This firm’s stable cash flows may point to a cataclysmic “Minsky Moment” and for once, equity holders are more concerned than creditors

The “Minsky Moment” refers to the tipping point that causes longer periods of cash flow stability to lead to more leverage-driven severe volatility in the market collapse that follows.

This firm’s high leverage and stable cash flows point to a scenario like the aforementioned phenomenon, but credit and equity investors seem to have wildly different opinions about the likely outcomes for this firm.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Prominent economist, Hyman Minsky, theorized that any bullish speculation that lasted long enough would lead to a market collapse.

Shortly after his death, his name was used to describe the tipping point at which a sudden decline in market sentiment led to a financial crisis. The “Minsky Moment” became a prominent phrase used during the Asia Debt Crisis of 1997, as well as in the Great Recession, just over a decade later.

Bull markets are often seen as times of economic prosperity, with stable cash flows and open lines of credit. Minsky theorized that longer bull runs and periods of seeming stability would lead to more severe and more volatile collapses, when cash flows eventually faltered.

The catalyst behind the volatility was simple: leverage. As periods of stability extend, more retail and institutional investors would take on debt to finance their speculation and corporations and consumers will do the same. Eventually, however, once this euphoria became unsustainable, the additional credit risk would bring with it a much worse downside.

As such, leverage can be a pressing concern, especially as stability reaches its end.

For over more than a decade, specialized REIT Iron Mountain (IRM) has seen remarkably stable returns, with Uniform return on assets (ROA) ranging between 7%-10% levels. As such, the firm has grown to expect stable cash flows, and over the years, has taken on significant debt, with a debt/EBITDA ratio hovering around 5.5x.

Debt investors assume that the storage of both paper and other products—Iron Mountain’s specialties—along with digital storage, will be a remarkably consistent business.

In fact, due to the ever-expanding amount of paper and the ongoing need for regulatory compliance and information security, the firm’s offerings seem to have the potential to continue their stability going forward.

This sentiment among investors can be seen by looking at the firm’s low bond yields, even with the company’s high leverage and climbing debt obligations. For reference, Iron Mountain’s bonds, expiring in 2025, trade at a YTW near 4.700%.

The debt investors may be right about the continued stability of the firm’s cash flows going forward. They have been so far. However, equity investors are pricing in something completely different.

It seems that equity investors may be more concerned about the potential of a “Minsky Moment” for the firm, as they are demanding a much higher dividend yield from their stocks than bond investors are demanding for their bonds.

Equity investors’ heightened concerns have led to a dividend yield that has surpassed 9%, nearly double the yield bond investors can expect. It seems that the two sides have wildly different expectations for the firm.

Ultimately, in the long-run, only one group of these investors can be right. The yields of these two securities should eventually converge.

Instead of siding with the bond investors or siding with equity investors and risk being on the wrong side, prudent investors can use this opportunity to initiate a pair trade, buying both the bond and the stock.

This allows for a near-riskless approach to take a yield on this REIT, and reap the benefits of being an investor that isn’t tied to a single asset class.

Credit Markets are Understating IRM’s Credit Risk, While the Bond Markets are Overstating Credit Risk

CDS markets are understating IRM’s credit risk with a CDS of 180bps relative to an iCDS of 272bps, while cash bond markets are grossly overstating risk with a YTW of 6.412% relative to an Intrinsic YTW of 2.832%.

Meanwhile, Moody’s is understating IRM’s fundamental credit risk, with their speculative Ba3 rating three notches higher than Valens’ HY2- (B3) credit rating.

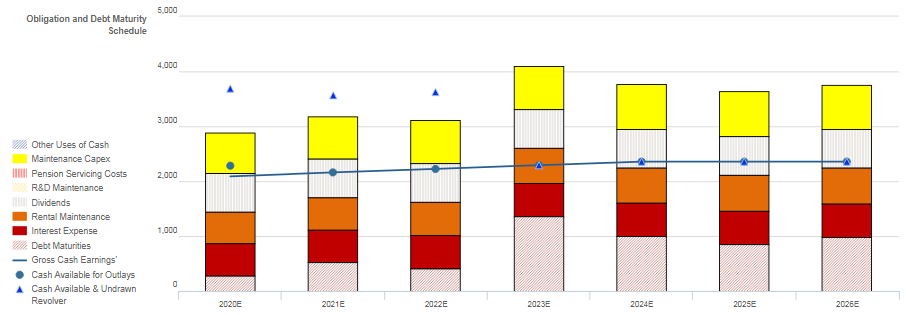

Fundamental analysis highlights that IRM’s cash flows would fall short of operating obligations in each year going forward. Moreover, the firm’s combined cash flows and cash on hand would fall short of servicing all obligations including debt maturities, starting in 2020, when the firm faces the first of a series of consistent, material debt headwalls.

In addition, although the firm has some capex and rental expense flexibility to free up liquidity in the short-term, IRM will have to refinance to avoid a liquidity crunch. That said, despite a lackluster 20% recovery rate on unsecured debt, the firm’s sizable market capitalization and history of successful refinancing should allow them to access credit markets to do so.

Incentives Dictate Behavior™ analysis highlights mixed signals for credit holders. IRM’s management compensation framework should drive them to improve all three value drivers: top-line growth, asset efficiency, and margins. This should lead to ROA expansion and increased cash flows available to service debt obligations.

In addition, management has low change-in-control compensation, indicating they are unlikely to seek or accept a buyout or takeover, limiting event risk for credit holders. However, management is not penalized for taking on excess leverage and overspending on assets to finance growth.

Furthermore, most management members are not material owners of IRM equity relative to their annual compensation, indicating they may not be well-aligned with shareholders for long-term value creation.

Consistent debt headwalls and a lackluster recovery rate indicate that CDS markets and Moody’s are understating credit risk, while a sizable market capitalization suggests that bond markets are overstating risk. As a result, a widening of CDS spreads, a ratings improvement, and a tightening of bond spreads are all likely going forward.

SUMMARY and Iron Mountain Tearsheet

As the Uniform Accounting tearsheet for Iron Mountain Incorporated (IRM:USA) highlights, the company trades at a 22.4x Uniform P/E, which is in line with global corporate average valuation levels but is below its historical average valuations.

Moderate P/E’s only require moderate EPS growth to sustain them. That said, in the case of Iron Mountain, the company has recently shown a 10% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Iron Mountain’s Wall Street analyst-driven forecast projects 28% growth in earnings in 2020 followed by 3% shrinkage in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $24 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for Iron Mountain, the company would just have to have Uniform earnings grow by 9% each year over the next three years.

Wall Street analysts’ expectations for IRM’s earnings growth are below what the current stock market valuation requires in 2021.

Meanwhile, IRM’s Uniform earnings growth is above peer average levels, yet the company is still trading below peer valuations.

In addition, the company’s earnings power is 1x corporate averages. Furthermore, total obligations, including debt maturities, maintenance capex, and dividends, are above total cash flows, signaling an average risk to its dividend or operations.

To summarize, IRM is expected to see above average Uniform earnings growth in 2020, which is expected to decline in 2021, falling short of market expectations.Therefore, as is warranted, the company is trading below peer valuations.

All the best, as always

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research