It Took a Maverick to Uncover This 7x Return Investment

When Mark Cuban bought the Dallas Mavericks on January 4, 2000, the team had had a 240-550 record the prior 10 years.

Through the entire 1990s, the team went to the playoffs once, in 1990. They lost all 3 games in that playoff series. Mavericks fans had not seen a playoff win in over a decade when Cuban bought the team.

And yet, Cuban paid an eyewatering $285 million for the franchise. At the time, no one had ever bought an NBA franchise for more than $200 million. His acquisition raised more than a few eyebrows.

Who buys one of the most poorly run franchises in the league, in a football town, for 40%+ more than anyone had ever paid for another NBA team?

But Cuban understood something important..

The Mavericks’ worth had nothing to do with their record the past 10 years. What would matter is the potential growth drivers he could unlock in the business going forward.

That would determine whether he was overpaying for a trophy asset, or he was as savvy with this purchase as he had been in building Broadcast.com and selling it to Yahoo for $5 billion.

Cuban was an avid basketball fan. He had courtside seats next to the Mavericks bench before he ever became an owner. He had done his research. He could see opportunities to unlock, to justify the value of his investment.

He saw where he would drive growth in the business, and how he could make a significant return on his investment. He was confident in betting on growth when others were just focusing on valuing the business as it was.

He started by focusing on filling up the arena. He sold seats in the nosebleeds for $8 a game to get people in the door. He knew he’d make up the money on concessions. He raised the high demand courtside seat prices 10x, from $200 a seat to $2,000. People still came, they wanted to be on TV.

Importantly, he also invested in the team itself. The way to make real money on the team wasn’t to starve the product and wait to make money on the broadcasting and ticket sales as they stood today, it was to drive growth in all sides of the business by investing to facilitate that growth.

The team had a core of Steve Nash and Dirk Nowitzki, who had both joined the team prior to Cuban buying the team. He surrounded them with the players they needed. When the team needed rebounding, he brought in Dennis Rodman, the seven-time NBA rebounding champion.

His investment yielded a return on the court. The following 10 years, the Mavericks didn’t have a losing season. They won the NBA championship in 2011. But just as importantly, his investment benefited the business’ ability to throw off revenue.

He also had great timing. Cuban purchased the team just when the industry he had made his money in, media and the internet, were making the league more international. They were also making overall fan engagement in the league stronger.

This meant bigger broadcasting deals, and new lines of revenue for the league as a whole. Lines of revenue that would trickle down to the Mavericks.

Cuban’s focus on investing in growth in the business, and his timing in riding a macro wave have led to the Mavericks value rising to $2.3 billion today, according to Forbes. That’s a 7x+ return for Cuban from his investment 19 years ago.

That is the kind of return you only can generate if you are comfortable betting on growth.

Buying a value stock, a company that is trading at 50% of its intrinsic value, can lead to a stock doubling. But its almost impossible to find a company that is intrinsically undervalued 7x what it is worth, based on current cash flows.

Only by finding investments that can transform their cash flows, can one generate 7x returns.

Few investors have more impressive track record finding growth investments than Richard Driehaus. For context, in the 1980s, a dollar invested in the Russell 2000 would have turned into $4.65. For Driehaus’ fund, that same $1 would have turned into $24.65. That’s a 5x higher return.

He’s kept on producing returns like those since.

Ever since Driehaus read John Herold’s America’s Fastest Growing Companies he’d embraced the idea that the best way to find companies that could massively outperform was to find companies who could grow.

As Driehaus himself has said:

“One market paradigm that I take exception to is: buy low and sell high. I believe far more money is made by buying high and selling at even higher prices.”

Driehaus doesn’t trouble himself with P/Es. If a P/E is high, but the earnings growth means the company can deliver, and already is showing strong results, his fund will jump in.

He doesn’t spend his time understanding what the company is worth and if its intrinsically undervalued. He focuses on if the company has positive operating momentum, and the ability to drive growth that can look like Cuban’s 7x return… or more.

Said differently:

“I believe you make the most money by hitting home runs, not just a lot of singles.”

- Richard Driehaus

Driehaus understood, and his firm still understands, that traditional valuation metrics, and the traditional valuation process for those who use as-reported accounting metrics, is deeply flawed. And so they focus on identifying companies that those methodologies have missed.

One of Driehaus Capital’s flagship funds is the Driehaus Small Cap Growth Fund. While as-reported methodologies may distort these companies performance, looking at Uniform Accounting analysis can start to unlock the power of Driehaus’ strategy.

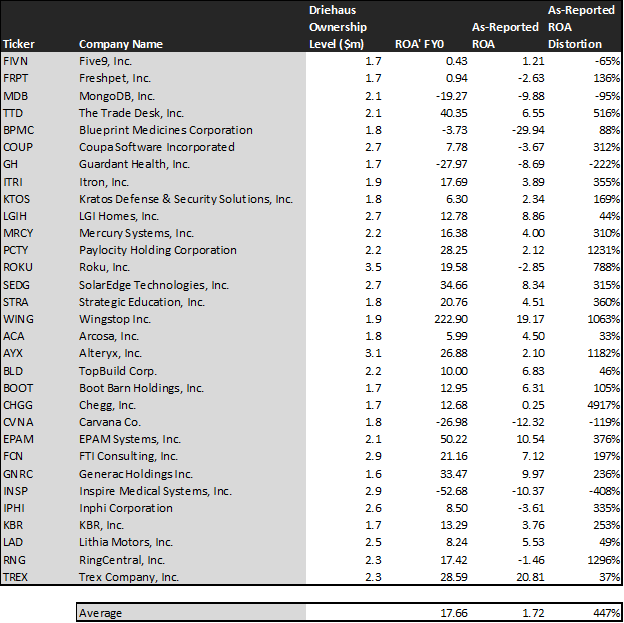

To show what we mean, we’ve done a high level portfolio audit of the Small Cap Growth Fund’s current portfolio, based on their most recent 13-F. This is a very light version of the custom portfolio audit we do for our institutional clients when we analyze their portfolios for torpedos and companies they may want to “lean in” on.

Using as-reported accounting, investors would be scratching their heads at the companies that Driehaus is buying. How can they think that these companies are good growth candidates, when these companies cannot even earn cost-of-capital returns. On an as-reported basis, these companies average a 2% return.

Growth in below cost-of-capital return businesses is value destructive. This isn’t the type of growth that the market would reward. If the Driehaus funds invested in poor performing companies, they wouldn’t be able to produce the outsized returns they are known for.

But once we make Uniform Accounting (UAFRS) adjustments, we realize that the returns of the companies in Driehaus’ portfolio are much more robust. Once we make these adjustments, Roku doesn’t have a -3% ROA, the company’s operating return is really almost 20%. RingCentral doesn’t have a -1% return, its really 17%.

If Driehaus was looking at as-reported metrics, they would never pick most of these companies, because they look like bad companies, and poor investments. Not viable platforms to build growth of of. For the average company, as-reported ROA understates profitability by almost 90%. Uniform ROA is 450% higher than the distorted as-reported metrics.

That being said, there are some companies that Driehaus might need to do greater research on. Uniform Accounting shows these companies are poor performing companies that may not be the growth engines the fund is looking for.

Two that jump out are Inspire Medical Systems, who doesn’t have a -10% ROA, they have a -53% return. Similarly, Five9 is still a below cost-of-capital return business, even after making Uniform Accounting adjustments.

But Driehaus isn’t just finding companies where as-reported metrics mis-represent a company’s real profitability. The reason Driehaus has such phenomenal returns is because they’re identifying companies with good businesses with massive growth opportunities.

This is where Driehaus’ goal of buying high and selling higher comes into play.

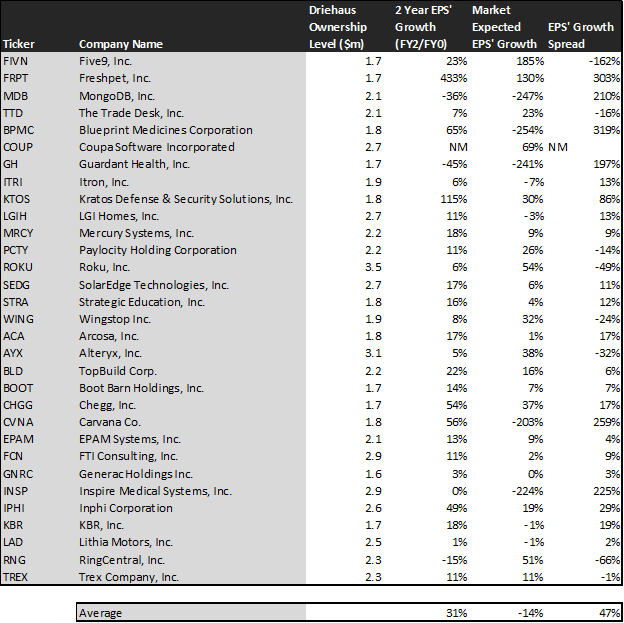

This chart shows three interesting datapoints:

- The first datapoint is what earnings growth is forecast to be over the next two years, when we take consensus Wall Street estimates, and we convert them to the Uniform Accounting framework. This represents the earnings growth the company is likely to have, the next two years

- The second datapoint is what the market thinks earnings growth is going to be for the next two years. Here we are showing how much the company needs to grow earnings by in the next 2 years, to justify the current stock price of the company. If you’ve been reading our daily and our reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for earnings growth

- The final datapoint is the spread between what the company could do, if the Uniform Accounting adjusted Wall Street estimates are right, and what the market expects earnings growth to be

The average company in the US is forecast to have 5% annual Uniform Accounting earnings growth over the next 2 years. The Driehaus fund is identifying companies that are growing 31% a year the next 2 years, on average. The fund is clearly meeting their growth mandate on a Uniform Accounting basis.

For context, this is even above their average as-reported EPS growth forecast, of 28% a year.

But not only is Driehaus Capital identifying companies that have stronger EPS growth than the average US company on a Uniform Accounting basis, they’re finding companies where the market is mispricing that earnings growth.

On a median basis, the market is pricing these companies to have a 9% earnings growth number. On both an average and a median basis, the market is massively understating how much earnings growth these companies will have.

These are the kind of companies that don’t just double, they produce 7x returns or more.

One example of a company in the Driehaus portfolio that has massive growth that the market is mispricing is Kratos (KTOS). Kratos is forecast to have 115% Uniform earnings growth, but the market is only pricing the company to have 30% earnings growth each year the next two years. That is a massive pricing dislocation the market is going to have to react to.

On the other hand, there are some names we’d recommend Driehaus review in their portfolio if we were meeting with their PMs. Two that jump out are Five9 (FIVN) (again) and The Trade Desk (TTD).

For Five9, not only are they a low return business, but the market is pricing the company for 185% annual earnings growth, when the company is only forecast to have 23% annual earnings growth.

Similarly, the market is pricing The Trade Desk to have 23% earnings growth going forward, when the company is only forecast to have 7% earnings growth. This does not look like the type of company that the Driehaus team would want to be owning once we see through the accounting noise.

But for the most part, Driehaus gets it right. And they get it right because they’re not trusting the as-reported accounting statements. Their focus on understanding growth better than anyone else is likely to continue to power strong returns and our Uniform Accounting portfolio review shows it.

We’re Relaunching Our Portfolio Audit Review Offering – And Making A Special Offer

For our institutional clients, we don’t just provide access to our Valens Research app. We also do bespoke research. We produce one-off deep-dive company analyses using all our tools, including Uniform Accounting, credit work, and our management compensation and earnings call analysis. We monitor their portfolios for potential Uniform Accounting signals to alert them. We provide custom datasets for quantitative analysis, and provide aggregate analytics. We also help them create unique idea generation screens that are customized to their approach, using Uniform Accounting and our other analytics.

But for most of our institutional clients, the analysis that they find most useful, and almost universally ask for, is a quarterly portfolio audit and call with our analysts.

Our institutional clients pay a significant premium for all our bespoke research. Some of our institutional clients have paid well over $100,000 a year for our uniquely tailored Uniform Accounting research, because of the value it adds to their process.

Until Thanksgiving, we’re making a special offer.

For any investor that buys access to the Valens Research app ($10,000/year subscription), we will include an Institutional-level portfolio audit and call with our analyst team with no extra charge.

Also, for those people who sign up to the offer before November 1st, we’ll include lifetime access to all of our newsletters, including our Market Phase Cycle and Conviction Long Idea List (a $6,000 value), for no extra charge, for as long as you remain a Valens Research app subscriber.

We want to help show you how powerful Uniform Accounting research can be for your investment strategy.

If you want to hear more about this offer, or are interested in subscribing, feel free to reply to this email. I’ll forward on your note to our head of client servicing. Or, feel free to reach out to Doug Haddad, the head of our client relations team, at doug.haddad@valens-securities.com or at 630-841-0683.

To read more about the offer and sign up, you can also click here – and read about another investing great, Seth Klarman..

Today’s Tearsheet

Today’s tearsheet is for Disney. Disney trades at a slight premium to the market. At current valuations, the market expectations are for negative Uniform EPS growth, and growth significantly below last year’s levels. The company’s forecast earnings and valuations are in line with peers, but the company has robust profitability and no risk to its dividend yield.

Regards,

Joel Litman

Chief Investment Strategist