Malibu Boats successfully rides the wave of the pandemic

It’s no secret to great investors that as-reported financial metrics are unreliable.

To be successful, these investors make adjustments to the financial statements to produce a true picture of economic reality, one that is otherwise obscured by arcane accounting principles. This allows them to find companies that exhibit three characteristics: high quality, strong growth potential, and low valuations.

Today, we highlight our FA Alpha screen, which emulates this investment strategy to produce outsized returns in excess of the market over long periods of time.

We’ll take a look at one company in particular on this month’s FA Alpha, describing how as-reported metrics distort economic reality and can lead investors to miss significant opportunities.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies, but rather looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

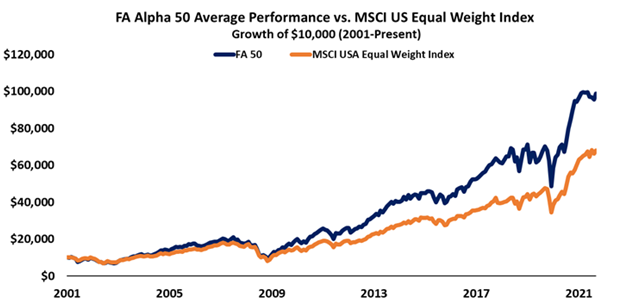

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

As the pandemic took over the world, it unlocked the At-Home Revolution.

When consumers couldn’t spend their money on experiences, they bought things. Traveling, dining, and going to the movies were no longer an option, so people turned to recreational sports like golfing, hunting, and boating.

Consumers looked for fun activities to do close to home, and having a boat or other fun toy seemed like a good idea. One of the big winners of this trend was Malibu Boats (MBUU), which offers a variety of boats under the brands of Malibu, Axis, Pursuit, Maverick, Cobia, Pathfinder, Hewes, and Cobalt.

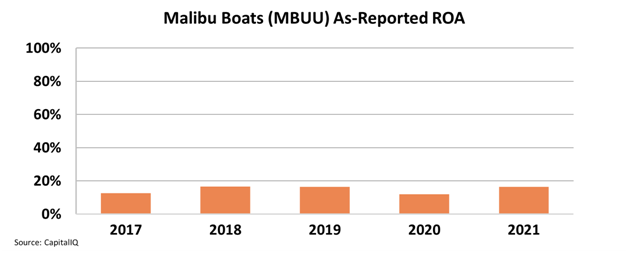

On an as-reported basis, it appears Malibu Boats was doing well, even before the pandemic, consistently generating a double-digit return on assets (ROA). It seems it was investing steadily ahead of the pandemic and again in 2021, positioning itself to make a healthy profit.

However, as-reported metrics fail to do Malibu Boats justice.

Uniform Accounting shows us that it was even more profitable than as-reported leads investors to believe.

ROA hasn’t just been above 10% (excluding 2020) for the past 5 years. It has been above 50%, with the exception of 2020, where it still reached an impressive 45% even amidst the pandemic where it was investing in further manufacturing facilities and experiencing supply chain bottlenecks.

While as-reported metrics make it look as though Malibu Boats doesn’t grow at all in 2020, Uniform Accounting shows us it has grown more than 20% for the last five years.

Even throughout the pandemic when demand was at a high, Malibu Boats made sure to position itself for strong growth so it can continue to excel even as the pandemic dies down.

People who have gotten hooked with their water toys keep coming back for more. Between this and the orders it is working through, Malibu Boats looks to be in a favorable position.

And yet the company trades at a below 10x Uniform P/E, as the market is overly pessimistic about the company’s future cash flows. The combination of impressively high returns, strong growth and low valuations is why it looks so compelling.

This high-quality market leader in its industry is inexpensively priced and growing aggressively, which is why our FA Alpha Screen discovered the name.

To see the other 49 names on the list, click here.

SUMMARY and Malibu Boats, Inc. Tearsheet

As the Uniform Accounting tearsheet for Malibu Boats, Inc. (MBUU:USA) highlights, the Uniform P/E trades at 9.6x, which is below the global corporate average of 24.0x, but around its historical P/E of 10.5x.

Low P/Es require low EPS growth to sustain them. In the case of Malibu Boats, the company has recently shown 9% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Malibu Boats’ Wall Street analyst-driven forecast is a 15% and 14% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Malibu Boats’ $67 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 9% annually over the next three years. What Wall Street analysts expect for Newmark’s earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power in 2020 is 10x above the long-run corporate average. Moreover, cash flows and cash on hand are 5x its total obligations—including debt maturities and capex maintenance. However, intrinsic credit risk is 150bps above the risk free rate.

All in all, this signals a moderate credit risk.

Lastly, Malibu Boats’ Uniform earnings growth is below its peer averages and is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research