This snack giant is eating up the competition during the At-Home Revolution thanks to its irresistible brand portfolio

Breakfast has long been considered the most important meal of the day by dieticians. As the pandemic has forced people to stay at home, people now have more time to consume a full breakfast in the morning. Today’s firm is one of the pillars of the cereal and snack industry.

Looking at as-reported numbers, it appears today’s firm generates declining and below cost-of-capital returns. Digging deeper into the numbers, we can see the firm has stronger profitability than the market thinks.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

I am a big believer of intermittent fasting (“IF”). There’s a large body of research showing it helps with bolstering testosterone, recovering from exercise, and losing weight.

Different from most other diets, IF focuses more on the timing of meals rather than the content or the quantity. Essentially, you complete a number of mini-fasts throughout the week. I found out 12-18 hour fasts daily give me the benefits I need. I fit all of my eating into the remaining six or so hours and fast the rest of the day. During that feeding window, I typically have one very large meal.

On the opposite end of the spectrum, it wasn’t too long ago when dieticians were pushing the idea of grazing. Grazing involves snacking throughout the day and spreading out meals. Instead of eating three moderate meals, someone might eat seven or eight smaller meals throughout the day.

It’s possible that grazing could help some people with weight loss, but it’s easy to see why many fail. It’s harder to limit yourself to 200 calories 10 times a day than it is to limit yourself to 2,000 calories in one meal. Despite the challenge, many people took to the grazing diet and may still be practicing today.

One of the beneficiaries of the grazing trend is Kellogg Company (K). Kellogg is a multinational food company best known for its cereal brands. The firm also owns Pringles, Eggo waffles, Cheez-Its, and other famous brands. The push to regular snacking instead of big meals meant a boon for snacks.

Additionally, the pandemic and subsequent lockdowns sent sales higher as people stocked up on non-perishable goods. Consumers are also spending more time at home due to restrictions on office work. Meals have become more flexible than ever, and your pantry is virtually always available. As a result, many folks have naturally trended towards a grazing pattern.

In addition, Kellogg has exposure to emerging food industries with high growth. The firm owns Morningstar Farms, which is a plant-based version of traditional meat products. Competitor Beyond Meat (BYND) has seen its stock skyrocket as people increase their consumption of alternative meat products.

One might expect a well-diversified and market leading food producer to generate above-average returns. Consumers have developed an affinity for these products and make recurring purchases every time they go to the grocery store.

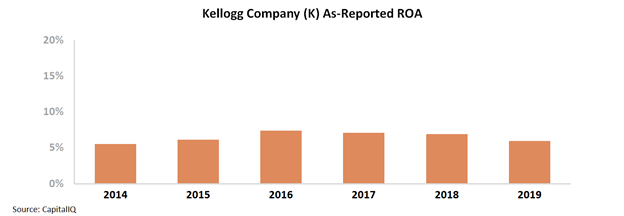

However, looking at as-reported return on assets (ROA), the firm barely looks to meet its cost of capital. Since 2014, its ROA has remained at 6%-7% levels.

Despite Kellogg’s market-leading position and potential tailwinds, it appears the company is unable to capitalize on the strength of its brands, generating below-average returns. At these levels, it looks like Kellogg needs consumers to buy more snacks just to cover its overhead.

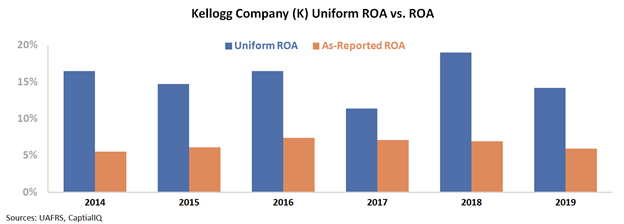

However, this picture of Kellogg’s performance is not accurate. This is due to distortions in as-reported accounting, including the treatment of interest expense and goodwill, among other distortions. Wall Street has missed Kellogg’s profitability.

In reality, Kellogg is a consistently strong business. Its Uniform ROA has ranged between 11% and 19% since 2014, averaging roughly 15%.

Kellogg’s diverse slate of market-leading brands has helped it maintain solid profitability over the last six years, almost the exact opposite story that as-reported metrics imply.

Without Uniform Accounting, investors would miss the strong returns of this snack company. They might see Kellogg as a firm with below average and declining returns instead of robust profitability.

Ultimately, since 2014, Kellogg has maintained its dominance and has continued to acquire firms to add to its brand. Additionally, as people spend more time at home, Kellogg will likely benefit as consumers snack more and continue to increase their at-home breakfast consumption.

SUMMARY and Kellogg Company Tearsheet

As the Uniform Accounting tearsheet for Kellogg Company (K:USA) highlights, the Uniform P/E trades at 23.6x, which is around the global corporate average valuation levels and its historical average valuations.

Average P/Es require average EPS growth to sustain them. In the case of Kellogg, the company has recently shown a 29% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Kellogg’s Wall Street analyst-driven forecast is an EPS growth of 8% and 12% in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Kellogg’s $63 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company would need to have Uniform earnings grow 6% per year over the next three years. What Wall Street analysts expect for Kellogg’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 2x the long-run corporate averages. However, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends, with intrinsic credit risk also being 70bps above the risk free rate. Altogether, these signals a high credit and dividend risk.

To conclude, Kellogg’s Uniform earnings growth is well above peer averages, and the company is trading in line with peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research