the name as high yield with a “BB” credit grade, which implies a greater than 10% chance of defaulting in the next 5 years.

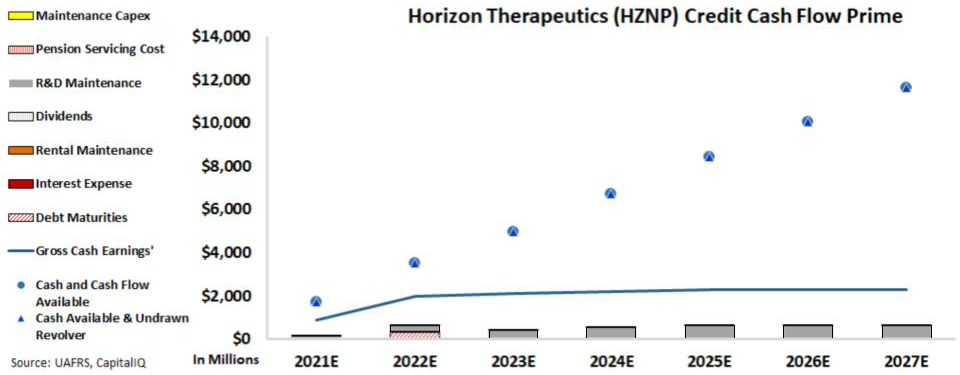

Our Credit Cash Flow Prime (CCFP) framework, which leverages Uniform accounting to correct for the deficiencies of GAAP and soberly evaluate the credit picture for any company, shows a very different picture.

See for yourself below.

The blue dots represent the cash available to the company, while the blue line represents Uniform earnings. The bars represent the set of obligations the Company must pay off in each subsequent year, with the most easily divertible obligations like maintenance capex stacked towards the top, and unbreakable contractual obligations like debt maturities sitting near the bottom:

Not only does Horizon have no debt maturities coming due in the next 5 years, but its cash flows exceed obligations by a healthy margin in each year going forward and its cash on hand will continue to steadily build.

There is no reason to assume that the company has significant default risk. That is why Valens rates the company as a safe IG3+, with a sub-2% default risk.

SUMMARY and Horizon Therapeutics Tearsheet

As the Uniform Accounting tearsheet for Horizon Therapeutics Public Limited Company (HZNP:USA) highlights, the Uniform P/E trades at 16.4x, which is below the global corporate average of 21.9x, but above its historical average of 14.5x.

Low P/Es require low EPS growth to sustain them. In the case of Horizon, the company has recently shown a 437% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Horizon’s Wall Street analyst-driven forecast is a 1% EPS decline in 2021 and a 64% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Horizon’s $105 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 3% over the next three years. What Wall Street analysts expect for Horizon’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power is 14x the long-run corporate average. Moreover, cash flows and cash on hand are 9x its total obligations—including debt maturities and capex maintenance. Together, this signals low credit risk.

To conclude, Horizon’s Uniform earnings growth is above its peer averages and the company is also trading above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research at Valens Research