This billboard company is priced like it’s going out of style, Uniform Accounting shows why those expectations are wrong

This advertising company is able to use older technology to succeed.

As-reported metrics would have you believe this company’s strategy has left it with returns only slightly above cost-of-capital levels, but true UAFRS (Uniform) based analysis shows the firm’s real profitability.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Over the past one hundred years, the world of marketing and advertising has changed drastically. As consumers have shifted where they spend time and get information, advertisers have changed with them.

Newspapers, radio, and television advertisements used to be the most popular marketing mediums. Now, more and more advertising spend is allocated to online mediums.

Google (GOOGL) and Facebook (FB) dominate the online and digital marketing world. Estimates put their combined market share at over 50% of all online advertising revenues. With the Google-Facebook duopoly taking in so much advertising and marketing spend, investors wonder if any other advertising method is worth investing in.

Many people see physical advertisements as a loser in the changing advertising market. One firm in particular that looks like it is struggling is Lamar Advertising (LAMR). Lamar is a real estate investment trust (REIT) that owns and operates over 300,000 billboards all over the United States and Canada.

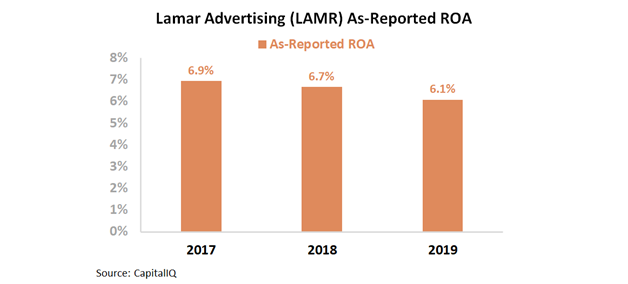

Investors see the company as having outdated and dying technology. As such, it is no surprise to these investors for the firm to realize declining profitability levels. As-reported return on assets (ROA) has fallen each of the past three years. Last year it was only at 6%, in line with corporate averages.

However, this is not an accurate depiction of the firm. Mistreatment of interest expenses and amortization, among other distortions, are severely decreasing the firm’s earnings.

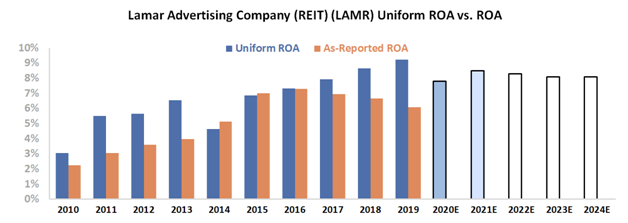

Uniform ROA for Lamar was actually 9% in 2019, and more importantly, Uniform ROA has risen every year since 2014.

Investors and the market appear to be overly pessimistic about the firm and its strategies. It is undeniable that online advertising has grown considerably over the past few years. However, physical advertising still has its place. For example, the average American spends nearly seven hours a week in the car, and while doing so passes dozens of billboards.

Also, Lamar understands it needs to adapt. As such, the firm has invested in technology like its Network Operating Center. This center allows Lamar to alter its digital billboards so advertisements can change based on the time of day. It also allows the firm who is using the billboard to showcase live scores, trending items, or any other user generated content to drive “eyeballs.”

With all of the improvements and growth Lamar has seen in recent years, it is surprising to see the market believes the growth trend will now end. In order to see specifically what the market is expecting the firm to do, we can use the Embedded Expectations Framework.

The chart below explains the company’s historical corporate performance levels, in terms of ROA (dark blue bars) versus what sell-side analysts think the company is going to do in the next two years (light blue bars) and what the market is pricing in at current valuations (white bars).

Sell-side analysts believe Uniform ROA will fall this year as advertising spend has dropped due to coronavirus. However, analysts also think Uniform ROA will continue to rise again in 2021. After that, the market is pricing in Uniform ROA to plateau.

However, companies will most likely begin to invest more in advertising once the country begins to fully open up. When that happens, Lamar very well may see its profitability continue its upward trend.

Investors are writing off Lamar because of its low as-reported ROA and old advertising model. However, those items are not telling the whole story.

Lamar has invested in newer technology in recent years and because of that, it has seen its as-reported ROA rise for years. With expectations of stagnant ROA being priced in, this may be a company investors want to keep an eye on.

Lamar Advertising Company (REIT) Embedded Expectations Analysis – Market expectations are for Uniform ROA to remain stable, but management may be concerned about AFFO, expenses, and debt issuances

LAMR currently trades near recent averages relative to Uniform earnings, with a 23.8x Uniform P/E (Fwd V/E’). At these levels, the market is pricing in expectations for Uniform ROA to maintain 8%-9% levels from 2019 through 2024, accompanied by 6% Uniform asset growth.

Meanwhile, analysts have similar expectations, projecting Uniform ROA to sustain 9% levels through 2021, accompanied by 10% Uniform asset shrinkage.

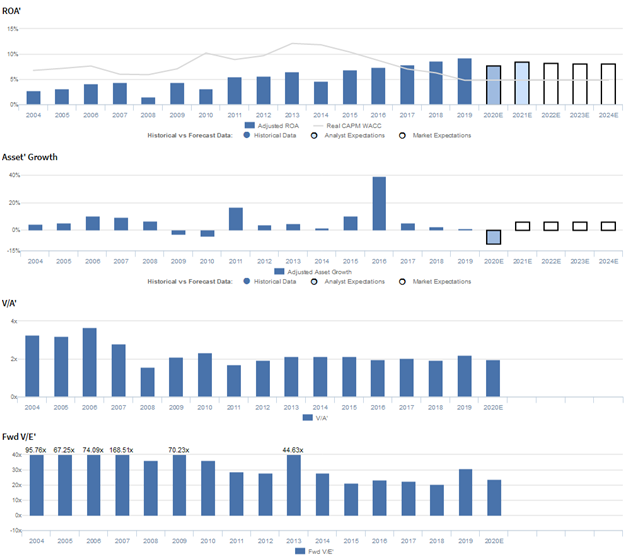

As a REIT specializing in the highly competitive outdoor advertising space, LAMR has historically seen weak, but generally improving profitability. After expanding from 3% in 2004 to 4% in 2007, Uniform ROA collapsed to 2% in 2008, amidst recessionary pressures. However, since then, Uniform ROA has rebounded to a peak of 9% in 2018-2019.

Meanwhile, Uniform asset growth has been somewhat volatile, positive in fourteen of the past sixteen years, while ranging from -5% to 39%.

Performance Drivers – Sales, Margins, and Turns

Improvements in Uniform ROA have been driven primarily by Uniform earnings margins expansion, slightly offset by declining Uniform asset turns.

Uniform margins expanded from 7% in 2004 to 11% in 2007, before collapsing to 4% in 2008 and recovering to 21% in 2013. Then, after declining to 15% in 2014, Uniform margins rebounded to 38% peak levels in 2018-2019.

Meanwhile, after improving from 0.4x in 2004 to 0.5x in 2005, Uniform turns have gradually compressed to 0.2x levels in 2017-2019.

At current valuations, markets are pricing in expectations for Uniform margins and Uniform turns to stabilize near current levels.

Earnings Call Forensics

Valens’ quantitative analysis of the firm’s Q4 2019 earnings call highlights that management may lack confidence in their ability to sustain adjusted funds from operations (AFFO) per share performance and reduce capex and other full-year expense growth. Moreover, they may be concerned about their recent $600mn bond issuance and the impact of recent changes to their reported guidance.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for LAMR than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics overstate LAMR’s margins, a key driver of profitability. For example, as-reported EBITDA margin for LAMR was 43% in 2019, higher than Uniform earnings margin of 38%, making LAMR appear to be a stronger business than real economic metrics highlight.

Moreover, since 2008, Uniform margins have expanded from 4% to 38%, while as-reported EBITDA margin has remained at 43% levels over the same timeframe, directionally distorting the market’s perception of the firm’s historical profitability trends.

SUMMARY and Lamar Advertising Company (REIT) Tearsheet

As the Uniform Accounting tearsheet for Lamar Advertising Company (REIT) (LAMR:USA) highlights, the Uniform P/E trades at 23.8x, which is around corporate average valuation levels and its own history.

Average P/Es require average EPS growth to sustain them. In the case of Lamar Advertising, the company has recently shown a 7% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lamar Advertising’s Wall Street analyst-driven forecast is a 30% shrinkage in 2020, before a 20% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lamar Advertising’s $66 stock price. These are often referred to as market embedded expectations.

The company needs Uniform earnings to grow by 1% each year over the next three years to justify current prices. What Wall Street analysts expect for Lamar Advertising’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 2x above the corporate average. However, cash flows are below their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals high dividend and credit risk.

To conclude, Lamar Advertising’s Uniform earnings growth is below its peer averages. Also, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research