Ingles Market continues to take advantage of pandemic-driven demand

As the pandemic abates, investors are starting to discount the trends powering many At-Home Revolution names over the past two years.

However, many of the trends established by the pandemic are here to stay. As folks learned to cook over the pandemic, they are likely to continue cooking meals at home in some capacity rather than eating out the same amount, even as they become able to.

Today, we’ll use Uniform Accounting to get to the heart of grocery chain Ingles Market’s true credit risk and decide whether Wall Street has gotten it wrong yet again.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

People remember the early days of the pandemic when everyone swarmed to buy toilet paper from the grocery store. But they often forget about the other ways the grocery store kicked off the at-home revolution.

With restaurants closed for dine-in, many people picked up cooking. Everything from baking sourdough bread to simply learning to cook entire meals from scratch surged in popularity.

This meant a significant jump in demand for grocery stores, and it doesn’t appear to be diminishing any time soon.

For grocery stores like Ingles Markets (IMKT.A), a chain in the southeastern United States, profitability has made great strides.

Ingles Market saw its return on assets (“ROA”) double in the pandemic, jumping from 4% to 8%. It sustained these levels through 2021 and is forecasted to keep going strong.

It seems like food consumption patterns have changed long-term, even after dine-in restrictions were lifted. With more folks buying groceries on a regular basis, chains like Ingles Market are set to have stronger returns for longer.

Yet it looks like the S&P hasn’t gotten the memo, giving Ingles Market a BB rating. A BB rating indicates that S&P thinks Ingles Markets has a 10% chance of going bankrupt in the next few years.

However, we see things differently, especially considering this is a company that saw resiliency in the midst of the pandemic.

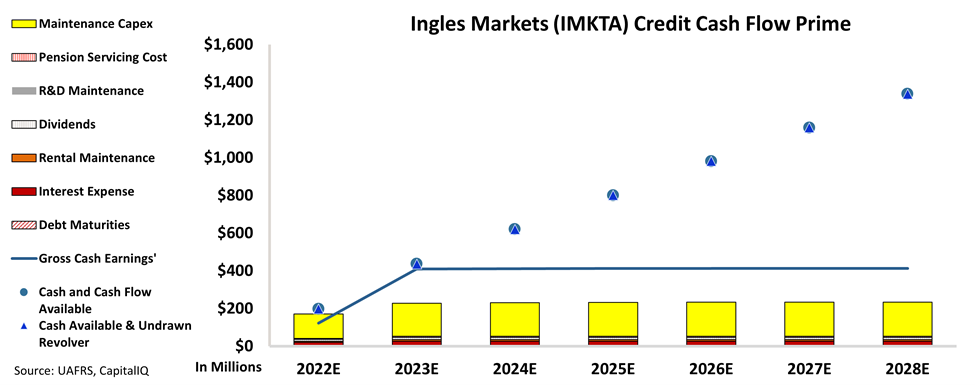

Using our Credit Cash Flow Prime (“CCFP”) framework, we can get to the heart of Ingles Markets true fundamental credit risk.

In the following chart, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As you can see, Ingles Markets has ample cash flow above all earnings for the next seven years. It’s also building a sizable amount of cash, and has barely any debt maturities in the next five years.

Considering its macro tailwinds, Ingles Markets is not the type of company that is a high default risk.

That’s why we rate it with an investment-grade rating of IG3+ and think it is much safer than the ratings agencies believe. An IG3+ rating translates to a less than 2% default risk, which is much more in line with the robust cash flows of Ingles Markets.

Using Uniform Accounting, we can see through the distortions of as-reported numbers to get to the true fundamental credit picture for companies in transition.

To see Credit Cash Flow Prime ratings for thousands of other companies we cover, click here to learn more about the various subscription options now available for the full Valens Database.

SUMMARY and Ingles Markets, Incorporated Tearsheet

As the Uniform Accounting tearsheet for Ingles Markets, Incorporated (IMKT.A:USA) highlights, the Uniform P/E trades at 9.1x, which is well below the global corporate average of 24.0x, but around its historical P/E of 8.2x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Ingles Markets, the company has recently shown 36% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ingles Markets Wall Street analyst-driven forecast is for a 6% EPS growth in 2022 and 1% EPS shrinkage in 2023.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ingles Markets’ $77 stock price. These are often referred to as market embedded expectations.

Meanwhile, the company’s earning power in 2021 is above the long-run corporate average. However, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividend. Additionally, intrinsic credit risk is 70bps above the risk-free rate. All in all, this signals a low credit and dividend risk.

Lastly, Ingles Markets’ Uniform earnings growth is above peer averages, but the company is trading well below peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research