Improving its community has helped Afya achieve high profitability

Education and healthcare are two essential factors in helping a community advance.

As Brazil looks to continue developing into the next economic powerhouse of the world, it will do so by focusing on healthcare and education.

Afya, a healthcare education company, is at the intersection of both of these needs, and has achieved remarkable profitability through its healthcare education platform.

That’s why this name showed up on our FA Alpha Screen. Its strong profitability, high growth, and attractive valuations make it a compelling company.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

Much of our development as a society has occurred due to a couple of primary factors.

The first, and perhaps more visible, has been the improvement in quality of life due to healthcare. Increases in the average life expectancy have allowed for more productive and enjoyable lives.

Another factor that we sometimes overlook is that much of these advancements have only been possible due to improvements in our education system.

Improving quality and access to education directly leads to a virtuous cycle of job creation and wealth concentration in developing countries.

Perhaps more importantly in helping to advance the community are the societal benefits of increasing access to education. Providing access to education, even if it doesn’t lead to higher education, promotes equality and empowerment while reducing crime and gender-based violence.

Taken together, we can see how critical it is for us to ensure we get the education of medicine right. Without it, we are left with a society that can’t protect the current generation or empower the next generation.

Afya (AFYA) is a great example of a company that is focusing on both. It’s a medical education school in Brazil that focuses on increasing access to care and reducing health disparities within underserved populations.

The company provides services essential to training the next generation of healthcare workers in Brazil.

With such an important role in advancing healthcare and education in Brazil, one might think that Afya is a highly profitable company.

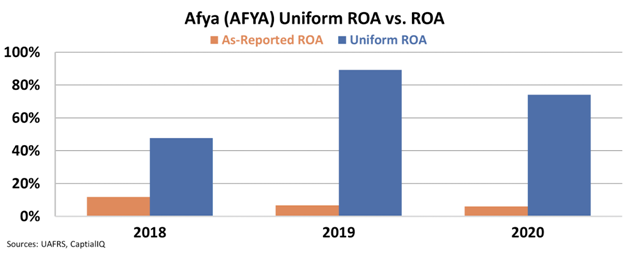

Yet as-reported metrics show that in 2020, even as the demand for healthcare and education surged due to the pandemic, the company had a return on assets (“ROA”) below the cost of capital. In 2020, ROA sat at 6%.

However, Uniform Accounting allows us to see a different picture.

By using Uniform metrics, we see that ROA has consistently outperformed and the company has returned a high ROA. Afya’s ROA in 2020 reached a massive 74% ROA which shows its strength and demand.

As a developing country, the Brazilian government is prioritizing education and healthcare investment and it continues to be a field that sees a strong influx of talent. This outside investment is part of why the company has been growing at robust rates of at least 20% every year.

So as Afya continues to deliver strong healthcare education and Brazil continues to grow, we can expect strong profitability and performance.

But you can only see this impressive performance if you look at the right Uniform Accounting data.

As-reported metrics hide the company’s strong asset strength, which helps to explain why Afya is undervalued with a V/E of 12.9x, well below market averages of 20x.

But this low valuation, combined with high returns and strong growth is what makes Afya such a compelling company, and is why it is such an interesting FA Alpha 50 name.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies, but rather looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

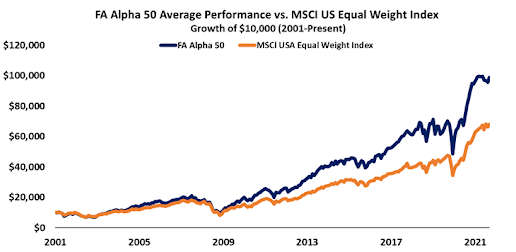

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

If you’re interested in seeing the other 49 names on this month’s FA Alpha, click here to learn more.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research