Investors are doubting this mission-critical pharmaceutical distributor

Last year, an estimated 5 billion retail prescriptions were filled in the U.S.

While buying medication seems relatively simple from a consumer perspective, there’s much more work that goes behind the scenes.

The pharmaceutical industry operates a highly complex supply chain, one that is highly reliant on Cencora (COR).

The company is an end-to-end pharmaceutical distributor that serves both manufacturers and healthcare providers.

Given its mission-critical nature, the company has enjoyed returns hovering above 60% in recent years. That said, it trades at a below-average P/E.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

Millions of individuals across the U.S. have their prescriptions filled daily. It’s estimated that nearly 5 billion retail prescriptions were filled in 2025.

While obtaining medication may seem like a relatively simple task from the perspective of a consumer, there’s a lot more that goes on behind the scenes.

Healthcare providers and pharmacies need access to a reliable supply chain to fill daily prescriptions and source medication from manufacturers.

Meanwhile, manufacturers need storage and transfer solutions to prevent tampering and other problems associated with transport and storage.

And that’s where Cencora (COR) comes in.

Cencora is an end-to-end pharmaceutical distributor specializing in connecting drug manufacturers to pharmacies, health systems, governments, and other healthcare providers.

For manufacturers, Cencora offers logistics, warehousing, drug research and clinical development support, and more.

Meanwhile, provider-specific offerings include wholesale and specialty distribution, practice and clinic solutions, and other related services.

This business model generated $321 billion in revenue in fiscal 2025, a 9% year-over-year bump. This growth was primarily fueled by its U.S. Healthcare Solutions segment which grew by nearly 6% and accounted for 91% of sales.

Management expects revenue to grow further between 4% to 6% for fiscal 2026.

The company has turned to acquisitions to bolster its distribution network further. Earlier this year, it acquired Eyesouth Partners’ retina business for $1 billion, folding it into Cencora’s Retina Consultants of America, a management services organization it acquired in 2025.

Cencora also acquired OneOncology, a platform that specializes in providing support to community-based medical practices across the U.S.

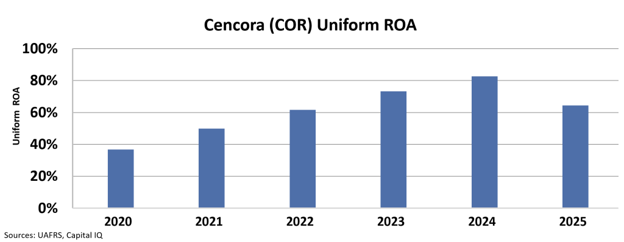

Cencora has generated high levels of returns over the past few years.

As the company continues to grow its business, it has established itself as a highly profitable company.

Since 2020, Cencora’s Uniform return on assets (“ROA”) has climbed from 37% to 64% today, with returns peaking at 83% in 2024.

And Wall Street analysts expect returns to continue climbing, to nearly 150% by 2027. Meanwhile, the market is only forecasting slight improvement from recent levels, projecting returns of 67% by 2030.

This valuation signals investor concerns about margin pressure and regulatory scrutiny.

Cencora’s mission-critical offerings in pharmaceutical distribution should enable it to sustain its returns and support earnings in the next few years, suggesting markets could be overly pessimistic at current valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research