The market punishes this pharmaceutical company unfairly along with the rest of the sector

Pharmaceuticals has always been a complex sector to understand. One usually needs to understand the science behind the products to be sure of an investment.

However, there are incredibly profitable and resilient parts of this sector, such as orphan drugs with extended licenses.

Harmony Biosciences (HRMY) falls into this category with its unique drug for daytime sleepiness and licenses.

The market treats the company as a regular uncertain pharmaceutical name, which leads to undervaluation.

That’s why it showed up on our FA Alpha Screen. The market’s lack of understanding of the sustainability of its high returns, the company’s high growth, and low valuations make it an interesting name.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

Investors are usually very cautious when it comes to pharmaceutical investments.

They have a good reason for that. These businesses are tough to understand for people who do not know the science behind them.

Whether a company can get approval for the drug (they developed or not) affects the valuations a lot, as research and development (“R&D”) is a big part of the business.

Even so, there are companies that have proven they have a working business model out there, and they are more resilient than most people think.

One of these areas is orphan drugs. Once the R&D process is done and the drug is approved, companies see high profitability that is sustainable in the long term.

This is because they get extended licenses and continue to benefit from them for years.

A company we are following right now is Harmony Biosciences (HRMY). It develops and commercializes therapies for patients with rare neurological disorders in the U.S.

The company falls into the exact category we have been describing, as it has a license for a unique drug for daytime sleepiness.

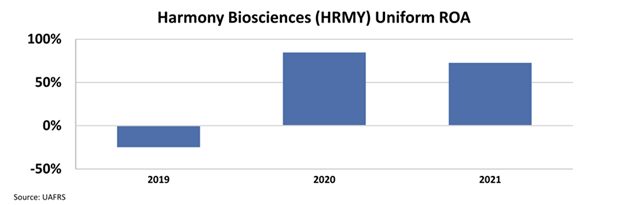

This license unlocked very high profitability for it. The Uniform return on assets (“ROA”) jumped from -25% in 2019 to 85% in 2020, just in a year. It sustained high profitability last year with an ROA of 73%.

Harmony Biosciences continues to invest in its core business, which is why they had incredible growth as well.

Of course, this incredible story does not mean investors should necessarily be investing in the stock. Recent growth in profitability and assets is not enough to consider this name as a potential investment.

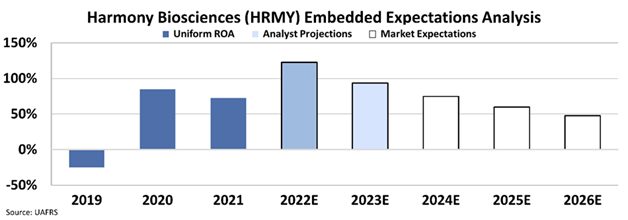

It is important to understand what the market thinks. If the consensus is that Harmony will be much more profitable each year going forward, this may cause overvaluations.

By utilizing our Embedded Expectations Analysis (“EEA”) framework, we can see what investors expect these companies to do at the current stock price.

Stock valuations are typically determined using a discounted cash flow (“DCF”) model, which makes assumptions about the future and produces the “intrinsic value” of the stock.

We know models with garbage-in assumptions based on distorted GAAP metrics only come out as garbage. Therefore, we use the current stock price with our Embedded Expectations Analysis to determine what returns the market expects.

At around $49 per stock, the market thinks the profitability in recent years will not be sustainable, and the Uniform ROA will go down to 48%.

Analysts, on the other hand, expect the next two years to be better than the last two, showing the disagreement between them and the market.

The market does not seem to be rewarding the company for its recent growth and extended license of its drug.

Investors put Harmony in the same basket as other pharmaceutical companies and punish it for the general uncertainty in the sector. But the company-specific details show us how resilient the business model is.

The market’s lack of understanding of the sustainability of its high returns, the company’s high growth, and low valuation means that Harmony Biosciences is a great candidate to be an FA Alpha 50 name.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up in investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies but rather on looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

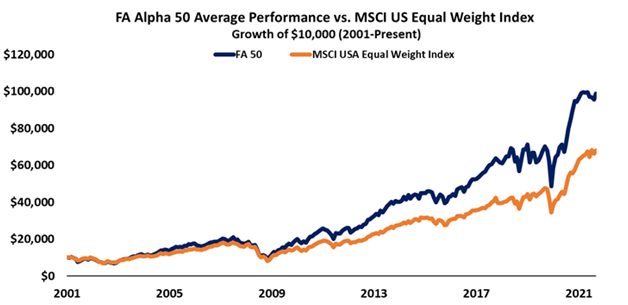

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To see the other 49 names on the list, click here.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research