Let’s check up on this green energy ETF that crashed back down to earth

This ETF was the darling of green energy investors last year, but it has seen a large pullback in recent months.

Amidst more extreme weather events and startling new reports on climate change, let’s check up on iShares Global Clean Energy ETF (ICLN) to best understand if the carbon neutral future is an investable theme, or still a bit overambitious to invest in today.

In addition to examining the portfolio, we’re including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Earlier this month, the Intergovernmental Panel on Climate Change (IPCC), a United Nations committee tasked with converting the latest scientific climate research into actionable policy suggestions, released a new report.

Unsurprisingly, the scientific consensus has not shifted its pessimistic tone on the issue. To the contrary, this report goes further than ever before to link human activity to not just the general warming of the climate, but also to specific weather calamities.

It also projects that even if all emissions stopped today, the existing greenhouse gasses already floating around in our atmosphere will warm the earth by an additional 1.5 degrees Celsius by 2040.

Much of this has already been known within various corners of the scientific world, but the news is garnering extra attention as it landed amidst a wave of increasingly extreme weather.

Record heat waves in the normally mild Pacific Northwest are causing uncontrollable wildfires to burn patches of land larger than the state of Rhode Island. Flooding in Germany, China, and India in areas not accustomed to massive storm surges and torrential rain is causing billions in damages. Battling climate change has become top-of-mind around the globe.

In the United States however, many people and politicians have yet to be convinced. The difference of opinion on climate change issues has become politicized, and with the “my way or the highway” nature of lawmaking, little progress is being made.

The reality isn’t quite so bleak. For example, five U.S. states have joined Canada and most of western Europe in agreeing to ban the sale of internal combustion engines by 2035 or earlier in favor of far more efficient electric vehicles.

California has mandated that all new houses be built with rooftop solar panels, with other states looking to do the same.

Although the United States has been jumping in and out of the Paris Agreement, which is the most multilateral push yet to address climate change, 63 Fortune 500 companies have independently committed to keep up with the Paris guidelines.

It cannot be denied, however, that even despite the waves made by clean energy monolith Tesla Motors (TSLA), the biggest and most impactful companies laying the groundwork for a carbon-neutral future are not American.

The primary reason for this is that climate change legislation has smoother paths in other countries.

Clean energy tech requires masses of R&D funding. On its own, it would never be economically feasible because oil & gas are leagues cheaper in the short run. It is not only cheaper now—It will continue to be cheaper so long as battery technology lags behind our collective energy storage needs.

However, once battery technology makes the necessary breakthroughs, everything will change. Wind and solar will overtake fossil fuels as the cheapest source of energy. Combined with their obvious benefits in emissions and worker safety, there won’t be a compelling reason to go back.

Despite this, on its own, the investment thesis is hazy. Nobody knows when these breakthroughs will happen, and in the interim, investors’ funds could work harder for them in other sectors. This is where government funding becomes so crucial.

Governments, which aim to serve not as investors but as agents for public good, can lighten the load for early investors. Hence, clean energy investment has centered around the countries where the government is most willing to help.

The United States, as it stands, is not one of those countries.

Investors confined to the American exchanges would not have access to green energy center-of-mass companies like the Denmark-based Orsted A/S (CPSE:ORSTED) and Vestas Wind Systems A/S (CPSE:VWS), or Spanish firm Iberdrola SA (BME:IBE).

But they do have access to the iShares Global Clean Energy ETF, trading as ICLN.

ICLN garnered a lot of attention last year as it bucked the trend of years-long flatness and soared from pre-pandemic highs of around $14 to over $33 in January 2021.

The run was fueled by some of the general lockdown-driven confidence and fund inflows to the equity markets, as well as the presidential election. Biden, who at the time was significantly ahead in polling, promised to usher in a wave of new funding for renewables and green technology. Anticipation grew further once he became President-Elect.

But in a classic case of “buy the hype, sell the news,” ICLN snapped its win streak immediately following the release of Biden’s energy plan. Since hitting its January highs, the ETF has backtracked about half of last-year’s gains.

Green energy investors may now be wondering what to expect moving forward. Let’s use Uniform Accounting to conduct a portfolio audit of ICLN’s largest holdings.

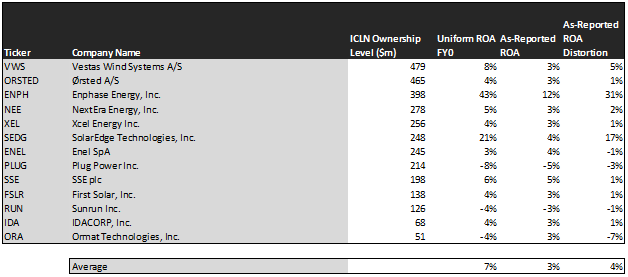

Although the business picture for green energy continues to improve, this table demonstrates the difficulty in maintaining an investment thesis for renewables without government support.

However, the market is seeing things to be worse than they truly are. Among these 13 names, the average as-reported return on assets (ROA) is only 3%, far below the cost of capital.

This is due to numerous distortions inherent to not only the American-used Generally Accepted Accounting Principles (GAAP), but also the International Financial Reporting Standards (IFRS). These rulebooks for financial reporting are startlingly inept at accurately representing the true profitability of companies.

After adjusting the financial statements, we can see that the average Uniform ROA is actually right around the cost of capital, sitting at 7%. This is an important barrier to cross because it shows businesses aren’t losing money compared to other investments.

It also shows these companies are more profitable than the oil and gas industry, which in recent years has consistently generated returns below the cost of capital.

One standout name among these holdings is Enphase Energy (ENPH). The California-based company supports the rooftop solar panel industry by selling inverters, batteries, and control software.

Enphase reports ROA of 12%, which is in-line with the U.S. corporate average. In reality, the company boasts a robust 43% ROA, and is growing fast. Over the past two years, Enphase’s revenue has nearly doubled and its margins have expanded significantly.

SolarEdge Technologies (SEDG), which sells a similar product to Enphase but to larger utilities installations, reports a lackluster 4% ROA. In reality, the company currently has a 21% Uniform ROA and has been robustly profitable for the past several years.

However, If SolarEdge and Enphase were to be removed from the analysis, average Uniform ROA for the remaining 11 names would only be 2%. This is reflective of the fact that green power generation is still in its infancy.

Without affordable industrial-scale energy storage solutions, renewable energy companies can only sell energy when there is sun or wind, limiting the utilization of their assets. Government funding might be able to bridge the gap to the advent of badly needed battery technologies, but the funds are not enough to turn most of the raw power generation companies profitable.

The companies poised to post strong profitability in the shorter term are those that sell needed clean energy components, software, services, and use-cases. ICLN, however, doesn’t seek these firms out specifically. Its purpose is to aggregate the entire clean energy market, not pick winners and losers.

For investors to really generate alpha, understanding profitability is only one part of the story. They also need to know what stocks are under-appreciated by the market, and which have lofty priced-in expectations.

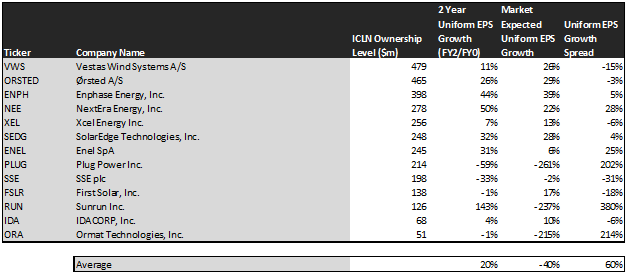

For this, we can use our Embedded Expectations Analysis. Take a look below:

This chart shows three interesting data points:

– The first datapoint is what Uniform earnings growth is forecast to be over the next two years, when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework. This represents the Uniform earnings growth the company is likely to have, the next two years.

– The second datapoint is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we are showing how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily and our reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for Uniform earnings growth.

– The final datapoint is the spread between how much the company’s Uniform earnings could grow if the Uniform Accounting adjusted earnings estimates are right, and what the market expects Uniform earnings growth to be.

For many hopeful green energy investors, these insights may bear some bad news. Given the current valuations of these companies, the market is expecting earnings to shrink by 40% over the next two years.

Analysts, who work every day to understand sales and industry trends, have more bullish expectations. They expect earnings to grow by 20%.

To investors, this means these companies need to beat analyst expectations to just meet their current valuation, let alone experience significant upside.

For example, take a look at ICLN’s largest holding, Denmark-listed Vestas Wind Systems (CPSE:VWS). While analysts expect 11% earnings growth, the market has priced in 26% growth.

Similarly, Xcel Energy (NasdaqGS:XEL), which is a pure-play renewable electricity generation company, has 13% earnings growth priced into its current valuation, whereas analysts expect a more muted 7% growth.

The key takeaway for investors is that as a whole, the green energy market is priced for success despite the gaps in technical capability. Although it has walked back much of last year’s gains, ICLN is still far from a value play. There may still be significant upside over the long-term, but investors may need to ask themselves what else their money can do in the meanwhile.

Although the industry is still young, it is far from a given that every green energy company will be able to rest on market trends alone to deliver value to shareholders. Given the low general profitability levels and high reliance on public funding, some of the ICLN names may not make it.

This is why we have built tools that allow you to see the same information as the largest hedge funds and financial institutions, to better help you pick out the winners from the losers yourself. Click here to learn how to get access to the Valens research company analysis tool.

Read on to see a detailed tearsheet of ICLN’s largest holding, Vestas Wind Systems.

SUMMARY and Vestas Wind Systems Tearsheet

As one of iShares Global Clean Energy ETF’s largest individual stock holdings, we’re highlighting Vestas Wind Systems’ tearsheet today.

As our Uniform Accounting tearsheet for Vestas Wind Systems (VWS:DNK) highlights, its Uniform P/E trades at 72.9x, which is above the global corporate average of 21.9x and its own historical average of 61.5x.

High P/Es require high EPS growth to sustain them. In the case of Vestas Wind Systems, the company has recently shown a 32% Uniform EPS shrinkage.

While Wall Street stock recommendations and valuations poorly track reality, Wall Street analysts have a strong grasp on near-term financial forecasts like revenue and earnings.

As such, we use Wall Street GAAP earnings estimates as a starting point for our Uniform earnings forecasts. When we do this, Vestas Wind Systems’ Wall Street analyst-driven forecast is a 33% EPS decline in 2021, followed by a 86% EPS growth in 2022.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify Vestas Wind Systems’ Kr. 241 stock price. These are often referred to as market embedded expectations.

What Wall Street analysts expect for Vestas Wind Systems’ earnings growth is below what the current stock market valuation requires in 2021 and above in 2022.

The company’s earnings power is 1x corporate averages. Additionally, cash flows are above their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit risk.

To conclude, Vestas Wind Systems’ Uniform earnings growth is well below peer averages, and the company is trading well below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research