Rating agencies are missing the risk of this tottering strip-mall operator, leaving bond investors in the cold

Retail is usually one of the hardest hit sectors during a recession. People have less money to spend on discretionary items, negatively impacting retail store sales.

Today’s company is home to some of the biggest retail stores in the U.S. This firm is a mall real estate investment trust (REIT), with locations across the country and a wide variety of clients.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Looking back at the Great Recession, the retail industry was hit hard. Demand fell precipitously as the economy took its worst hit in nearly a century. Worse yet, when the economy finally returned to normal, retailers were forced to contend with Amazon’s emergence.

Among the hardest hit retail locations were strip malls. These malls struggled to find anchor tenants to keep them alive.

The way strip malls structure their stores is around what are called anchor tenants, which are big-name businesses with high, stable demand that draw people to a mall. While at the mall, customers end up shopping at neighboring stores, helping keep the whole system afloat. Malls with strong anchor tenants are generally more popular.

While many malls have suffered, one of the most resilient has been Kimco Realty Corporation (KIM), one of the largest mall REITs in the country.

Kimco is a REIT with over 400 shopping centers in the U.S. and over 70 million square feet of leasable space. Kimco properties are generally located near large cities, with 85% of revenue coming from its top 20 core markets.

Moody’s & other rating agencies have given the company the benefit of the doubt as a sustainable REIT due to its prior resiliency. The firm is rated a Baa1 investment grade credit by Moody’s.

This implies less than a 2% risk of default over the next 5 years.

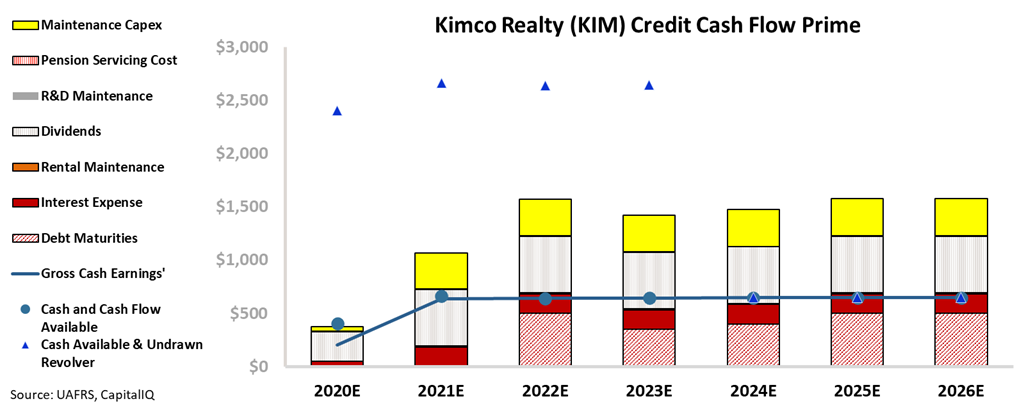

However, looking at the firm’s credit cash flow prime (CCFP), we can see the rating agencies are understating Kimco’s credit risk.

As the CCFP below shows, Kimco is a much weaker credit than rating agencies are assuming.

Kimco’s cash flows and cash on hand fall short of obligations every year going forward. Additionally, cash is below dividend obligations even if Kimco is able to refinance all of its debt maturities.

This means the company is going to have to make some tough decisions going forward about cutting capex spend or dividend obligations.

Additionally, malls have seen a significant drop in demand due to the pandemic. People are increasingly choosing digital outlets to make purchases, potentially hurting the firm’s cash flows if businesses do not resign their leases.

Because of these weak cash flows and minimal cash balance, we rate Kimco a HY2 (B2) credit. This high-yield rating estimates a nearly 25% risk of default, far higher than the 2% implied by Moody’s.

Ultimately, Kimco is a much riskier credit than rating agencies give it credit for.

The firm has weak cash flows and cash balances, which will likely fall below dividend obligations going forward. Furthermore, Kimco may face headwinds in the wake of the pandemic due to the acceleration of e-commerce trends.

Kimco’s true credit risk only becomes obvious when using Uniform Accounting. As-reported metrics can be misleading for understanding both credit and equity signals.

KIM’s Credit Risk is Understated Considering Material Debt Headwalls

Credit markets are understating KIM’s credit risk with a YTW of 1.149% and a CDS of 109bps relative to an Intrinsic YTW of 2.269% and an intrinsic CDS of 186bps. Meanwhile, Moody’s is materially understating KIM’s fundamental credit risk, with its investment grade Baa1 credit rating seven notches higher than Valens’ HY2 (B2) credit rating.

Fundamental analysis highlights that KIM’s cash flows are likely to consistently fall below operating obligations in each year going forward. Moreover, its combined cash flows and expected cash build are expected to fall short of all obligations including debt maturities starting next year, the last year before a series of consistent debt maturity headwalls.

However, the firm has capex flexibility to cover potential cash shortfalls in the near-term. Additionally, the firm’s robust 140% recovery rate on unsecured debt and moderate market capitalization should give it access to the credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for creditors. KIM’s compensation framework should incentivize management to focus on all three value drivers: top-line growth, margin expansion, and asset efficiency, which should lead to Uniform ROA expansion and increased cash flows available for servicing debt obligations.

Additionally, most management members hold significant KIM equity relative to their annual compensation, likely aligning them with shareholders for long-term value creation. That said, a majority of the management team has high change-in-control compensation, indicating they may be incentivized to seek a sale of the company or accept a buyout, increasing event risk.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (8/7) highlights management is confident essential retailers are looking to expand and that they can work with retailers to ensure they make payments on a suitable schedule.

However, management is also confident there are few potential deals on the market and that it is difficult to predict the occupancy rate in 2021. Moreover, they are confident some of their retailers are declaring bankruptcy and that it is difficult to predict spreads.

Moreover, they may be concerned about the potential of new Urban Outfitters and Anthropologie stores and their ability to increase FFO per diluted share. Furthermore, they may be exaggerating how helpful curbside pickup has been for their customers.

Finally, they may lack confidence in their ability to expand to more locations.

KIM’s material debt headwalls indicate that credit markets and Moody’s are understating the firm’s credit risk. As such, both a widening of credit spreads and a ratings downgrade are likely going forward.

SUMMARY and Kimco Realty Corporation Tearsheet

As the Uniform Accounting tearsheet for Kimco Realty Corporation (KIM:USA) highlights, the company trades at a 13.3x Uniform P/E, which is below global corporate average valuation levels and its own historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Kimco, the company has recently shown an 8% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Kimco’s Wall Street analyst-driven forecast projects a 256% EPS growth in 2020 followed by an 85% EPS decline in 2021.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Kimco’s $15.61 stock price. These are often referred to as market embedded expectations.

The company needs to grow its Uniform earnings by 1% each year over the next three years to justify current prices. What Wall Street analysts expect for Kimco’s earnings growth is well above what the current stock market valuation requires in 2020, but well below that requirement in 2021.

Furthermore, the company’s earning power is below the long-run corporate average. Also, cash flows and cash on hand are below total obligations—including debt maturities, capex maintenance, and dividend. Together, this signals high credit and dividend risk.

To conclude, Kimco Realty’s Uniform earnings growth is well above its peer averages, but the company is trading well below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research