Manufacturing is coming back to U.S. shores, benefitting names like Oshkosh

For customers to see prices come back to earth, it seems that some amount of reshoring is necessary, reversing the globalization trends of the past twenty years. The U.S. government is investing into domestic manufacturing to help repair malfunctioning supply chains.

This is going to be a huge win for domestic manufacturers, and especially equipment providers for building. Oshkosh Corporation (OSK) is one example of a company who will directly benefit from this spending wave.

As-reported metrics make it seem like Oshkosh has an unprofitable business that is slowly dying. However, Uniform Accounting proves that the company is already profitable and ready to take a piece of the spending coming.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The U.S. has learned its lesson from the pandemic and supply chain crisis.

In the last two years, consumers witnessed extended lead times, increased unavailability of products, and a higher number of canceled orders.

The government is aware of the problem, and now they are trying to fix it. The CHIPS and Science Act President Biden signed is a first step to addressing these issues through onshoring.

This is the time for production to come home. As a recent Bloomberg article made the case, the aftermath for the pandemic is the best time to shorten supply chains and bring mission-critical manufacturing back to the U.S.

This will be a huge advantage for domestic manufacturing companies. And one of the biggest winners is going to be companies who make the tools needed to build new factories and industrial parks on domestic soil.

One big potential beneficiary in that space is Oshkosh Corporation (OSK).

The company manufactures and markets access equipment, specialty vehicles, and truck bodies for various markets.

Through its biggest segment of access equipment, it provides a wide range of products such as work platforms and telehandlers.

The company is highly exposed to construction, industrial, institutional, and general maintenance applications. This makes the company well-positioned to benefit from the domestic Supply Chain Supercycle

Reshoring would mean an increased number of operations and customers. However, investors need to be sure of the company’s ability to boost profitability before making a decision.

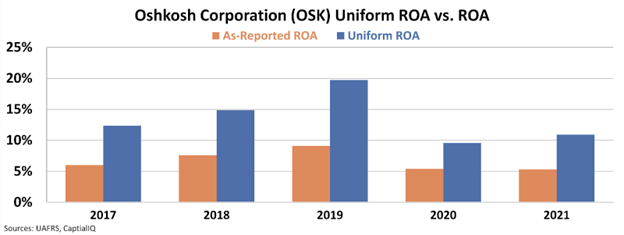

Looking at the as-reported metrics, Oshkosh seems like it is generating returns just above the cost of capital. This is not a good sign for investors.

The as-reported return on assets (“ROA”) of the company went down from 6% in 2017 to 5% in 2021.

Even though the company may benefit from reshoring, it seems to have difficulties with its profitability, making investors concerned.

However, this picture of the company’s profitability is inaccurate. This is because of the distortions in as-reported accounting, and they can be fixed by making the over 130 adjustments needed under Uniform Accounting standards.

In reality, the profitability of the company is twice the as-reported numbers.

Uniform ROA was 12% in 2017 and stabilized at 11% in 2021.

The company is already above average in profitability, and it will see benefits from the reshoring trend in the U.S.

Investors using as-reported metrics would think that the company doesn’t have a good business, and the spending coming to them would not help it that much.

Uniform Accounting proves otherwise and allows investors to see the reality.

SUMMARY and Oshkosh Corporation Tearsheet

As the Uniform Accounting tearsheet for Oshkosh Corporation (OSK:USA) highlights, the Uniform P/E trades at 17.6x, which is around the global corporate average of 19.3x and its own historical P/E of 16.3x.

Low P/Es require low EPS growth to sustain them. In the case of Oshkosh Corporation, the company has recently shown a 22% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Oshkosh Corporation’s Wall Street analyst-driven forecast is a 39% EPS shrinkage and 80% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Oshkosh Corporation’s $81 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 8% annually over the next three years. What Wall Street analysts expect for Oshkosh Corporation’s earnings growth is below what the current stock market valuation requires in 2022, but above the requirement in 2023.

Furthermore, the company’s earning power in 2021 is 2x the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 80bps above the risk-free rate.

All in all, this signals low credit risk.

Lastly, Oshkosh Corporation’s Uniform earnings growth is below its peer averages, but the company is trading near its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research