Losing the “quarantine 15” means turning to diet players like Medifast

With folks returning to the office and re-entering their normal routines, many have been working over the past two years to lose that pandemic weight gain.

This is why returns for companies like Medifast have exploded, as return subscription customers have decided to seek out their services for the first time.

However, as-reported metrics seems to miss the tailwinds Medifast is seeing, and makes it appear the company has low profitability.

That’s why this showed up on our FA Alpha Screen. Its strong profitability, high growth, and attractive valuations make it a compelling company.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

During the pandemic, routines were disrupted, gyms were closed, and it was possible to wear sweatpants to work. All of these factors combined to create a phenomenon known as the “quarantine 15,” an all-too common weight gain trend.

During the last two years, more folks than ever were looking for alternative ways to be healthy and shed any unwanted pounds.

For many, this meant going out and buying exercise bikes like Peleton’s (PTON) offerings. While this can be effective, Peloton stock is now suffering after pulling forward demand and running out of the market.

Meanwhile, the total health and diet players like Medifast (MED) are thriving even as the pandemic has abated. With its plethora of diet products and lifestyle brands, customers to any of Medifast’s offerings are repeat customers to keep up their health, even as the world opens back up.

However, as-reported metrics seem to miss just how much people are willing to pay for this service, and how much returns in 2020 should have improved from this demand.

As-reported metrics make it appear that return on assets (“ROA”) has only been improving slowly over the past three years, with no change from any subscription bump in 2020. This would tell investors they were unable to capitalize on this huge tailwind in the industry.

For a company positioned so well to ride these pandemic tailwinds, investors would hope to see a much stronger picture in 2020.

Meanwhile, Uniform Accounting shows us a different picture than stagnant profitability.

Looking at the right numbers, we can see that Medifast actually saw a massive surge in profitability as demand skyrocketed. Uniform ROA jumped from 83% in 2019 to 139% in 2020.

Furthermore, returns have been suppressed in 2021 only because the business is investing heavily in growth. Medifast grew by almost 150% in 2021 to accommodate the new demand.

As folks looked to become healthier and combat weight gain in 2020 and 2021, it’s clear they turned to Medifast to make that happen.

However, the market seems to be missing these tailwinds, as it’s still pricing Medifast at a bargain 12x Uniform P/E.

But you can only see this impressive performance if you look at the right Uniform Accounting data.

As-reported metrics hide Medifast’s strong ROA in 2020, which combined with its explosive growth in 2021 and low valuations today, makes it a compelling company and an interesting FA Alpha 50 name.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies, but rather looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

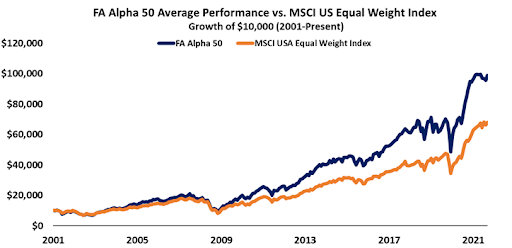

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

If you’re interested in seeing the other 49 names on this month’s FA Alpha, click here to learn more.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research