Investors are underestimating this alcoholic beverage firm

The alcohol industry is grappling with softening beer demand due to shifting consumer tastes and tightened spending. In 2025, U.S. beer sales fell 3% and total production hit a decade low.

These industry-wide trends make it seem beer is no longer the cultural force it once was.

However, Diageo (LSE:DGE) – owned Guinness has bucked those trends, as it continues to remain popular among its target demographic.

Yet despite this positive momentum for the company, investors expect the firm’s returns to drop below its historical levels of performance.

Investor Essentials Daily:

Thursday News-based update

Powered by Valens Research

The alcohol industry is facing a demand problem.

According to analytics company Gallup, the share of U.S. adults who drink alcohol fell to 54% in 2025. That’s the lowest reading since Gallup began tracking the data 87 years ago.

Likewise, more breweries closed than opened in 2024. And in 2025, U.S. beer sales fell 3%, and total beer production hit a decade low.

Those trends make it seem beer is no longer the cultural force it once was.

That said, Guinness keeps drawing a crowd.

The World Cup gives pubs a convenient reason to pour more pints of the Irish beer this summer. But the bigger story started long before the tournament. Guinness has become one of the rare old alcohol brands that feels current, social, and surprisingly flexible.

Guinness has always had an obvious drawback, as it takes longer to pour than a standard beer.

The brand’s two-part pour takes close to two minutes, including the first pour with the glass tilted at 45 degrees, a pause for the nitrogen bubbles to settle, and a second pour to finish the creamy head.

Guinness built famous campaigns in the 1990s and 2000s around that waiting period, making patience part of the appeal.

Over the decades, Guinness has leaned into the details that make its pint recognizable and sought after. For example, its parent company, Diageo (LSE:DGE), pushes bars to use clean Guinness-branded glasses.

That has come in handy, because a popular social media trend nowadays is folks trying to “split the G” on a Guinness pint glass. The goal of this drinking challenge is to take a perfect first sip of Guinness so that the remaining beer lines up exactly with the horizontal bar of the “G” in “Guinness” printed on the glass.

Guinness didn’t invent the trend, yet the brand has benefited from people playing with the product in public.

A big transformation for Guinness came in 2019, when Gráinne Wafer took over as Diageo’s global category director of beer. Since then, Guinness has moved from lagging Diageo’s broader portfolio to posting double-digit sales growth.

In the 2025 fiscal year, Guinness sales increased 13%, and the amount of Guinness beer poured rose 14%.

That compares with Budweiser and Corona owner Anheuser-Busch InBev (BUD) and Coors Light owner Molson Coors Beverage (TAP), which saw beer volumes drop 2.2% and 6.4%, respectively, in the first half of 2025. Plus, Guinness is now the top-selling draft beer in both New York and Boston.

On top of all that, demand is high for the nonalcoholic version of the beer, Guinness 0.0. It’s the top-selling nonalcoholic beer in the U.K. And its sales grew by double digits in fiscal 2025, helping Diageo’s nonalcoholic portfolio rise roughly 40%.

Guinness has bucked the broader downtrend in beer consumption and sales. Still, investors don’t seem to expect much from Diageo in the years ahead.

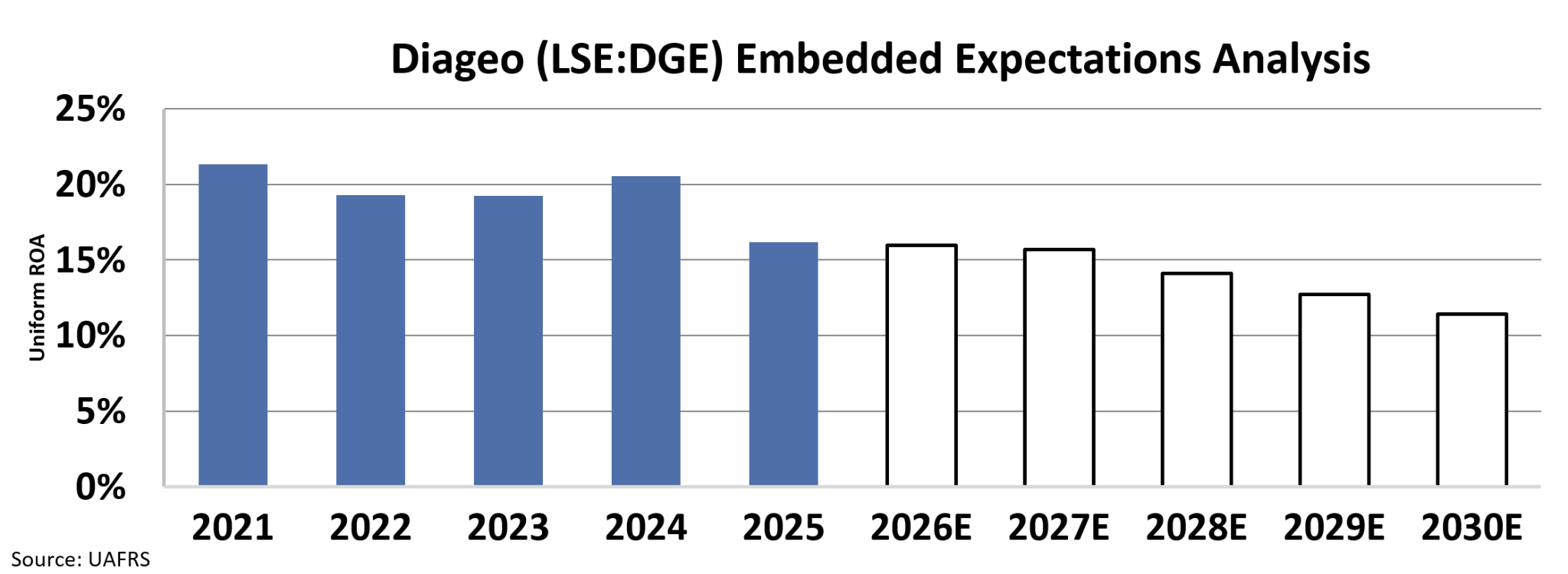

We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Diageo’s Uniform return on assets (“ROA”) used to sit above 20% consistently.

Since COVID-19, it has hovered around the 16% to 20% range. Investors expect the company’s returns to dip below that range.

The market expects Diageo’s Uniform ROA to slide to 11% by 2030, putting the company’s returns below the average U.S. company.

That’s a pessimistic outlook for a business with one of the world’s strongest beer franchises, especially one that has thrived amid an industry slowdown.

To be fair, Diageo still has some work to do across its spirits offerings and North American markets. (Its North American sales just fell about 9% in the quarter ended March 31.)

Guinness proves the company still knows how to build demand, though.

While overall beer consumption is slipping and many brewers are struggling to maintain volumes, Guinness is doing the opposite.

Its beer sales are rising, demand for nonalcoholic Guinness 0.0 is growing rapidly, and the brand continues to gain relevance with younger consumers through social media.

That combination matters for shareholders.Markets often punish alcohol companies as if weakening consumption hits every brand the same way. But Guinness shows that category pressure can make the strongest brands stand out even more.

If Diageo keeps improving investors might have to rethink their pessimistic outlook.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research