As-reported metrics make Lululemon look like just an average company rather than a trendsetter

Nowadays, athleisure rules the fashion world. Customers look for trendy outfits that they can wear while going out with friends and hitting the gym. Combining style and functionality, athleisure wear is the rising star of the apparel industry.

Today, we are going to look at Lululemon Athletica Inc (LULU), one of the leading brands in athleisure, through the eyes of Uniform Accounting, to see how it’s performing as more and more people turn to workout clothes.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

A fusion of “athletic” and “leisure”, athleisure wear is among the signature fashion trends of the 21st century.

With the rise of synthetic fibers, health consciousness, and the social media platforms like Instagram, athleisure has become increasingly popular over the years.

And in the last few years, demand for comfortable and stylish clothing has been rising even more when people started to work from home.

Every big name in the sportswear industry has been investing heavily to launch their athleisure lines and one of the early contenders is Lululemon Athletica. It pioneered athleisure wear with the launch of its “Boogie Pants” in 1998 and has remained a leader and trendsetter in the industry since.

Lululemon has been a powerful brand in athleisure wear for so long that it almost feels like it’s faded in the background.

Despite all this, looking at as-reported metrics the company does not look to be leading a fashion trend of the 21st century. Instead, it looks like an average sportswear company.

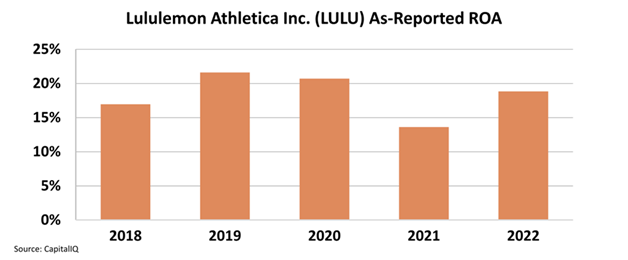

As-reported metrics indicate that Lululemon has consistently been between a 15% and 20% return on asset (“ROA”) business over the past 5 years.

For a company at the front of the athleisure trend, its ROA appears to not be anything extraordinary.

However, as-reported metrics understate the company’s real profitability.

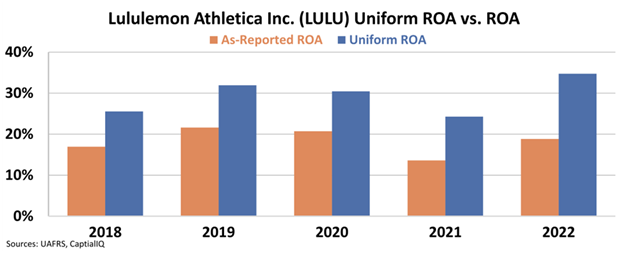

Uniform Accounting provides a totally different perspective for Lululemon and shows the true performance of the company.

As people think about working from home more regularly, or permanently, and being more casual, demand surged for Lululemon’s products and its profitability followed.

As Uniform Accounting shows, ROA has not been stable. It’s actually been improving and rose from 25% levels in 2021 to 35% levels in 2022.

In reality, the strength of Lululemon’s brand remains impressive, and over the past five years, the company’s Uniform ROA has been in the 25% to 35% range, as opposed to the 15% to 20% that as-reported metrics lead us to believe.

In the same time period, Lululemon has been investing in its growth, recently acquiring Mirror to capitalize on at-home workouts and further develop its athletic brand.

The distortions of as-reported metrics have been hiding how Lululemon took advantage of the At-home Revolution and implemented a successful growth strategy to help the firm remain strong, even as life returns to normal post-pandemic.

As clothing remains more casual going forward, Lululemon remains well-positioned to continue to see impressive profitability that the market seems to be missing.

Uniform Accounting provides the right tools for investors to unlock the real value that the company offers. To learn more about how to gain access to the real numbers for almost 25,000 companies around the world, click here to read about our Uniform Accounting database.

SUMMARY and Lululemon Athletica Inc. Tearsheet

As the Uniform Accounting tearsheet for Lululemon Athletica Inc. (LULU:USA) highlights, the Uniform P/E trades at 34.5x, which is above the global corporate average of 24.0x, but below its own historical P/E of 40.1x.

High P/Es require high EPS growth to sustain them. In the case of Lululemon Athletica, the company has recently shown a 71% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Lululemon Athletica’s Wall Street analyst-driven forecast is 15% and 16% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Lululemon Athletica’s $317 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 13% annually over the next three years. What Wall Street analysts expect for Lululemon Athletica’s earnings growth is above what the current stock market valuation requires through 2024.

Furthermore, the company’s earning power in 2022 is 6x the long-run corporate average. Also, cash flows and cash on hand are about 4x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals low credit and dividend risk.

Lastly, Lululemon Athletica’s Uniform earnings growth is below its peer averages, and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research