The market is ignoring the growing debt crisis while valuing this company

Buy Now, Pay Later (BNPL) services like Affirm (AFRM) and Klarna have surged in popularity, but rising credit losses and risky borrower profiles are raising red flags.

Nearly two-thirds of BNPL users have subprime credit, and many hold multiple simultaneous loans, indicating growing financial strain.

Despite this, companies like Affirm are projecting significant profit improvements, with the market pricing in a strong turnaround.

However, these optimistic expectations may overlook the mounting defaults, loosened regulatory oversight, and the risk of broader fallout.

The BNPL model, once seen as a flexible solution, could usher in the next major consumer credit crisis.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

Americans are using “Buy Now, Pay Later” (“BNPL”) for everything from laptops to lunch.

Affirm Holdings (AFRM), Klarna, and others have pitched it as a zero-interest solution for consumer flexibility.

At first, this innovative solution promoted spending, but the cracks are forming.

Klarna, one of the biggest BNPL providers, reported a 17% year-over-year rise in credit losses.

Moreover, the Consumer Financial Protection Bureau (“CFPB”) found that nearly two-thirds of BNPL users have risky credit profiles.

As households fall under financial pressure, this could be the start of a credit domino effect.

BNPL defaults are quietly surging, even as major players downplay the threat. Klarna claims defaults are a “tiny share” of total loans, while Affirm insists there are “no signs of stress” among its borrowers.

The reality is very different. BNPL use in 2023 topped $75 billion in the U.S., often by borrowers already in debt.

These loans may be interest-free but they’re not risk-free. The CFPB’s latest data shows nearly two-thirds of BNPL borrowers have subprime or deep subprime credit and BNPL lenders granted approval for 78% of loan applications from this group.

Julie Margetta Morgan, now leading the Century Foundation, suggested that many Americans were turning to buy now, pay later services as a temporary fix layered on top of existing credit card debt.

Numbers from the CFPB back this claim. 63% of BNPL borrowers had at least two simultaneous loans during the year, while 33% had BNPL loans from multiple providers.

With rising delinquencies and a rollback in regulatory oversight under the Trump administration, BNPL players are flying into a storm without radar.

Klarna’s rising credit losses and Affirm’s expanding loan book, up 36% year-over-year, are warning signs.

However, the market has high confidence in BNPL players despite concerning industry data.

Affirm is the only major public BNPL lender, making it a key name to watch. Yet it hasn’t generated even one year of positive operating income since going public in 2021. Still, investors seem convinced the company will soon turn things around.

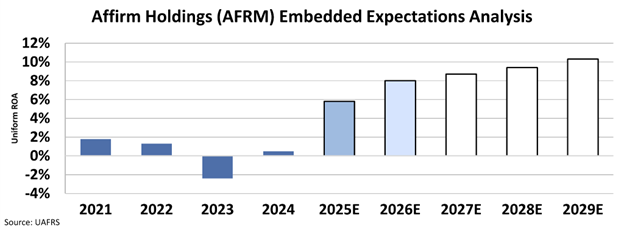

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Affirm’s Uniform return on assets (“ROA”) has been far below the cost of capital since 2021, ranging from (2%) to 2%.

Analysts expect Uniform ROA to improve significantly over the next two years reaching 8% by 2026.

And the market thinks Uniform ROA will sustainably expand even beyond that level to 10% by 2029.

Take a look…

That tells us the market expects Affirm to go from losing money to making solid profits by 2025 and keep improving from there, an optimistic view that overlooks rising credit problems.

BNPL lenders are lending to people already stretched thin, and Affirm’s current valuation doesn’t reflect that danger.

As more people miss payments and regulations loosen, the fallout could be severe.

The CFPB’s weakened oversight creates the perfect environment for unchecked risk.

Without formal protections, BNPL lenders can continue offering loans to people already struggling with debt.

If late payments keep rising, it won’t just be Affirm investors who suffer. Stores, credit card issuers, and the broader economy could all feel the effects.

What started as a feel-good way to split up purchases could end up as the next big consumer credit mess.

Investors should be skeptical of companies that rely on fragile borrowers to keep growing.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research