The small electrical component manufacturer Littelfuse is poised to supply the next investment wave

Here at Valens, we often talk about the upcoming capex supercycle in the United States, such as with Cleveland-Cliffs back in November.

This supercycle promises a huge wave of growth in the U.S. and an expansion of corporate earnings to new highs. For investors to be best exposed to this theme, they should be looking at all of the suppliers to the smart infrastructure revolution.

Today, we’ll use Uniform Accounting to understand the true profitability of Littelfuse and decide whether Wall Street has gotten it wrong yet again.

Also below, a detailed Uniform Accounting tearsheet of the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

In late 2021, we regularly highlighted a huge trend we see that will begin playing out over the next few years.

For the past 20 years, the assets across corporate America’s balance sheets, along with the nation’s infrastructure, have grown significantly older. Partly thanks to once-in-a-generation black swan events like the Great Recession and the coronavirus pandemic pushing off investment, the U.S. is ready for big spending on infrastructure once again.

A big part of this re-investment will come in shoring up aging supply chains that are buckling under the post-pandemic load. Other parts will be in bringing in new fiber cabling across the U.S. to allow the world to be more interconnected than ever before.

This is why a large piece of this reinvestment is going to be in smart investment. Smart investment isn’t in the sense of how intelligently it will be allocated, even though today’s engineering tools make it easier than ever. Instead, smart means connecting things to the internet that have never been online before.

With the birth of the internet of things, or moving physical objects onto the internet, the big winners of this capex supercycle won’t just be the traditional construction supplies like Caterpillar (CAT) and Danaher (DHR). It will also be the suppliers of all of the electrical equipment investors aren’t paying attention to yet.

One example of these electrical part suppliers is Littelfuse (LFUS), which makes fuses, dischargers, sensor products, diodes, and transistors. These are all the exact kinds of small pieces that are going to be needed to power the next wave of smart investment.

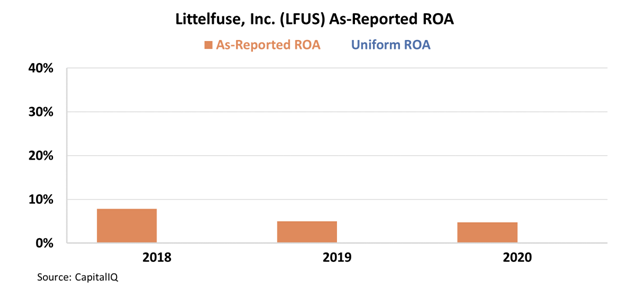

However, looking at the as-reported metrics, it would appear that an investment in Littelfuse would be throwing good money at bad anyway. Over the past three years, returns have slid from below average 8% levels to just 5%, around the cost of capital for the business.

However, a closer look at the business’s real performance tells a much different story. Using Uniform Accounting, which adjusts for distortions such as goodwill and excess cash, which are artificially inflating the assets on the balance sheet.

After resolving these discrepancies, we can see that in reality returns have been not only above the cost of capital but above average returns as well. While returns did fall during the pandemic as companies put off investment, returns were as high as 31% in 2018.

As spending promises to pick up again in earnest going into 2022 and beyond, names like Littelfuse promise to boom. However, this isn’t the only name that is going to see a huge benefit from the surge in capex spending.

In our Conviction Long List, we highlight a plethora of names that are poised to benefit from this macroeconomic trend that the wider investment community hasn’t yet caught onto. If you are interested in reading more, you can click here to subscribe.

SUMMARY and Littelfuse, Inc. Tearsheet

As the Uniform Accounting tearsheet for Littelfuse, Inc. (LFUS:USA) highlights, the Uniform P/E trades at 19.4x, which is below the global corporate average of 24.0x, but around its historical P/E of 19.7x.

Low P/Es require low EPS growth to sustain them. In the case of Littelfuse, the company has recently shown a 12% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Littelfuse’s Wall Street analyst-driven forecast is a 73% and 2% growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Littelfuse’s $297 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 8% annually over the next three years. What Wall Street analysts expect for Littelfuse’s earnings growth is above what the current stock market valuation requires in 2021 but below that requirement in 2022.

Furthermore, the company’s earning power is 3x above the long-run corporate average. Moreover, cash flows and cash on hand are 4x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

Lastly, Littelfuse’s Uniform earnings growth is above peer averages but the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research