Investors may want to reconsider withdrawing from this fund

The hedge fund space is tough.

It seems like every day there are headlines of funds locking client deposits, management disputes, or even funds shutting down.

This makes sense as 2022 was the worst year for hedge funds in the last fourteen years. The negative 6.5% returns almost match the industry’s biggest loss in the last two decades, which was a 13% decline during the financial crisis.

In this chaos, one firm stood out for an unfortunate reason. Losses of about 40% caused the withdrawal of $3 billion by investors, in just one year.

It’s also worth noting that the founder of this fund is one of Julian Robertson’s notorious “Tiger Cubs.”

Bad years happen, but these investors didn’t let it slide. However, a strong 2023 could have clients coming back.

Let’s take a look at this tiger cub’s top 15 holdings and gauge whether investors pulled out their money a little too fast.

In addition to examining the portfolio, we include a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Also below is a detailed Uniform Accounting tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Tiger Management was one of the most well-known and influential hedge funds in history.

The fund itself closed its doors in March 2000, but it nonetheless produced some of the most well-known funds and managers in business today. Those who worked at Tiger went on to create their own funds, becoming known as the “Tiger Cubs.”

These cubs were special beyond raw intelligence.

Founder Julian Robertson hired individuals that could add value in different ways, he preferred people that could offer different angles to a story.

And the hiring of Stephen Mandel would attest to that.

Mandel shared a similar start to the likes of Baupost Group’s Seth Klarman and JPMorgan’s Jamie Dimon. Graduates from Harvard Business School who would enter the industry, and quickly find themselves outpacing peers.

Going from Goldman Sachs to Tiger Management as a consumer analyst, it became evident that Mandel understood the industry like no other.

With conviction in his knowledge and experience, Mandel would then initiate the journey of a tiger cub with the founding of Lone Pine Capital in 1997.

Lone Pine started and continues to operate as a long/short equity fund. In simpler words, the fund identifies undervalued and overvalued stocks and hedges them against each other.

While this strategy follows a simplistic framework, the returns can be exponential if executed correctly. And Lone Pine Capital is living proof.

The fund has produced an average annualized return of 15% since its inception. For context, the S&P 500 delivered an annualized return of about 9% in that same time frame. Lone Pine has been beating the market and competitors for a while now.

Most of this success can be attributed to the 249.16% gain between June 2013 and 2023, where the fund reaped the benefits of what seemed to be an everlasting bull market. However, the triple-digit return does not tell the full story.

Lone Pine struggled immensely in the post-pandemic market. From late 2021 to mid-2022, the fund posted losses amounting to 47%, leading it to become the fourth-worst-performing hedge fund in that period.

With such large losses incurred, investors panicked and quickly began withdrawing funds. Clients withdraw an estimated $3 billion through June 2023, causing the AUM to drop about 51% y-o-y.

The series of bad investments and redemptions prompted a strategy shift which was announced in July 2022. Management outlined a shift towards “steady compounders” and the movement away from growth stocks. This repositioning was also accompanied by reduced leverage and increased stake in short bets and “beaten-down equities.”

Despite 2022 being a horrible year, these actions may have stimulated a recovery period in 2023 as the fund is up 12% as of July.

As for the third quarter, Lone Pine’s portfolio has appeared to take a liking to technology equities. Recent purchases of Meta Platforms (META), Alphabet (GOOGL), and Block (SQ) as well as increased stakes in Visa (V) and NVIDIA (NVDA) suggest that the fund may see newfound potential in the space.

In light of a promising 2023 and a portfolio repositioning, let’s take a look at Lone Pine Capital’s top 15 holdings and assess whether these changes will be enough to bring investors’ money back into the fund.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It’s no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in real robust profitability and which may not be as strong of an investment.

See for yourself below.

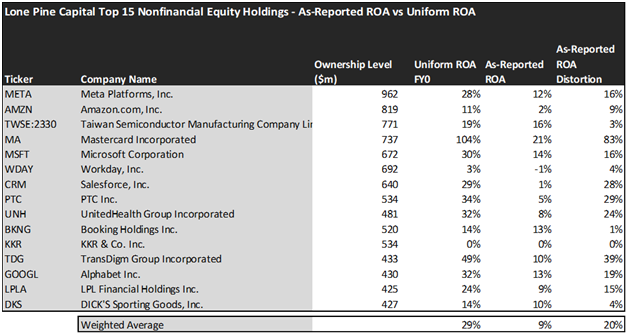

Looking at as-reported accounting numbers, investors would see that Lone Pine Capital invests in low-quality companies.

On an as-reported basis, many of the companies in the fund are notably below-average performers. The average as-reported ROA for the top holdings of the fund is 9%, which is notably lower than the 12% U.S. corporate average.

However, once we make Uniform Accounting adjustments to accurately calculate the earning power, we can see that the average return of Lone Pine Capital’s top holdings is very profitable compared to what as-reported metrics show, coming in at 29%.

As the distortions from as-reported accounting are removed, we can see that Meta Platforms (META) isn’t a 12% return business. Its Uniform ROA is 28%.

Meanwhile, Mastercard (MA) seems like a 21% return business, but this payment processing corporation actually powers a 104% Uniform ROA.

That being said, to find companies that can deliver alpha beyond the market, just finding companies where as-reported metrics misrepresent a company’s real profitability is insufficient.

To really generate alpha, any investor also needs to identify where the market is significantly undervaluing the company’s potential.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

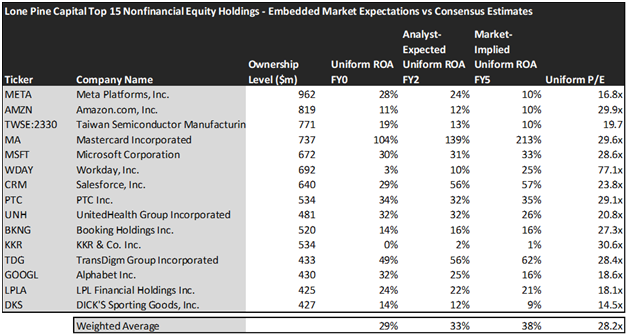

This chart shows four interesting data points:

- The average Uniform ROA among Lone Pine Capital’s top holdings is actually 29%, which is way above the corporate average in the United States.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here are 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, the average Uniform P/E across the investing universe is roughly 20x.

Embedded Expectations Analysis of Lone Pine Capital paints a clear picture. Over the next few years, Wall Street analysts expect the companies in the fund to increase profitability. Similarly, the market has expectations for these companies to exceed current valuations.

Analysts forecast the portfolio holdings on average to see Uniform ROA jump to 33% over the next two years. At current valuations, the market has even higher expectations than analysts and it expects a 38% Uniform ROA for the companies in the portfolio.

For instance, Workday (WDAY) returned 3% this year. Analysts anticipate its returns to increase to 10%. Similarly, the market seems to think optimistically about the company’s future and its pricing in an increase in profitability to reach a Uniform ROA of 25%.

The numbers indicate that 2022 performance may be undermining the potential that Lone Pine Capital’s portfolio presents.

As-reported and Uniform distortions are quite evident in this scenario. One falsely depicts the fund to be a collective of below-average performers, whilst Uniform Accounting paints a picture of a fund that understands the importance of holding highly profitable companies.

Analyzing market and analyst expectations reinforces this idea. Expectations for this portfolio are a jump from 29% levels to a ROA of 38%, within the next five years. This may limit upside as these companies are already being priced in for growth. However, it is also indicative that Lone Pine Capital understands the benefits of high-quality firms.

The thing that stands out the most though is the different angles the fund has in exposure to Artificial intelligence (“AI”).

From a software and innovation perspective, the fund is holding three of the biggest players in the space: Meta Platforms (META), Alphabet (GOOGL), and Microsoft (MSFT). On the manufacturing side, the fund holds a large semiconductor player—Taiwan Semiconductor (TWSE:2330). Lastly, from a retail and application standpoint, companies like Amazon (AMZN), Salesforce (CRM), and Mastercard (MA) are all corporations that would benefit tremendously from AI automation and are likely to implement AI tools into their services.

This portfolio appears to cover all sides that could benefit from AI technology.

There are various different stances on AI and its abilities. At the end of the day, it’s clear that AI is a secular growth story. Sentiment may come and go a bit but the top guys are still being fueled by the potential.

The AI boom has stimulated the economy over the last few years, and it appears that Lone Pine is deciding it’s time to ride the wave.

Yes, 2022 was bad but that very well could just be a one-off outlier. The fund has potential, and the story is being heavily driven by technological advancements.

Investors were panicked but a strong start in 2024 may convince doubters that Lone Pine Capital is back to its old self.

This just goes to show the importance of valuation in the investing process. Finding a company with strong profitability and growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which has not been fully priced into their current prices.

To see a list of companies that have great performance and stability at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of one of Lone Pine Capital’s largest holdings.

SUMMARY and Workday, Inc. Tearsheet

As one of Lone Pine Capital’s largest individual stock holdings, we’re highlighting Workday, Inc.’s (WDAY:USA) tearsheet today.

As the Uniform Accounting tearsheet for Workday, Inc. highlights, its Uniform P/E trades at 77.1x, which is above the global corporate average of 18.4x, but below its historical average of 141.3x.

High P/Es require high EPS growth to sustain them. In the case of Workday, Inc., the company has recently shown 58% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Workday, Inc.’s Wall Street analyst-driven forecast is for EPS to grow by 250% and 36% in 2024 and 2025, respectively.

Furthermore, the company’s return on assets was 3% in 2023, which is below the long-run corporate averages. Also, cash flows and cash on hand consistently exceed its total obligations—including debt maturities and CAPEX maintenance. These signal low operating risk and low credit risk.

Lastly, Workday, Inc.’s Uniform earnings growth is above peer averages, and in line with peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research