Investors can’t tell if this used car Goliath still has room to run, or is already overpriced

Of the industries surging during the pandemic, few have seen acceleration like the used car market. The “At-Home Revolution” has created a new class of car owners.

Using GAAP valuations, today’s firm seems like an interesting investment to take advantage of these trends. However, real valuations are not telling the same story.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

One consequence of the pandemic forcing social distancing is increased spending outside of cities. Consumers are moving out of urban areas to trade the defunct benefits of city living for more home space.

With this lifestyle shift comes a change in transportation. In cities, it’s easy to rely on public transportation. Now, new suburban and rural homeowners need a car to get around. Additionally, even current city dwellers are investing into cars to avoid taking public transportation and risk exposure to the virus.

This has driven a huge spike in demand for used vehicles. Newer buyers tend to be more price sensitive and are looking for the better deal. This has led to a huge acceleration in the entire market.

According to the Manheim Used Vehicle Value Index, the median price of used vehicles jumped in price by 17% during 2020.

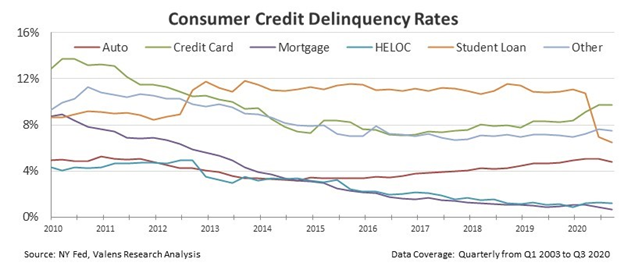

In a normal recession, consumer loan defaults tend to spike in areas like car loans, and customers are forced to make tough choices. In 2020, auto loan default rates actually fell slightly thanks to this strong market.

With prices at all-time highs and huge shortages in the used car market, car sellers and suppliers are set up to win.

This is why the market has been betting on CarMax (KMX).

CarMax is the largest used car retailer in the United States, with over seven hundred thousand cars sold in 2019. Now, investors are betting on CarMax taking advantage of the record demand to grow that number tremendously.

Over the past year, the stock has more than doubled from pandemic lows. The name is trading at around $120, near all time highs.

After such an impressive stock run, investors today are bound to wonder if upside can continue, or the stock is overbought.

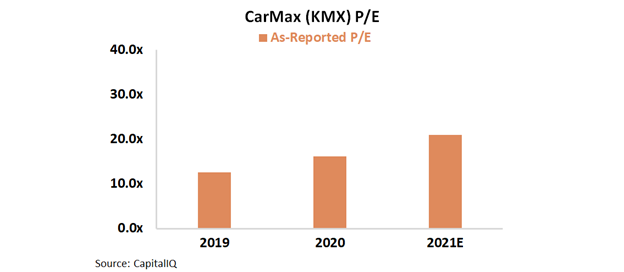

Looking just at as-reported metrics, investors would be inclined to believe this run could continue. The as-reported P/E ratio for CarMax is only 21x, slightly above the corporate average.

A company positioned for growth in such a hot industry should see a P/E multiple well above averages, as investors price in this market upside.

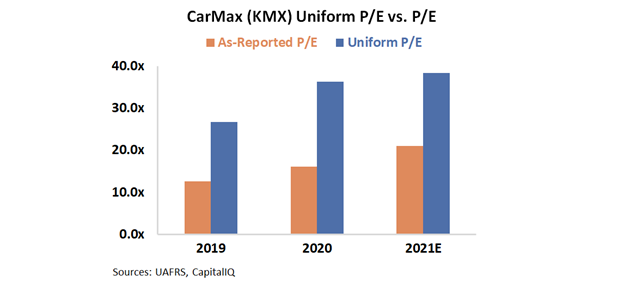

However, most investors’ interpretations of P/E are being distorted by as-reported accounting practices.

Thanks to GAAP treatment of financial subsidiaries, operating leases, and other line items, the earnings power of CarMax is being misstated.

Rather than a P/E in line with averages of 20x, the real Uniform P/E of the company is 38x, almost double.

Using Uniform Accounting, it becomes clear the market has already priced in the tailwinds of the used car market into CarMax’s stock price.

Investors stuck with faulty data may assume there is further upside for CarMax, and buy into stock after its run. Investors stuck using faulty data will always be investing behind the curve.

SUMMARY and Carmax, Inc. Tearsheet

As the Uniform Accounting tearsheet for CarMax, Inc. (KMX:USA) highlights, the Uniform P/E trades at 37.6x, which is above the global corporate average of 25.2x and its own historical average of 32.3x.

High P/Es require high EPS growth to sustain them. In the case of CarMax, the company has recently shown a 15% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, CarMax’s Wall Street analyst-driven forecast is a 12% EPS decline in 2021 and an 18% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify CarMax’s $121 stock price. These are often referred to as market embedded expectations.

In order to justify current market expectations, the company would need to have Uniform earnings grow by 14% each year over the next three years. What Wall Street analysts expect for CarMax’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Also, cash flows and cash on hand are at 260% its total obligations—including debt maturities and capex maintenance. Together, this signals an average credit risk.

To conclude, CarMax’s Uniform earnings growth is below its peer averages while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research