Leveraging what we teach in the classroom in the investing world

Every year, we teach a course on how to look at the best companies in the world, and we teach another on how to value stocks from the perspective of the best investors.

Learning about the investing greats shows us what makes a good business, a good investment, and how those two might not be the same.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Last Sunday, we wrapped up the first of two executive MBA courses we teach every year at Hult International Business School.

Last week’s class was called Return Driven Strategy (RDS), which is the framework I created alongside Dr. Mark Frigo more than 15 years ago.

The framework distills what makes great companies successful. It is a straightforward framework that builds up from companies having genuine assets as its bedrock.

It then peaks with the idea that the only way companies can actually maximize wealth sustainably, like the companies that we study in Return Driven Strategy, is by doing so ethically.

Otherwise, managers will eventually run their businesses into the ground.

A great company that we have taught about in the class for as long as we have been teaching it is Danaher Corporation (DHR).

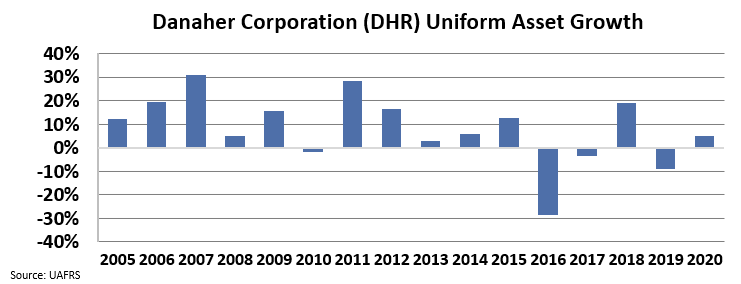

As Uniform Accounting metrics highlight, the company has only seen its return on asset (ROA) levels dip below 20% one time in the past 15 years.

See for yourself below.

Additionally, it has regularly been able to achieve double-digit asset growth. It has been able to do this from both acquisitive and organic growth thanks to its genuine asset, the Danaher Business System.

This genuine asset is the company’s process for integrating acquisitions and streamlining its purchases, along with constant optimization of its business processes.

That said, while Danaher is a great Return Driven Strategy company, it is not a company we will be teaching in the next part of the class.

The class that begins tomorrow is called Global Strategic Valuation (GSV). This is the class where we teach how to pick great stocks.

Danaher, for as great of a company as it is, isn’t a great stock. The market already knows just how dominant the Danaher Business System is, meaning investors are pricing in the company’s genuine assets.

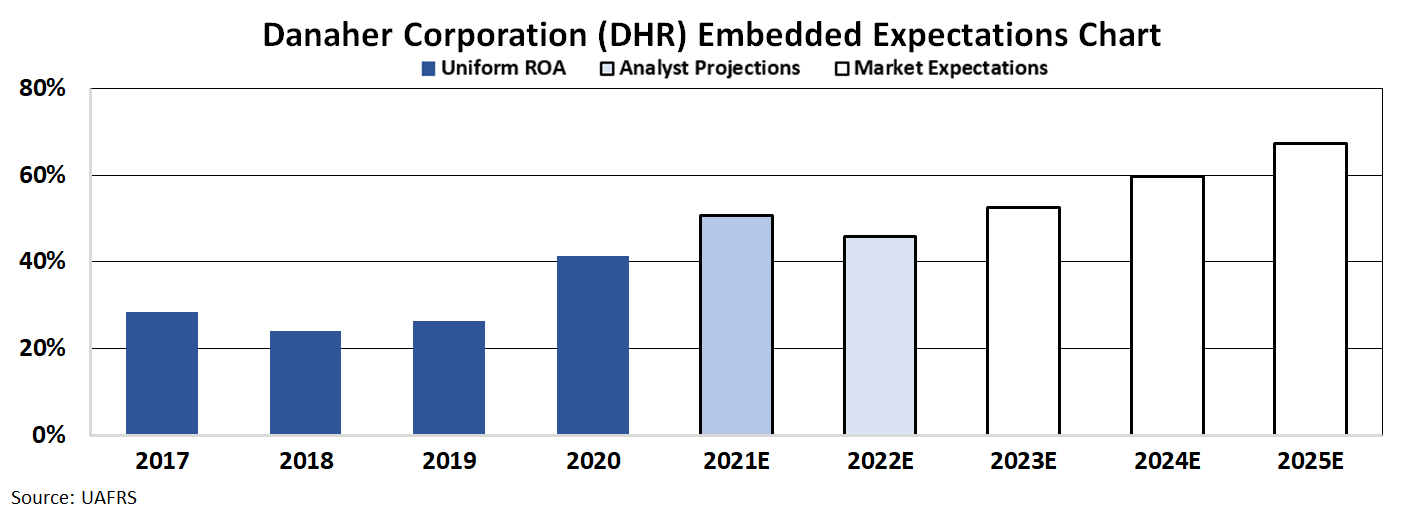

To gain a greater understanding about what the market is pricing in, we can use our Embedded Expectations Framework.

Most investors determine stock valuations using a discounted cash flow (DCF) model, which takes assumptions about the future and produces the “intrinsic value” of the stock.

However, here at Valens, we know models with garbage-in assumptions only come out as garbage. Therefore, we’ve turned the DCF model on its head with our Embedded Expectations Framework. Here, we use the current stock price to determine what returns the market expects.

In the chart below, the dark blue bars represent Danaher’s historical corporate performance levels in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how the company’s ROA will shift in the next five years.

Wall Street analysts are expecting Danaher’s Uniform ROA to improve to 46% levels by 2022.

Well above this forecasted growth, the market is pricing in Uniform ROA to expand to 67% by 2025.

Our embedded expectations model shows the market is pricing the company’s ROA to rise to record high levels by 2025.

This is why studying both business strategy, like we do in RDS, and valuation like we do in GSV, is so important.

To understand if a company could be a great stock, investors first have to study its business strategy. However, not all great companies are great stocks to own.

SUMMARY and Danaher Corporation Tearsheet

As the Uniform Accounting tearsheet for Danaher Corporation (DHR:USA) highlights, the Uniform P/E trades at 28.8x, which is above the global corporate average of 23.7x and its own historical average of 26.4x.

High P/Es require high EPS growth to sustain them. That said, in the case of Danaher, the company has recently shown a 60% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Danaher’s Wall Street analyst-driven forecast is a 39% EPS growth in 2021 and immaterial EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Danaher’s $253 stock price. These are often referred to as market embedded expectations.

Danaher is currently being valued as if Uniform earnings were to grow 12% annually over the next three years. What Wall Street analysts expect for Danaher’s earnings growth is above what the current stock market valuation requires in 2021 but below that requirement in 2022.

Furthermore, the company’s earning power is 7x the long-run corporate average. Also, cash flows and cash on hand are 4x above its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, Danaher’s Uniform earnings growth is above its peer averages and the company is also trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research