Barry Diller’s InterActiveCorp looks vulnerable post-pandemic, but there’s more than meets the eye

With the onset of the pandemic a year and a half ago driving a surge in home buying across the developed world, more and more people have spent money on home improvement projects.

Yet, for one company that acts as a digital market maker for professional service providers and consumers looking for home repair and remodeling, as-reported metrics suggest negative profitability.

Today, we use Uniform Accounting to unearth the true operating performance of this business and discover whether its famed owner has lost his touch.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Few people have impacted the entertainment industry over the past six decades as much as Barry Diller, founder and Chairman of the global internet and media company IAC/InterActiveCorp (IAC).

Diller was a key factor behind the success of Paramount Pictures during the latter half of the 20th century, overseeing the studio when it produced massive hits such as the musical comedy Grease (1978) and the sitcom TV series Cheers (1982).

He also founded Fox Broadcasting in 1986, which was the most successful attempt at competing with the big three television networks (ABC, CBS, and NBC) and was smart enough to understand how the internet would completely reshape the media landscape, leading him to accumulate and build online assets ahead of the competition.

These online media assets include online travel shopping company Expedia Group and Match.com, owner of a wide slew of dating websites.

Diller still owns stakes in many of these businesses, worth roughly $3 billion, but his current focus is on running one final part of the powerful portfolio of media assets he has accumulated over the years—home brands.

IAC owns several digital marketplace services that help consumers connect with service professionals for solutions such as home repairs, remodeling, cleaning, and landscaping. These include HomeAdvisor, Angie’s List, and the Handy brands, which cumulatively create a marketplace of demand that matches buyer and seller.

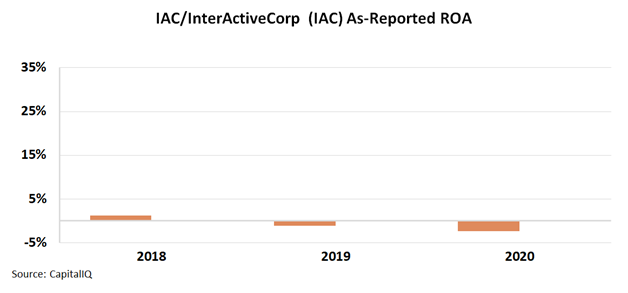

This sounds like a great business to be in, and many people are certainly aware of the strength of the Angie’s List brand. Yet, on an as-reported basis, it looks like the great Barry Diller is struggling with these businesses, with as-reported return on assets (“ROA”) negative over the past two years. This should be surprising to investors since any good company exposed to the At-Home Revolution should have been taking off.

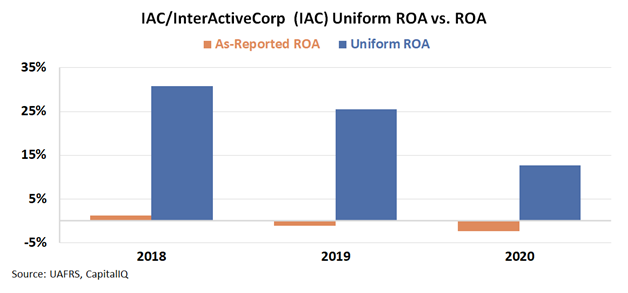

In reality, a deeper look at IAC using Uniform Accounting shows that Diller isn’t holding onto Angie’s List and HomeAdvisor to turnaround unprofitable brands, he’s keeping them because they’re great businesses.

On a Uniform ROA basis, IAC was generating healthy profits in 2018 and 2019, and even with a dip in 2020, it’s still a 13% ROA business, above the corporate average of 12%.

See for yourself…

This suggests Barry Diller hasn’t lost his touch in finding and managing great companies and also demonstrates the importance of viewing a business in a way that truly reflects economic reality.

With as-reported numbers, which are the fruit of GAAP accounting rules, it is impossible for investors to get a real picture of a company’s operating performance. This is because arbitrary accounting rules leave much to the discretion of bookkeepers, distorting a simple understanding of the business.

With Uniform Accounting, which remedies these distortions, we can see that Barry Diller’s media empire is alive and well.

SUMMARY and IAC/InterActiveCorp Tearsheet

As the Uniform Accounting tearsheet for IAC/InterActiveCorp (IAC:USA) highlights, the Uniform P/E trades at 176.1x, which is well above the global corporate average of 24.3x its historical P/E of 35.0x.

High P/Es require high EPS growth to sustain them. In the case of IAC, the company has recently shown immaterial Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, IAC’s Wall Street analyst-driven forecast is a 131% and a 485% EPS decline in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify IAC’s $142 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 24% annually over the next three years. What Wall Street analysts expect for IAC’s earnings growth is below what the current stock market valuation requires in 2021 and 2022.

Furthermore, IAC’s earning power in 2020 is 2x the long-run corporate average. Moreover, cash flows and cash on hand are at 598% of total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

To conclude, the company’s Uniform earnings growth is below its peer averages. However, the company is trading above its average peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research