Meeting the surging demand for advanced testing equipment

The supply chain supercycle is set to bolster manufacturing capacity over the next decade.

This growing manufacturing capacity will necessitate an increased demand for testing equipment, a demand that inTEST (INTT) is well-prepared to meet.

inTEST offers testing and process solutions primarily tailored for the manufacturing sector, with prominent applications in the industrial, semiconductor, automotive, and aerospace sectors.

Furthermore, the company has successfully rebounded from the challenges posed by the pandemic and stands ready to cater to this elevated demand.

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The U.S. is expected to see significant investments in infrastructure and supply chains over the coming years due to various policy initiatives and market forces.

We are in a supply chain supercycle driven by the need to reshore manufacturing and strengthen domestic supply chains. This will require large investments in factories, equipment, warehouses, transportation and logistics infrastructure.

The Bipartisan Infrastructure Bill allocates $1.2 trillion for new infrastructure spending over 10 years, including investments in roads, bridges, ports, and broadband.

The CHIPS Act aims to boost domestic semiconductor manufacturing through $280 billion in incentives. This includes building new semiconductor fabrication plants in the U.S.

Nearshoring production to Mexico and Central America is expected to strengthen regional manufacturing ecosystems and industrial capabilities near the US market.

All these initiatives are stimulating billions of dollars in investments to develop supply chain and manufacturing capabilities in the U.S.

With the manufacturing industry poised for expansion over the coming decade, the need for advanced testing equipment becomes increasingly clear.

inTEST Corporation (INTT) is ideally positioned to meet this surging demand.

The company supplies test and process solutions for manufacturing, mostly used in industrial, semiconductor, automotive, and aerospace industries.

inTEST’s extensive range of equipment and solutions, combined with its well-established industry presence, uniquely positions it as a vital partner for manufacturers looking to uphold the highest standards of product quality and safety.

Furthermore, inTEST has already demonstrated its resilience and adaptability in the face of adversity, having successfully weathered the challenges posed by the pandemic.

As a result, the company stands prepared to meet the elevated demand for its products and services, ensuring that manufacturers have access to the critical tools they need to maintain and expand their production capabilities.

However, the market fails to fully understand the company’s potential.

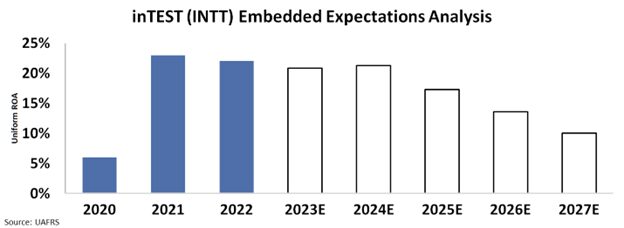

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s Uniform return on assets (“ROA”) to fall to around 10%.

The market’s pessimistic view is caused by not completely understanding opportunities raised by the supply chain supercycle.

inTEST is poised to play a pivotal role in the anticipated manufacturing boom in the U.S., fueled by investments in infrastructure, supply chains, and the semiconductor industry.

With a proven track record and a commitment to innovation, inTEST is well-prepared to provide the testing equipment and process solutions that manufacturing firms will require in the coming years.

SUMMARY and inTEST Corporation Tearsheet

As the Uniform Accounting tearsheet for inTEST Corporation (INTT:USA) highlights, the Uniform P/E trades at 10.4x, which is below its global corporate average of 18.4x, but around its historical P/E of 8.7x.

Low P/Es require low EPS growth to sustain them. In the case of inTEST, the company has recently shown a 18% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, inTEST’s Wall Street analyst-driven forecast is a 5% and 13% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify inTEST’s $15 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 9% annually over the next three years. What Wall Street analysts expect for inTEST’s earnings growth is above what the current stock market valuation requires through 2024.

Furthermore, the company’s earning power is 4x its long-run corporate average. Moreover, cash flows and cash on hand are 4x its total obligations—including debt maturities, capex maintenance, and dividends.

All in all, this signals average credit risk with no dividends.

Lastly, inTEST’s Uniform earnings growth is above its peer averages, but in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research