This family-controlled business is priced for credit problems, Uniform Accounting and compensation analysis shows why markets are wrong

One of our areas of focus at Valens is understanding how Incentives Dictate Behavior. This is the idea that people do what they are paid to do. If we can understand how a management team is compensated, we can understand the likely strategies they are going to pursue.

Today’s company has a single family that owns over a quarter of outstanding shares of the business the family founded. Of course, the family’s direct control is going to have important impacts on what management is directed to do for the business. Understanding this can change our outlook.

Below, we also show Uniform Accounting restates financials for a clear credit profile.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

We regularly talk about the idea of how Incentives Dictate Behavior, how people do what they’re paid to do.

When we discuss corporate incentives, that means understanding how credit issues could impact a company’s strategy.

For example, when a company is close to bankruptcy, management is not likely to focus on the incentive of bonus compensation. Instead, management will manage the company to avoid losing their jobs in bankruptcy. This is what we call debt-driven corporate governance.

Compensation isn’t the only way to think about incentives though. Shareholders also have a direct impact on how management runs the business, especially material shareholders. In particular, this can be relevant when you have large shareholders who have much of their wealth tied up in a business as a founder, because of their many years at the business, or as an activist investor.

An example of this nuance is Ingles Markets (IMKT.A), where the Ingles family owns 27% of the company. With the founding family still holding such a large stake, the firm is likely to largely do what its controlling stakeholder wants.

It also means that since all the Ingles family’s livelihood is tied up with the business, Chairman Robert Ingle and his family are likely to be aligned with creditors in not wanting the company to go bankrupt.

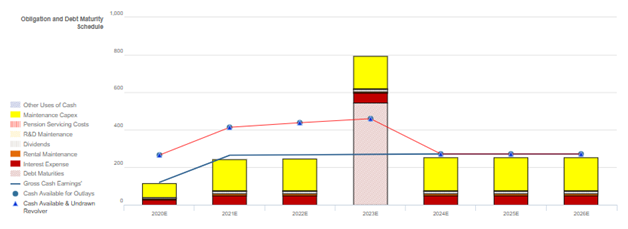

That’s relevant when looking at Ingles’ credit profile. Cash flows consistently match obligations every year except in 2023, where there is a large debt maturity headwall of $545 million.

The company’s credit spreads are somewhat elevated because of concerns about that headwall. The market is spooked about the company’s refinancing risk.

However, considering the family’s concentrated wealth, the Ingles likely have a singular focus on making sure that debt maturity headwall does not create problems. That means management will have a similar focus.

Also, as you can see from the Credit Cash Flow Prime, the firm is at no risk of default for the next three years thanks to its cash balance and cash flow generation. This gives the firm time to refinance its outstanding debt.

Strong liquidity and considerable capex spending also show that Ingles has some flexibility going forward.

Despite all of this, bond yields for Ingles are currently at 5.079%. The market sees Ingles as possibly being unable to pay off their upcoming debt, and has priced it accordingly.

Understanding how the Ingles family and management are motivated helps explain why that does not make sense. It helps us identify that credit yield may be overstating the company’s fundamental credit risk.

Credit Risk Remains Overstated as IMKT.A’s Robust Recovery Rate Continues to be Overlooked

Cash bond markets are materially overstating credit risk with a YTW of 5.079%, relative to an Intrinsic YTW of 3.319% and an Intrinsic CDS of 309bps. Meanwhile, Moody’s is overstating IMKT.A’s fundamental credit risk, with its Ba2 credit rating two notches lower than Valens’ XO (Baa3) credit rating.

Fundamental analysis highlights that IMKT.A’s cash flows should exceed operating obligations in each year going forward. However, the combination of the firm’s cash flows and expected cash build would fall short of servicing all obligations in 2023, when the firm faces a material $545mn debt headwall.

That said, the firm’s robust 187% recovery rate on unsecured debt should allow access to credit markets to refinance when necessary.

Incentives Dictate Behavior™ analysis highlights mostly negative signals for creditors. IMKT.A does not disclose information on management’s compensation framework, making it difficult to understand how well management is aligned in terms of value creation for the business, highlighting risk in the information gap between the firm and investors.

However, although most management members are not material holders of the firm’s equity relative to average annual compensation, Chairman Ingle holds 27% of total IMKT.A common shares outstanding, indicating he may influence other NEOs to align with shareholders for long-term value creation.

IMKT.A’s operational sustainability and robust recovery rate indicate that Moody’s and cash bond markets are overstating credit risk. As such, a tightening of credit spreads and ratings improvement are both likely going forward.

SUMMARY and Ingles Markets, Incorporated Tearsheet

As the Uniform Accounting tearsheet for Ingles Markets, Incorporated (IMKT.A:USA) highlights, the company trades at a 19.4x Uniform P/E, which is below global corporate average valuation levels, but around its historical average valuations.

Low P/Es only require low EPS growth to sustain them. That said, in the case of Ingles Markets, the company has recently shown a 40% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ingles Markets’ Wall Street analyst-driven forecast projects 14% earnings growth in 2020, followed by a 6% shrinkage in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ingles Markets’ $40 stock price. These are often referred to as market embedded expectations.

The company can have minimal shrinkage in Uniform earnings each year over the next three years and still justify current price levels.What Wall Street analysts expect for Ingles Markets’ earnings growth is below what the current stock market valuation requires in 2021.

Furthermore, the company’s earning power is below corporate average levels. However, cash flows and cash on hand will be sufficient to cover the company’s debt maturities in each year going forward, excluding 2023, when the firm faces a material debt headwall.

Together with the company’s intrinsic credit risk being 350bps above the risk-free rate, its earning power and debt maturities signal a high risk to its credit and dividend.

To summarize, Ingles Markets is currently seeing average peer Uniform earnings growth. However, the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research