The market is steering clear of this Chinese-owned browser

Cheap stocks often trade at low valuations for clear reasons and the majority of them don’t offer bargains.

Opera (OPRA) more than doubled its earnings last year, driven by a 63% jump in advertising revenue and a shift toward higher-value users, which lifted ARPU by 44% even as total MAUs fell.

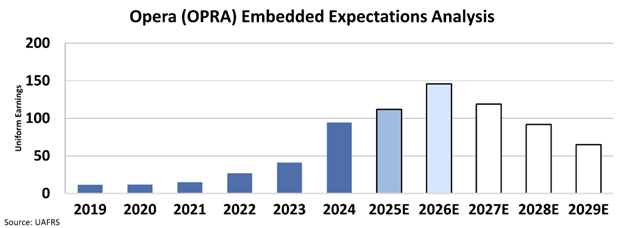

Despite these gains, Opera trades at cheap valuations, implying the market expects earnings to drop significantly instead of continuing to climb.

Persistent concerns about its Chinese ownership and data-privacy risks continue to dampen investor sentiment.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

When using our EEA tool, it’s easy to spot companies that look cheap at first glance. But often there’s a solid reason behind an apparently low price.

The EEA starts by looking at a company’s current stock price.

From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

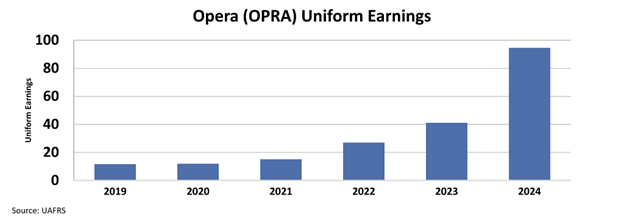

Opera (OPRA) has more than doubled its Uniform earnings from $41 million to $95 million last year.

A key driver of this performance has been advertising revenue, which grew by a staggering 63% year-over-year and now constitutes approximately 67% of total revenue.

This significant increase is attributed to a strategic shift towards “intent-based advertising,” allowing Opera to effectively connect users with advertisers through various channels within its browser.

Opera is doing this by refining its user base to enhance its Average Revenue Per User (ARPU) by concentrating on attracting and retaining users from more lucrative niche segments.

Instead of simply maximizing the total number of users, Opera is focusing its marketing and growth initiatives on demographics and regions that demonstrate a higher potential for revenue generation, especially younger users in Western markets.

Not all users contribute equally to revenue. By prioritizing individuals who are more likely to engage with revenue-generating features, the company managed to achieve a more efficient monetization of its user base.

While there has been a noticeable decline in the overall Monthly Active Users (MAU) figures, this has been accompanied by a significant increase in ARPU.

ARPU saw a 30% yearly growth from 2021 to 2024, and more recent figures show the trailing twelve months ARPU at $1.94, a year-over-year increase of 44%.

The growth in MAU from the Western market, which stood at 54 million with a 3 million year-over-year increase, has helped to counterbalance the reduction in total MAUs.

The proportion of these higher-value Western users within Opera’s total user base has also been increasing, reaching 18%, up from 10% in the first quarter of 2021.

Despite the strong results coming from the strategic shift, the market is pessimistic about Opera’s future earnings.

Currently, the company trades at an 11.2x Uniform P/E, which is far below compared to its peers and the corporate average.

At this level, the market expects Opera’s Uniform earnings to decline to $65 million from $95 million last year.

Concerns regarding the Chinese ownership of Opera have indeed been a recurring theme among investors and the market.

This issue adds a layer of complexity to the company’s investment profile, standing in contrast to its operational successes and otherwise attractive financial metrics.

Originally a Norwegian firm, Opera was acquired by a mix of Chinese investors in 2016.

Key entities involved included Kunlun Tech, a Beijing-based mobile games company and Qihoo 360, an internet security company.

Following this acquisition, Opera held an IPO on the Nasdaq in 2018.

Currently, Kunlun Tech, and by extension its controlling shareholder Zhou Yahui, who also serves as Opera’s Chairman and CEO, maintains an almost 70% controlling interest in the company.

Geopolitical tensions between China and Western countries often lead to increased scrutiny of Chinese-owned companies, especially those in the technology sector that handle user data.

There are persistent concerns about data privacy, security, and the potential for influence from the Chinese government.

These concerns can affect investor sentiment, irrespective of the company’s actual practices or its compliance with international regulations.

For a company like Opera, which develops web browsers and provides internet services, these data-related concerns can be particularly pronounced.

His ownership structure could make Opera a target for U.S. regulators, similar to other Chinese tech firms.

Allegations or even the perception of potential spyware or undue data access by Chinese entities can significantly impact user trust and, consequently, the company’s market valuation.

Opera has in the past had to counter claims regarding its data practices.

Furthermore, the association with Chinese ownership can cause concerns over corporate governance and the transparency of business operations, particularly regarding related-party transactions or strategic decisions that might prioritize the interests of the controlling shareholder.

For example, Hindenburg Research released a report in early 2020 that was critical of Opera, citing concerns related to its Chinese ownership.

While Opera has continued to operate and grow since then, such reports can leave a lasting impression on market perception.

Therefore, while Opera’s management might point to strong growth in advertising, strategic shifts towards higher ARPU users, and a healthy balance sheet, the “Chinese ownership” aspect remains a significant consideration for the market.

Investors should exercise caution with Chinese-owned firms, particularly those involved in distributing software and handling user data.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research