The market’s expectations for this clothing brand leave ample room for upside

Consumers cutting back is weighing on premium athletic apparel, yet Lululemon’s (LULU) focus on stylish, high‑quality seasonal updates has driven double‑digit revenue growth in 10 of the last 12 quarters and sustained high profitability.

With its North American market maturing, Lululemon is leaning into fast‑growing international markets and a still‑underleveraged menswear line to fuel future growth.

Despite these strengths, the market’s expectations imply the earnings will slip sharply, suggesting room for Lululemon to exceed those conservative projections.

Investor Essentials Daily:

Wednesday News-based update

Powered by Valens Research

Consumers are tightening their belts, and it’s hitting the athletic apparel industry hard.

Recent data shows U.S. financial optimism at its lowest since late 2023, with savings confidence dropping sharply.

Nearly half of Americans now feel worse about their financial health than they did six months ago.

For brands built on premium pricing, this trend spells trouble, with shoppers skipping $150 sneakers for cheaper alternatives or secondhand options.

However, not all athletic apparel companies are struggling…

Lululemon (LULU) has changed the way people dress for everyday workouts and leisure, and it continues to build on that strong foundation.

The company started by offering workout gear that was both stylish and comfortable, and over time, it became known for its quality and smart product updates.

Today, Lululemon remains a market leader by focusing on product development and growing its market share both at home and abroad.

The brand keeps its customers interested by introducing new products every season. This approach, called “seasonal newness,” means that shoppers always have fresh choices.

Lululemon listens to what its customers want and makes small changes to improve the style and function of its apparel.

This steady flow of new products helps keep the business strong even when the market becomes more competitive.

At home in North America, the market has become more mature, which makes growth a bit slower. However, Lululemon is not relying solely on its American customers.

The company has seen good results in international markets, especially in Asia. In countries like China, where the middle class is growing, there is a strong demand for high-quality athletic wear.

This international push helps balance the slower growth in the U.S. and gives the company a broader base of customers.

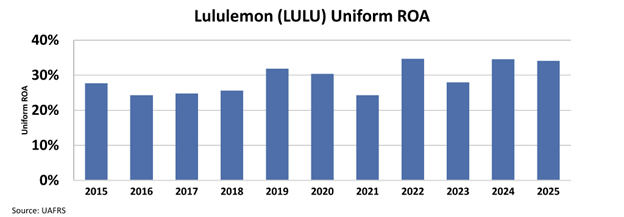

Recent earnings prove Lululemon’s strength, with double-digit growth in 10 quarters out of the last 12 quarters.

This performance resulted in the company achieving consistent Uniform return on assets (“ROA”) levels of around 30% since 2019, well above the corporate average.

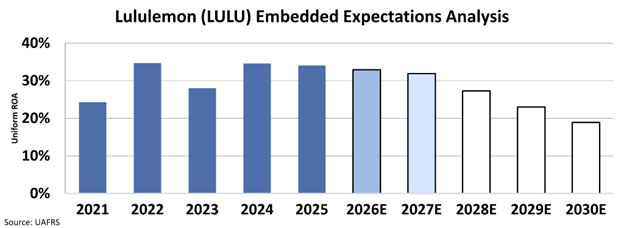

However, the market is quite pessimistic about this business, and they expect it to sustain its stable profitability for years to come.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market predicts that the company’s Uniform ROA will fall to around 19%.

Looking ahead, Lululemon’s growth story is shifting from domestic maturation to international expansion.

International markets currently account for only about 25% of total revenue but are growing at a formidable pace of nearly 20% annually, with China leading the charge with growth rates between 25% and 30%.

This provides a long and clear runway for future top-line growth as the brand continues to penetrate these relatively untapped markets.

Alongside geographic expansion, the menswear category presents another significant opportunity.

Representing just a quarter of total sales, the men’s line is growing steadily and has ample room to scale as Lululemon leverages its established brand equity to attract a loyal male customer base.

These two pillars, international and menswear, are poised to become primary drivers of value creation for the company and its investors.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research