This traditionally poor performing industry may be riding the At-Home Revolution’s tailwinds

With stiff competition entering the space over the years, this grocery company has faced significant headwinds and declining returns.

The At-Home Revolution has reinvigorated consumers’ desire to make their own food, and this company may be poised for a turnaround.

Today we highlight if this potential turnaround is an investable opportunity.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Smart restaurants have shifted their business models from dine-in to takeout over the last year. While takeout has certainly been on the rise, there has also been a surge in aspiring home cooks.

People with extra time on their hands have tried their hands at everything from fresh pasta to sourdough bread, and some have shifted their habits to include more home-cooked meals throughout the week.

Companies like Blue Apron (APRN) have benefited because they provide fast and easy ways for novice cooks to make their own food.

While demand for dine-in has started recovering, there’s a new demographic of home cooks who, due to cost, convenience, or a new hobby, aren’t planning on going back to restaurants any time soon.

As people are making more meals at home, not only cooking kit companies like Blue Apron win. Key players in the food supply chain win as well.

Another great example are grocery stores like Kroger (KR).

Traditionally, grocery stores have been unexciting businesses to be in. With large square footage required, slim margins, and little differentiation, grocery chains have needed to focus on efficiency to survive.

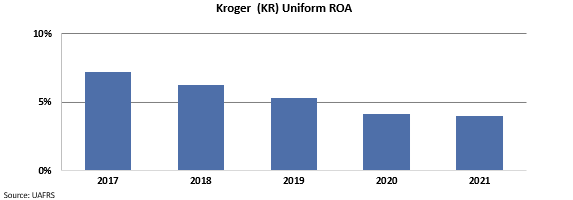

Furthermore, over the last few years, stores like Kroger have begun to face stiff competition from firms like Walmart (WMT). As competition has placed higher pressures on the firm, Kroger has seen their returns fade.

Specifically, return on asset (ROA) levels have faded from 6% in 2017 to 4% in 2021.

As discussed above, the At-Home Revolution has started to improve the grocery business.

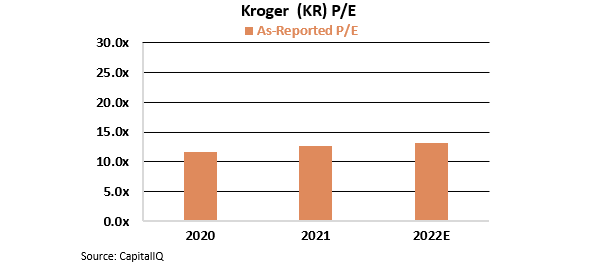

When looking at the company’s valuations, it looks like the market is ignoring Kroger’s potential in this new environment.

Specifically, by looking at the company’s as-reported P/E ratio, investors can conclude Kroger is trading at a relatively inexpensive 13x P/E compared to the corporate average of about 25x.

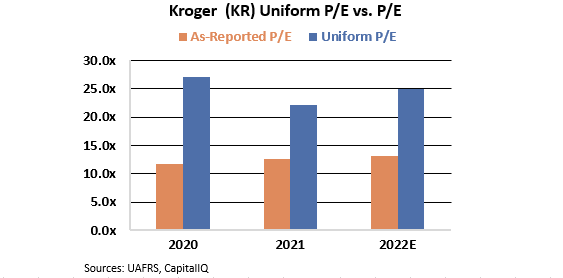

In reality, once Uniform Accounting adjustments are made, the company’s valuations tell a different story than the as-reported basis.

Kroger’s Uniform P/E is currently 26x, which is actually around market averages, showing the firm to be trading at a slight premium rather than a discount.

As highlighted, Kroger’s valuations are trading on par with the corporate average, which doesn’t make it an attractive stock to ride these tailwinds.

By looking at the Uniform Accounting metrics, we can easily pick out the difference between what could be an improving company and a rising stock. While Kroger the business may see improvement over the next few months, any upside for the stock may already be priced in.

SUMMARY and The Kroger Co. Tearsheet

As the Uniform Accounting tearsheet for The Kroger Co. (KR:USA) highlights, the Uniform P/E trades at 25.6x, which is around the global corporate average of 25.2x, and its own historical average of 26.2x.

Moderate P/Es require moderate EPS growth to sustain them. That said, in the case of Kroger, the company has recently shown an 18% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Kroger’s Wall Street analyst-driven forecast is a 31% EPS growth in 2021 and 1% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Kroger’s $37 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 8% per year over the next three years in order to justify current stock prices. What Wall Street analysts expect for Kroger’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Also, intrinsic credit risk is 70bps above the risk-free rate and cash flows and cash on hand are falling below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a high dividend risk and low credit risk.

To conclude, Kroger’s Uniform earnings growth is above its peer averages and the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research