Investors are underestimating this health care firm’s potential

Most know the 3M Company (MMM) through brands like Scotch Tape, Scotchgard, and Post-it notes. However, what many don’t realize is that this company used to have a health care segment.

In 2022, 3M announced the spinoff of its health care business which was finalized in 2024, resulting in the creation of a business now known as Solventum (SOLV).

Since the spinoff, the company has operated as a diversified business that’s been able to deliver strong returns.

Despite this, investors expect this company’s returns to fall in the next few years.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

The 3M Company (MMM) is one America’s biggest conglomerates and has exposure in the industrial, worker safety, and consumer goods sectors.

Most know this company through brands like Scotch Tape, Scotchgard, and Post-it notes. However, what many don’t know is that it used to have a health care segment, which was—prior to its divestment in 2022—one of 3M’s best performing businesses, generating nearly 30% of the company’s revenues.

In the past several years, 3M had been marred by controversy and bogged down by litigation, owing to its use of per- and polyfluoroalkyl substances (“PFAS”) which are now known as “forever chemicals”—substances that can cause serious health problems.

As the lawsuits and reputational damage piled up, investors worried about how much 3M would have to pay out in settlement fees, completely ignoring its high-margin business.

In 2022, 3M announced its plans to spin off its health care division which it finalized in 2024, resulting in a business that’s now known as Solventum (SOLV).

Solventum operates three major business units, namely Medical Surgical (“MedSurg”), Dental Solutions, and Health Information Systems.

The MedSurg segment specializes in medical supplies such as bandages, surgical drapes, stethoscopes, wound care, and others. Meanwhile, Dental Solutions focuses on dental care and orthodontic products and equipment. Health Information Systems provides software solutions for hospital-related administrative tasks.

MedSurg is a strong performer for Solventum, as it occupies a 15% market share in the medical equipment space. That said, the Health Information Systems segment is no slouch either.

The U.S. health care system is extremely complex, which makes Solventum’s offering in this space crucial because it ensures hospitals get paid for the work and services they render. Roughly three-quarters of U.S. hospitals rely on the company’s health information software.

The Health Information Systems segment generates 39% margins and is expected to keep growing between 5% to 6% annually going forward. It’s able to generate and sustain those margins because the software it provides is designed to capture recurring revenues.

Solventum’s diversified business has enabled it to generate strong results since its spinoff.

In 2024, Solventum generated a Uniform return on assets (“ROA”) of 30% alongside an asset growth of 11%. And last year, the company posted $8.3 billion in sales, with MedSurg delivering $4.87 billion in sales, followed by Health Information and Dental Solutions at $1.3 billion each.

Despite these strong results, the company currently trades at a below-average P/E of 13x. Moreover, the market expects returns to drop in the next few years.

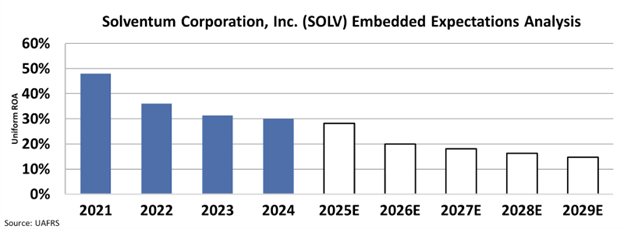

We can see this through Valens’ Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At current valuations, investors expect Solventum’s returns to drop by half, from 30% in 2024 to just 15% in 2029.

Based on these valuations, investors appear cautious about the company’s post-spinoff execution and margin sustainability. However, this assessment largely ignores its ability to sustain and generate returns.

Solventum’s diversified portfolio and recurring demand profile position it to support steady earnings and attractive returns for years to come.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research