This utility-like industry isn’t regulated like one, and Uniform Accounting shows that has led to massive returns the market isn’t recognizing

Due to their steady volume demand and lack of switching alternatives for customers, utilities are heavily regulated by governments to avoid price gouging, thus limiting their profitability.

Meanwhile, this industry has similar dynamics to utilities, with steady demand and few alternatives, yet lacks the same government scrutiny. As a result, one would expect firms in this industry to be massively profitable, but as-reported metrics inaccurately portray that this is not the case.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Gas. Water. Electricity. These bills have been something most homeowners or renters have become accustomed to, often prioritizing these payments over most other obligations.

The need for these utilities in everyday life gives the utility companies that provide them steady volume demand. People need to use them consistently, leading to decreased volatility and resistance to economic swings.

Utility businesses are often natural monopolies. The infrastructure required to produce and deliver their services are often extremely expensive to build and maintain. New power plants don’t pop up every day and going off-grid with generators and wells isn’t feasible for most.

The combination of a steady volume of demand and the lack of alternatives or competitors to give consumers switching options is why utilities themselves are heavily regulated. This regulation helps prevent utilities from price gouging, while allowing them to remain profitable.

Another industry that has consistent demand from those who need it, regardless of economic downturns, has come to the forefront in the midst of the pandemic—lab testing.

This industry is essential for the medical field, helping patients and doctors conduct a variety of important tests from routine blood screens to complex gene-based testing to coronavirus testing, most recently.

Outside of those internal to medical facilities, this industry is dominated in the United States by two major players, Quest Diagnostics (DGX) and Laboratory Corporation of America (LH), or LabCorp for short.

However, these companies are not regulated nearly as much as utilities, even though they are just as necessary to many people’s lives and given that there are few alternatives.

Considering the prices they charge aren’t regulated like an electric or water company’s, one would expect them to generate sky high returns. For the most part, demand is steady regardless of price.

However, as-reported metrics show that they haven’t been as profitable as one would expect.

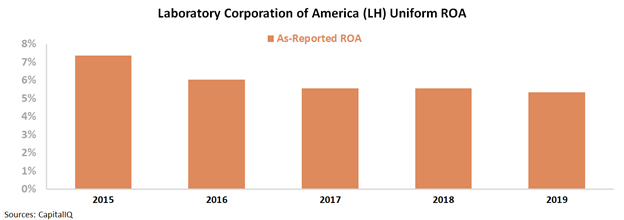

In fact, over the past five years, as-reported ROA for LabCorp has declined from 7% in 2015 to 5% in 2019, barely eclipsing cost-of-capital levels. The company’s profitability is not even at corporate average levels.

This finding is baffling. Perhaps these firms are staying controlled in their pricing to avoid the additional scrutiny and regulation they may risk by overcharging? Perhaps they understand their importance to society and want to remain as accessible as possible?

Although optimistic thoughts, in reality, the as-reported metrics are just wrong. LabCorp and Quest both do have impressive returns when using Uniform Accounting to cut out misleading accounting distortions.

Historically, LabCorp’s returns have been robust, consistently above 15% each year. That said, this year, they’re forecast to dip dramatically. Even though people are relying on LabCorp for coronavirus testing, the healthcare system’s strong focus on this one area has severely limited demand for their other, potentially higher-margin, services around elective procedures.

Even though the coronavirus appears to be an issue that will be largely transitory, markets are pricing in expectations for returns to remain near historical lows in the long-run, misunderstanding how profitable this company actually is.

Although many people have been able to delay more routine or preventive screenings and many healthcare providers have halted most voluntary procedures, these health services are still necessary and can’t be delayed forever, suggesting that equity upside may be warranted for LabCorp once these services are reinstated.

Laboratory Holdings Embedded Expectations Analysis – Market expectations are for Uniform ROA to decline to record lows, but management is confident about growth, margins, and free cash flow

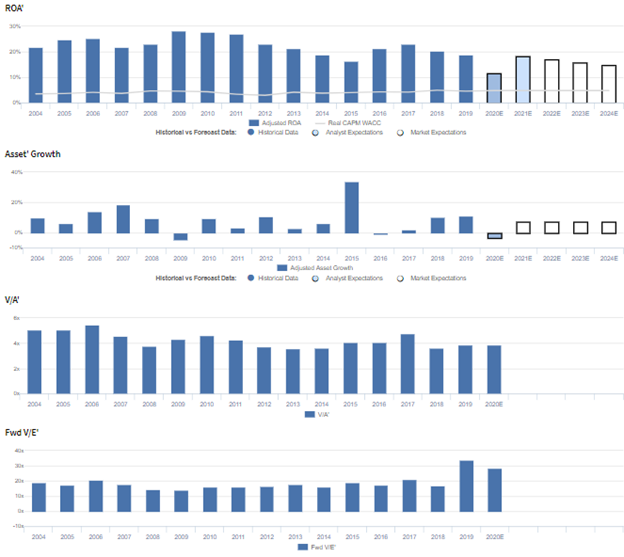

LH currently trades near corporate averages relative to Uniform earnings, with a 28.7x Uniform P/E (Fwd V/E′). At these levels, the market is pricing in expectations for Uniform ROA to fall from 19% in 2019 to 15% in 2024, accompanied by 8% Uniform asset growth going forward.

Meanwhile, analysts have less bearish expectations, projecting Uniform ROA to slightly decline to 18% levels through 2021, accompanied by 3% Uniform asset shrinkage.

Historically, LH has seen robust, but somewhat volatile profitability. Uniform ROA ranged from 22%-25% levels from 2004-2008, before expanding to a peak of 28% in 2009-2010 and fading to 16% in 2015. Subsequently, following the acquisition of Covance, Uniform ROA recovered to 21%-23% levels in 2016-2017, before falling to 19% in 2019.

Meanwhile, Uniform asset growth has historically been somewhat consistent, positive in fourteen of the past sixteen years, while ranging from -5% to 19%, excluding outlier 34% growth in 2015, due to the aforementioned acquisition.

Performance Drivers – Sales, Margins, and Turns

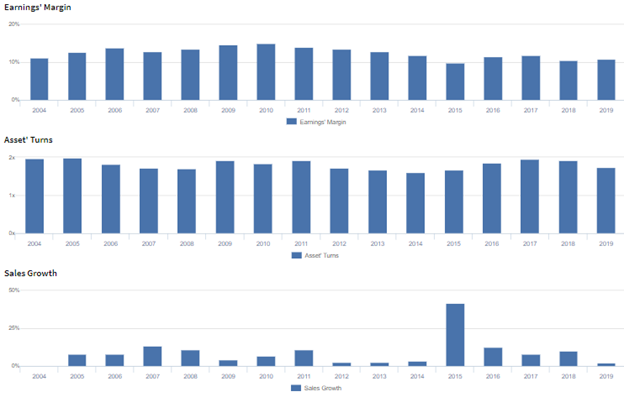

Trends in Uniform ROA have been driven by compounding trends in both Uniform earnings margin and Uniform asset turns.

After improving from 11% in 2004 to a peak of 15% in 2010, Uniform margins have since regressed back to 11%-12% levels in 2016-2019.

Meanwhile, Uniform turns faded from 2.0x in 2004 to 1.7x in 2008, before rebounding to 1.9x in 2011 and compressing to 1.6x in 2014. Then, after recovering to 1.9x in 2016-2018, Uniform turns declined to 1.7x in 2019.

At current valuations, markets are pricing in expectations for continued deterioration in both Uniform margins and Uniform turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q4 2019 earnings call highlights that management is confident they expect a 3% revenue growth rate in 2020 when excluding unusual items, that their free cash flow improved from $926mn in 2018 to $1.04bn, and that they expect margins to improve again.

In addition, they are confident they expect Covance organic revenue growth to range in the mid-to high single-digits both with and without pass-throughs.

However, management may be overstating the potential synergies of their Covance acquisition and the regulatory commercialization support capabilities of their cell and gene therapy development solutions.

Furthermore, they may have concerns about capital allocation and increases in their capital expenditures, and they may lack confidence in their ability to sustain acquisition-related revenue growth.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for LH than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight.

Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate LH’s profitability.

For example, as-reported ROA for LH was near 5% in 2019, materially lower than Uniform ROA of 19%, making LH appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2015, as-reported ROA has declined from 7% to 5%, while Uniform ROA has shown improving fundamentals, rising from 16% to 19% over the same timeframe, directionally distorting the market’s perception of the firm’s recent profitability trends.

SUMMARY and Laboratory Corporation of America Holdings Tearsheet

As the Uniform Accounting tearsheet for Laboratory Corporation of America Holdings (LH) highlights, it trades at a 28.7x Uniform P/E, which is above corporate average valuations and its company’s historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of LabCorp, the company has recently shown a robust Uniform EPS growth of 10%.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, LabCorp’s Wall Street analyst-driven forecast is for Uniform EPS shrinkage of 48% in 2020, followed by 106% growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $170 per share. These are often referred to as market embedded expectations.

In order to meet current market valuation levels, LabCorp would have to have Uniform earnings grow 2% each year over the next three years.

What Wall Street analysts expect for LabCorp’s earnings growth is higher than what the current stock market valuation requires.

Meanwhile, the company’s earnings power is 3x corporate averages, and their robust cash flows and cash on hand signal that there is low risk to the company’s operations and credit profile.

To conclude, LabCorp’s Uniform earnings growth is below peer averages, but the company’s price to earnings is above peer average valuations.

Best regards,

Joel Litman

Chief Investment Strategist

at Valens Research