Publishing is dying, but Uniform Accounting shows this name might be able to buck that trend

Print publishing is a dying industry and at first glance, it looks like all of the players in it are circling the drain. This includes a niche player that many might recognize as a leading player in its market.

It is famously difficult to buck the trend of your overall industry, but digging past the as-reported financials suggests this company might be doing just that.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

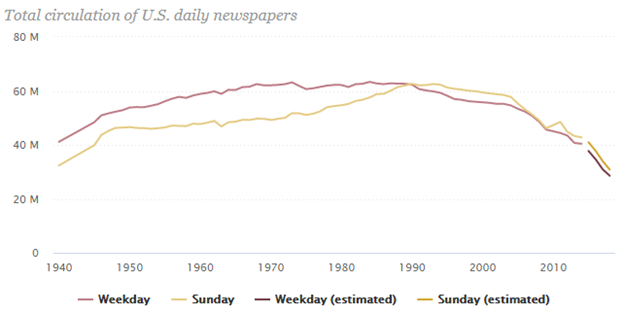

The print publishing industry is dying.

After peaking at over 60 million in the 1990s, daily US newspaper circulation has fallen by over half, to sub-30 million recently. The below chart from the Pew Research Center highlights just how steep that decline has been:

It isn’t contained to just print news, either.

The Association of American Publishers highlights that paperback and mass market book sales were down 8% in 2019, hardback down 1%. Pew also highlighted massive declines in ad pages in top tier magazines as early as the beginning of this decade.

In this environment, it is no wonder to investors why a name like John Wiley & Sons has struggled. In fact, returns for the firm have fallen from 9%+ pre-Recession, to 7% at the beginning of the decade, to just 5% currently:

The firm is focused on publishing, and it is hard to have success when you’re in a dying industry.

But this isn’t really the whole story for Wiley.

In reality, it is focused on protecting a small niche of the publishing world, and moving their solutions online. Wiley owns a large part of the educational and research-based publishing world, and anyone who recently graduated college, or has kids there now, will tell you the firm is also part of the online learning oligopoly.

So that begs the question, why has Wiley struggled to sustain profitability? If it effectively owns a very lucrative niche in the market but is still earning nothing, does that mean the whole publishing sector is dead?

No. The data just misses the mark.

In reality, the firm has sustained over 20% returns historically, and in recent years, profitability has actually expanded:

The market hasn’t recognized this yet, though, and JW.A shares have lagged significantly recently. Investors looking at the as-reported financials think this is a dying business, and that it will continue to bleed money until it eventually fades like other peers have. Although management appears to have concerns about near-term fundamentals, it appears Wiley is going to be able to buck those negative industry trends over the long-term.

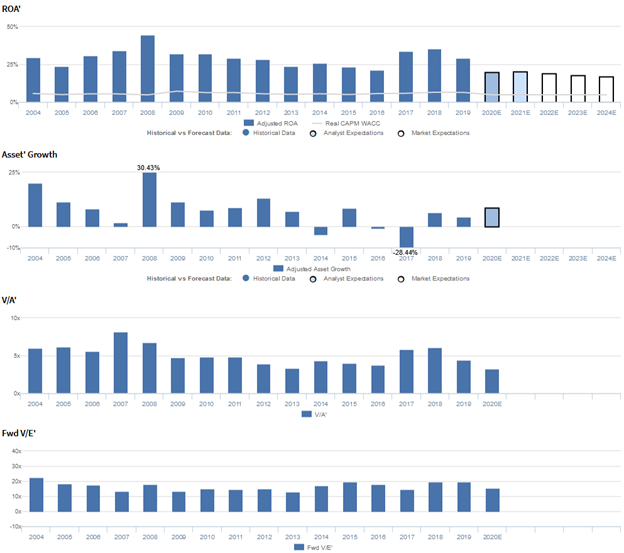

John Wiley & Sons, Inc. Embedded Expectations Analysis – Market expectations are for further compression in Uniform ROA, and management may be concerned about margins, Education Services, and their network

JW.A currently trades below corporate averages relative to Uniform Earnings, with a 16.1x Uniform P/E (Fwd V/E’).

At these levels, the market is pricing in expectations for Uniform ROA to compress from 29% in 2019 to 18% by 2024, accompanied by immaterial Uniform asset shrinkage going forward.

Analysts have similar expectations, projecting Uniform ROA to fall to 19% by 2021, accompanied by 8% Uniform asset growth.

Historically, JW.A has seen cyclical profitability. After the turn of the century, the firm saw Uniform ROA decline from 30% in 2004 to 24% in 2005, before improving to 45% peaks in 2008.

However, following the 2007 acquisition of Blackwell Publishing, Uniform ROA faded to 21% by 2016, and subsequently expanded to 35% in 2018, before sliding to 29% in 2019.

Meanwhile, Uniform asset growth has been fairly consistent, positive in thirteen of the past sixteen years, while ranging from -4% to 30%, excluding outlier 28% Uniform asset shrinkage in 2017.

Performance Drivers – Sales, Margins, and Turns

Trends in Uniform ROA have been driven by trends in both Uniform earnings margin and Uniform asset turns.

After expanding from 11%-12% in 2004-2005 to 15%-16% levels in 2012-2015, Uniform margins faded to current 14% levels in 2019.

Meanwhile, Uniform turns sustained 2.3x-2.4x levels from 2004-2006, before expanding to a peak of 2.9x in 2007.

Thereafter, Uniform turns declined to just 1.5x in 2016, before jumping to 2.5x in 2017, and receding to 2.1x in 2019.

At current valuations, markets are pricing in expectations for further declines in both Uniform margins and turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q2 2020 earnings call highlights that management is confident that online usage continued to grow with 3.3 billion Wiley platform sessions in the last 12 months and that they are rapidly shifting the focus of their business to respond to industry challenges.

However, management may lack confidence in their ability to sustain revenue growth and improve their EBITDA margin. Moreover, they may be concerned about their Education Services revenue mix, the sustainability of new society partnerships, and potential headwinds from FX rates.

Finally, they may be exaggerating the strength of their customer and partner network and the consistency of client feedback.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for JW.A than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate JW.A’s profitability.

For example, as-reported ROA for JW.A was 5% in 2019, materially lower than the Uniform ROA of 29%, making JW.A appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2016, as-reported ROA has remained stable at 5%-6% levels, while Uniform ROA has expanded from 21% to 29% over the same timeframe, directionally distorting the market’s perception of the firm’s recent profitability trends.

SUMMARY and John Wiley & Sons, Inc. Tearsheet

As the Uniform Accounting tearsheet for John Wiley & Sons, Inc. (JW.A) highlights, Uniform P/E trades at 16.1x, which is below corporate average valuations but around historical average valuations for the company.

Moderate P/Es require moderate EPS growth to sustain them. In the case of John Wiley & Sons, the company has recently shown a 13% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, John Wiley & Sons’ Wall Street analyst-driven forecast is Uniform EPS shrinkage of 23% in 2020, and a 4% growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $36 per share. These are often referred to as market embedded expectations.

In order to meet current market valuation levels, John Wiley & Sons would have to have Uniform earnings to shrink by 11% each year over the next three years.

What Wall Street analysts expect for John Wiley & Sons’ earnings growth two years out is above what the current stock market valuation requires.

Meanwhile, the company’s earnings power is 5x corporate averages. However, with cash flows and cash on hand dipping below total obligations, this signals that there is a high risk to the company’s operations and credit profile.

To conclude, John Wiley & Sons’ Uniform earnings growth is above peer averages, while the company’s price to earnings is below peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research