If you’ve ever worn sweatpants to a Zoom meeting, you understand something the rating agencies don’t

If you used to go to work wearing a suit, chances are that you don’t anymore. Today’s company stands to benefit enormously from this post-pandemic casualization trend.

But the credit rating agencies still see it as a risk to its bondholders. Let’s dive in with Uniform Accounting to put the company’s cash flows up against its obligations and see how the rating agencies have missed the story.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The last year and a half has seen many people bask in the joy of one simple pleasure: being able to work in sweatpants.

For a long time, the idea of casual workplaces was seen as a big perk. Employees at tech companies loved that they could come to work wearing jeans, versus slacks, skirts, and suits.

Once the work environment got pushed to whatever can be seen through a webcam, many people went all the way to sweatpants. Now anybody could live the tech company dress code dream and more!

While work environments were slowly moving in this direction already as part of a broad, multi-decade casualization trend, the several months during the pandemic marked a sudden step-change for every industry. That change was more significant than the prior twenty years worth of casualization. Even Goldman Sachs completely eliminated their dress code.

Now that employees are returning to physical work, companies are realizing they can’t just ignore the past two years with their dress code.

Even the companies that are fully in-person with little to no remote option realize they are competing with firms that do allow remote work, and the casual dress that comes with it. Hence, in-person work everywhere has casualized significantly in the wake of the pandemic.

When the 170 year old originator of jean culture, Levi Strauss (LEVI), went public in 2019, this was not the future it and investors expected.

In the company’s most recent earnings call, CEO Charles Victor Bergh spoke about a new denim cycle. It’s not only being driven by rapid post-Covid casualization, but customers who delayed their new jeans purchases during the pandemic all buying at once, causing a rush of sales.

Bergh explained that the denim category over the past 9 months has hit $11.2 billion, higher than the $10.6 billion compared to the same period in 2019, and far higher than the $8.5 billion during the pandemic.

These incremental sales are bolstering the company’s cash flows and building its cash position, which it can use to reinvest into new products or capacity, return capital to shareholders, or repay its debt.

But with the major credit rating agencies still rating Levi as a high yield name with a BB+ rating, they imply it has a 10% risk of going bankrupt in the next 5 years. Amid tailwinds marking the beginning of a strong cycle and foundational changes in demand extending past any cycle, our team thought to investigate.

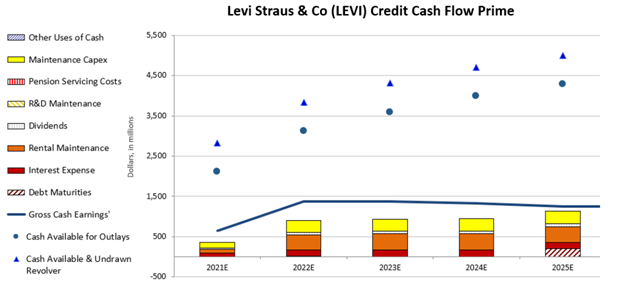

A closer look at the company’s Credit Cash Flow Prime (“CCFP”) shows no real risk of default. Levi has lots of cash, and no debt maturities for several years, and cash flows that well exceed obligations.

In the chart below, the stacked bars represent the firm’s obligations each year for the next seven years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand available at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

Even with earnings coming back down in later years as the denim cycle wanes, this CCFP shows that the company poses no significant risk to its creditors. Levi is an investment grade IG4+ name.

Dislocations in credit ratings are often followed by dislocations in credit yields. We are always looking for bonds with attractive risk-reward payoffs.

The Valens Conviction Credit List offers deep credit security analysis that identifies the best bonds in the corporate credit universe. Investors looking for a safe place to store their money for the next five or fewer years should look no further than the Conviction Credit List. Learn about how to get access here.

SUMMARY and Levi Strauss & Co. Tearsheet

As the Uniform Accounting tearsheet for Levi Strauss & Co. (LEVI:USA) highlights, the Uniform P/E trades at 18.1x, which is below the corporate average of 24.3x, but around its historical P/E of 18.2x.

Low P/Es require low EPS growth to sustain them. In the case of Levi, the company has recently shown a 60% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Levi’s Wall Street analyst-driven forecast is for 238% and 11% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Levi’s $27 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 15% over the next three years. What Wall Street analysts expect for Levi’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, the company’s earning power in 2020 is near the long-run corporate average. Moreover, cash flows and cash on hand are more than 2x its total obligations—including debt maturities, capex maintenance, and dividends. Additionally, intrinsic credit risk is 60bps above the risk-free rate. All in all, this signals a low dividend and credit risk.

Lastly, Levi’s Uniform earnings growth is above peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research