Investors are undervaluing F1’s commercial rights holder

Formula 1 is one of the world’s most prestigious sporting events, with a global fanbase of more than 827 million viewers.

While F1 may seem like a fixture in today’s entertainment and sports landscape, it took years to reach the heights it’s reached today.

In the U.S., F1’s ascent to popularity began in 2017, after Liberty Media Corporation acquired the F1’s rights holder, Formula One Group (FWON.K) and aggressively expanded the brand.

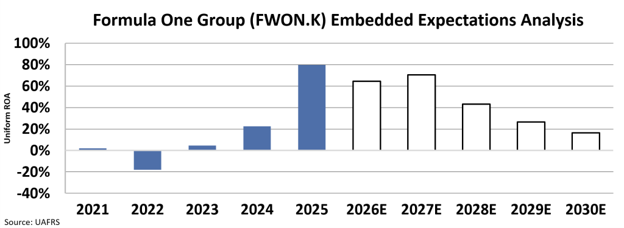

Formula One Group has drastically expanded returns in recent years, from just 5% Uniform ROA in 2023 to 80% in 2025.

That said, investors expect the company’s returns to tail off in the next few years.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

Formula One (“F1”) has slowly emerged as one of the world’s most popular sporting events, experiencing rapid growth in popularity in recent years.

In 2025, F1’s fanbase grew to 827 million, it also set new attendance records, reaching 6.7 million attendees at races, and saw a 33% increase in YouTube viewership. Notably, the company saw an 11% increase in its U.S. fanbase.

F1 races have been held since 1950, and while it enjoys a strong presence in the American market now, the same couldn’t be said more than a decade ago.

The sporting event only recently gained ground in the U.S. after Liberty Media Corporation acquired the F1’s rights holder, Formula One Group (FWON.K), in 2017.

Another factor that led to F1’s rise in popularity and relevance was the 2019 Netflix reality series titled “Formula 1: Drive to Survive” which helped popularize the sport to American audiences during the pandemic years.

F1’s ascent has contrasted recent declines in its largest U.S. rival, NASCAR. In 2025, NASCAR saw a 14% year-over-year viewership decline. F1, on the other hand, saw a 20% year-over-year growth.

An F1 season typically runs from March to December annually, spanning 24 races across 21 countries, providing it with global exposure and media coverage for almost a whole year.

The Formula One Group virtually enjoys a global monopoly over F1 as its commercial rights holder. The company generates its revenue through four primary segments.

Media Broadcasting, which sells broadcast rights to streamers and TV networks, generates the bulk of revenue at 31%.

Meanwhile, Race Promotions, which charges fees to cities and promoters who want to host F1 events, delivers nearly 27% of company revenue.

Sponsorships generate an additional 22% of revenue. This segment enables Formula One Group to monetize F1’s global reach by selling sponsorship rights to giants such as LVMH and Amazon Web Services.

Finally, 20% of revenue comes from ancillary income from direct-to-consumer streaming subscriptions like F1 TV, premium hospitality, licensing, merchandise, and real estate.

The Formula One Group’s diversified revenue streams has enabled it to remain exceptionally resilient and heavily insulated from single-event disruptions.

The company has leveraged its model to substantially grow its returns in recent years. Uniform return on assets (“ROA”) rose from 5% in 2023 to 80% in 2025.

The Formula One Group aims to sustain its returns by monetizing F1’s surging popularity. It recently signed a five-year broadcasting deal with Apple TV worth $750 million. It also inked a sponsorship agreement with LVMH worth $100+ million annually over 10 years.

The company is also doubling down on its “Sprint Races,” an event held the day before an F1 race. In 2021, only 3 races were held. That number is expected to rise 12 by 2027, this presents an opportunity for the company to extract additional revenue from its crowded schedule, which could result in further ROA expansion.

Despite Formula One Group’s ability to deliver strong returns and push for further monetization, investors seem to expect a dropoff in returns in the next few years.

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

After delivering a ROA of 80% in 2025, investors expect returns to drop to 16% by 2030, representing a steep decline in returns.

That is a massive tail off. It also signals investor concerns regarding event disruptions. Due to the fighting in Iran earlier this year, F1 cancelled the Bahrain and Saudi Arabia legs of its 2026 season.

Investors may fear lasting implications of these cancellations and appear to be doubting the company’s ability to replicate and build upon recent success.

Uniform Accounting suggests investors may be undervaluing this business.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research