Leidos may have figured out the secret to winning profitable government contracts

Few people picture government contractors as the sort of companies to mint cash.

With the competitive bidding processes and increased oversight that come along with a check from Uncle Sam, on the surface, the industry appears only a marginally profitable one at best.

Yet, for one provider of solutions in the defense and national security space, Uniform Accounting presents a fundamentally different story.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Government contracts have always been very competitive. State, local and federal contractors all bid their lowest possible price for these jobs as to guarantee tax payers get the best deal possible.

Taxpayers expect to get both quality and price for their contributions to the government, and elected officials can be held responsible or booted out of office if they don’t deliver.

That’s why government contracts operate differently than those from the private sector. The deals also almost always include specific rules in case the contractors go over budget, requiring them to be on the hook for any overage.

They also typically require certain reviews and regulations in areas such as sourcing, ostensibly to make sure no one is making too much money from the government’s checkbook.

With this sort of imposed oversight and regulation, one would intuitively expect most government contractors to see their profitability trend towards cost-of-capital levels, which are currently around 6%.

This should be even more pronounced for firms who simply outsource labor instead of providing customized goods, research, or development.

Applying this logic, one might assume a company like Leidos Holdings (LDOS), the majority of whose business is focused on government contracting in areas such as intelligence analysis, cybersecurity, and operational support, would have minimal or no economic returns.

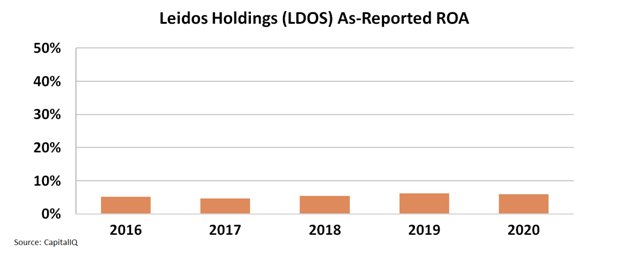

As a matter of fact, a glance at as-reported financial metrics would seem to confirm the thesis that the government doesn’t allow its contractors to reap massive profits from tax-funded programs.

Over the past five years, Leidos has seen a meager as-reported return on assets (“ROA”) of 5%-6%, right around cost of capital levels, leading one to assume the government is managing their contracts with exactly this philosophy in mind.

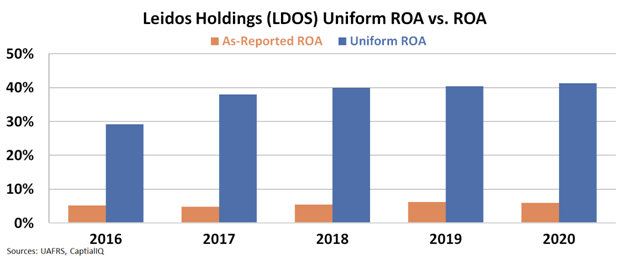

However, none of the government officials making these deals understand how GAAP metrics fail to display economic reality, something they could stand to learn.

That’s because the reality is, while the government may think Leidos is generating cost-of-capital returns through its contracting business, the company is actually producing Uniform ROA over 40%, highlighting how profitable the business of providing services to the government can be.

Thanks to Uniform Accounting, we can see that specialized service solutions in areas like defense and intelligence lead not only to big government contracts, but profitable ones as well.

Military spending, especially in specialized fields such as cybersecurity, is set to only increase in the future. This means certain defense contractors, whose profitability remains obscured by as-reported financial data, are set to benefit tremendously.

While some government officials may not recognize what is really going on, the reality doesn’t change, and we here at Valens will continue to sift through the noise.

SUMMARY and Leidos Holdings, Inc Tearsheet

As the Uniform Accounting tearsheet for Leidos Holdings, Inc (LDOS:USA) highlights, the Uniform P/E trades at 15.6x, which is around the global corporate average of 21.9x and its historical P/E of 15.7x.

Low P/Es require low EPS growth to sustain them. That said, in the case of Leidos, the company has recently shown a 21% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Leidos’ Wall Street analyst-driven forecast is an 8% and 9% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Leidos’ $92 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 2% annually over the next three years. What Wall Street analysts expect for Leidos’ earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power in 2020 is 7x the long-run corporate average. Moreover, cash flows and cash on hand are nearly 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, Leidos’ Uniform earnings growth is below its peer averages, while the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research