The recent restrictions on tech exports could be a huge opportunity for this semiconductor company

The U.S. recently announced new measures on tech exports which will make it extremely difficult for Chinese companies to obtain or manufacture advanced computer chips.

As a result of these restrictions, some semiconductor companies will take a big hit, while some of them will have a huge opportunity.

One of the companies that can benefit from this is none other than Intel Corporation (INTC).

However, the Embedded Expectations Analysis (“EEA”) shows that the market doesn’t recognize the tailwind yet, which creates a significant opportunity for investors.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The U.S. just announced new restrictions on tech exports to China earlier this month, as a part of the continued “economic war” between the two geopolitical rivals.

These restrictions will also prohibit American citizens and companies from providing direct or indirect support to Chinese companies involved in advanced chip manufacturing.

In this situation, some semiconductor companies that supply various products to Chinese firms will take a big hit.

However, there are some companies the market hates right now, but will benefit from this tech nationalism.

One of them is the giant chip maker Intel Corporation (INTC).

Intel has long been one of the most dominant semiconductor companies in the world, but in the last few years, it has fallen behind its rivals.

Right now the company is trying to position itself to become the U.S.’s response against Chinese and Taiwanese companies.

The company announced its plans of massive investments over the next 10 years to build new fabrication facilities and these “Megafabs” could help Intel to return to its good old days.

Considering how Taiwan Semiconductor Manufacturing Company (TSM) utilized these facilities to boost its profitability, Intel could make a big return in the upcoming years as well.

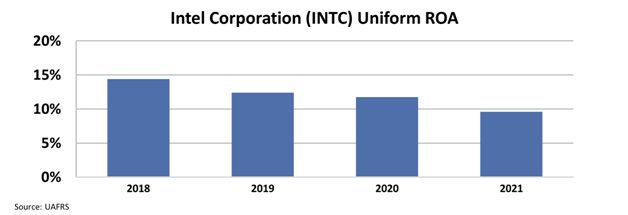

These massive investments and the opportunity from the restrictions could be a significant factor in Intel’s future profitability as the company experienced a declining trend in profitability for the last four years.

Intel’s Uniform return on assets (“ROA”) fell from 14% in 2018 to 9% in 2021.

This declining profitability trend clearly shows that the company needed investments and supportive tailwinds to bounce back, and Intel is trying to do exactly these things.

However, it seems that the market doesn’t recognize the company’s efforts and the opportunity that lies ahead.

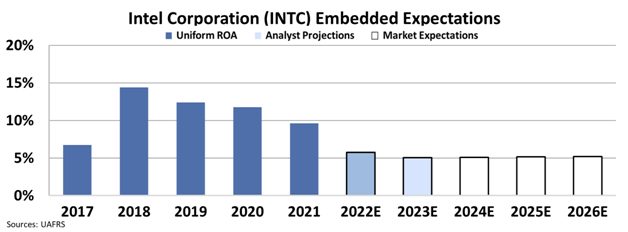

By utilizing our Embedded Expectations Analysis (“EEA”) framework, we can see what investors expect these companies to do at the current stock price.

Stock valuations are typically determined using a discounted cash flow (“DCF”) model, which makes assumptions about the future and produces the “intrinsic value” of the stock.

We know models with garbage-in assumptions based on distorted GAAP metrics only come out as garbage. Therefore, we use the current stock price with our Embedded Expectations Analysis to determine what returns the market expects.

At around $26, the market expects the company to have a huge hit and its Uniform ROA to fall even further to 5%. Wall Street analysts seem to agree with the market.

The Embedded Expectations Analysis shows that the market does not realize the huge tailwind Intel has due to the new restrictions and the company’s “Megafab” investments.

For context, Taiwan Semiconductor’s Uniform ROA is typically around 13%, right above corporate averages. Its lowest Uniform ROA in the last 15 years was 8%.

If Intel’s investments into fabrication help it keep its returns stronger, then the market has the stock totally wrong.

That makes it an interesting opportunity for investors to consider, if they think this fab investment will pay off.

SUMMARY and Intel Corporation Tearsheet

As the Uniform Accounting tearsheet for Intel Corporation (INTC:USA) highlights, the Uniform P/E trades at 22.7x, which is above the global corporate average of 17.8x and its historical P/E of 17.9x.

High P/Es require high EPS growth to sustain them. In the case of Intel Corporation, the company has recently shown a -3% shrinkage in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Intel Corporation’s Wall Street analyst-driven forecast is a -58% and -38% EPS shrinkage in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Intel Corporation’s $27 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 15% annually over the next three years. What Wall Street analysts expect for Intel Corporation’s earnings growth is below what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power in 2021 is 2x the long-run corporate average. Moreover, cash flows and cash on hand are 1.4x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 60bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Intel Corporation’s Uniform earnings growth is below its peer averages, but above its peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research