Insider Trading Reveals Recent Trends May Not Be Short-Lived

There’s a website that many institutional investors follow religiously.

It has some of the most valuable information Wall Street professionals can access. It’s so powerful that it can change how these folks view the entire market.

They just don’t talk about it.

This website looks like it hasn’t been updated since Web 1.0. It doesn’t offer any primary research. It doesn’t run highly advanced audio analysis on management’s communication, like our Earnings Call Forensics work.

It’s not exclusive to Wall Street, either. You can access it just as easily as a hedge funder with a seven-figure salary.

And yet, this old, obscure website is one of the best ways for institutional investors – and anyone else who knows about it – to learn what management is really thinking.

We’re talking about secform4.com.

It’s a simple setup. All it does is compile a document that companies file hundreds of times a week, in an easy-to-digest format.

But institutional investors find it invaluable because they understand a key tenet of investing. Whenever you want to understand what management is thinking, the best trick is to follow the money.

Longtime subscribers know we think the most valuable annual filing from all public companies isn’t the 10-K. It’s a proxy filing called the DEF 14A.

The DEF 14A explains how management is compensated. It’s central to our incentives dictate behavior (“IDB”) research, which helps us understand if management really has our back as investors.

The Form 4 gives us another window into management’s thinking. Unlike the DEF 14A, it doesn’t tell us whether or not management is focused on the right metrics. Instead, it tells us if the team is confident it can execute to do what it needs to do in order to push the stock higher.

Any time an insider buys or sells stock in their company, the U.S. Securities and Exchange Commission (“SEC”) requires it to be reported in a Form 4. And whenever a company reports a Form 4, it gets posted on secform4.com.

The website helps give investors transparency. They know if management is unloading stock or scrambling to buy more. That might signal management knows something investors don’t.

It isn’t just useful for individual companies, either. It’s also a powerful tool to understand the outlook for management teams across the economy.

Today, we will explain how investors can understand and use this insider trading information to their benefit.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Secform4.com does not stop at compiling these filings. It also analyzes the results.

The conclusions of the analysis are not surprising most of the time. As a whole, management teams tend to buy stock when it is cheap and sell stock when it is expensive.

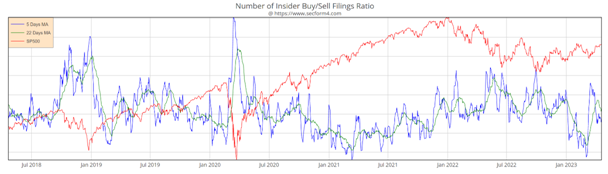

The following chart shows the ratio of daily buy and sell filings from public Form 4 data. A higher ratio means management teams are buying more (and are generally more bullish), and a lower ratio means they are selling more (and are more bearish).

In early 2020, the S&P 500 sank and insider buying skyrocketed. Management teams knew their stocks were cheap and saw it as a buying opportunity.

For the most part, the two lines tend to move in different directions. But every once in a while, something changes. Stocks start dropping, but management isn’t buying anymore. Or stocks keep rocketing higher, and management is still buying aggressively.

When management buys even though stocks are soaring, it is the sound of a slot machine jackpot going off. The getting is so good that these folks want more stock, no matter the price.

When management is not interested in buying shares on the cheap, it is a flashing warning sign. It signals that management teams across all industries are not comfortable with the macro outlook.

Even though the market is dropping, they would prefer to wait and see. They do not want to risk lighting more of their money on fire.

That is exactly what we saw in mid-March. The ratio fell to near its lowest level in the past five years and it got there in a hurry.

However, right after the fall, things changed quickly.

Silvergate Capital (SI), Silicon Valley Bank, and Signature Bank (SBNY) collapsed, taking the market with it. The five- and 22-day moving averages rose quickly as management teams took advantage of the market panic, buying up shares as fast as they could.

The ratio jumped from the bottom to slightly above-average levels in only a week.

Don’t confuse this with your usual market conditions.

Management teams saw an opportunity and they took it.

However, this does not change the overall trend. As the market leaves the bank crisis behind, insider trading is going back to where it was. The moving averages are falling almost as fast as they rose.

We still think the rally to start the year is a “FOMO” rally, not a real one. And management teams seem to confirm this, since they’re not eager to buy today.

Management teams see the mounting headwinds. That means the volatility we have seen in March and April may be only the start.

Expect more of the same for the next few months.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research