This company will help the supply-chain supercycle keep the lights on

We anticipate a surge in investment for infrastructure development and supply chain enhancement in the U.S. This surge will lead to the establishment of new manufacturing facilities, warehouses, and distribution centers.

An important player in this landscape is LSI Industries (LYTS), a provider of lighting and display solutions tailored for commercial use.

Notably, LSI has already begun reaping the rewards of increased infrastructure spending and is well-positioned to continue capitalizing on this trend.

However, market sentiment raises doubts about the sustainability of this trend and expectations point to a potential decline in profitability.

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

As we discussed last week, the U.S. is planning significant investments to bolster domestic infrastructure and strengthen supply chain resilience over the coming years.

This initiative is aimed at addressing aging roads, bridges, airports and other public works, as well as incentivizing production and distribution capabilities within the U.S.

The scale of funding earmarked for these purposes is expected to drive substantial construction of new manufacturing plants, warehouses, distribution centers, and other commercial and industrial facilities.

There will be considerable demand for a wide range of materials and equipment needed to outfit the interiors and exteriors of these projects.

One company that is positioned to directly benefit from this spending is LSI Industries (LYTS).

As a leading provider of advanced lighting and graphic display solutions, LSI’s products see widespread use in commercial applications such as retail stores, warehouses, office buildings, airports, and more.

Its lighting fixtures and digital signage are crucial components for new facilities being built across various industries.

Furthermore, LSI has undergone a transformation in recent years under new leadership appointed in 2018. The management team implemented measures to improve operational efficiency and financial flexibility.

Notable actions included paying down debt obligations and divesting non-core business lines. These strategic moves have strengthened LSI’s balance sheet and profitability profile compared to prior years.

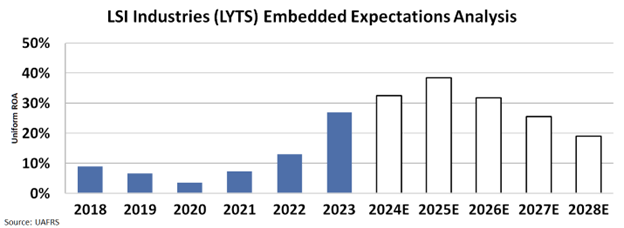

The company’s Uniform return on assets (“ROA”) jumped from 9% in 2018 to 27% in 2023.

Take a look…

LSI has already captured growth opportunities stemming from the initial ramp-up in infrastructure spending over the last fiscal year. Its revenues expanded during this period.

With billions more in allocated public works funding still in the pipeline at the federal level through at least 2026, construction activity can be expected to remain at elevated levels. This is a good signal for the continuation of project awards and orders for LSI’s lighting solutions.

Despite the promising outlook, it appears that the broader market remains skeptical about the sustainability of this growth trajectory.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall to around 19%, a big fall from 27% in 2023.

The market thinks that high growth in profitability isn’t sustainable.

The market outlook likely underappreciates the company’s solid competitive positioning and financial foundation and the long runway of infrastructure projects still in development.

LSI is well equipped through its product range and production capabilities to capitalize on rising demand from these incentives.

Further gains in market share and margins appear attainable.

SUMMARY and LSI Industries Tearsheet

As the Uniform Accounting tearsheet for LSI Industries (LYTS:USA) highlights, the Uniform P/E trades at 12.9x, which is below its global corporate average of 18.4x, but above its historical P/E of 3.8x.

Low P/Es require low EPS growth to sustain them. In the case of LSI Industries, the company has recently shown an 8% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, LSI Industries’ Wall Street analyst-driven forecast is a 21% and 16% EPS growth for 2024 and 2025, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify LSI Industries’ $15.07 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 13% annually over the next three years. What Wall Street analysts expect for LSI Industries’ earnings growth is above what the current stock market valuation requires through 2025.

Furthermore, the company’s earning power is 4x its long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends.

All in all, this signals low dividend risk.

Lastly, LSI Industries’ Uniform earnings growth is above its peer averages and in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research