Not So Royale with Cheese

It’s not surprising that Vincent Vega didn’t go to Burger King to find out what the Whopper was called in Pulp Fiction.

McDonald’s has long been the most ubiquitous of all the fast food chains, in the US and globally. This is why Vincent knew what a Quarter Pounder with Cheese was called in Europe, a Royale with Cheese, but did not know what a Whopper was called.

McDonald’s massive footprint means they have consistently struggled to grow the last 10 years. The company has grown restaurants by less than 2% a year the past 10 years, well below overall restaurant growth globally.

Because of this, the company has tried multiple initiatives to attempt to boost growth. The company has tried rolling out all-day breakfast. They have run multiple specials throughout the years, including periodically bringing back the McRib.

However, over the past 10 years, revenues for MCD have fallen more than 10%.

The company has been able to boost profits, as their efforts to franchise more and more stores have boosted profits by reducing their costs. They have similar revenue lines, but without the needed investment and operating costs, the company has seen Net Income rise from $4.3 billion to $5.9 billion over the past 10 years.

The company’s strong earnings growth has driven the company’s stock to triple the past 10 years.

But those franchising tailwinds have largely run out in the past few years, as the company’s potential to franchise more restaurants has expired. Less than 10% of the company’s stores are now company-owned, limiting the flexibility for the company to boost earnings through continuing this initiative.

And that was before the company’s CEO ran into ethical issues that may be leaving a company that already looked like it had stagnant growth even more rudderless.

The market doesn’t appear to be concerned about these issues. Even after the recent drop, the company is priced for all-time high returns. However, management is showing concerns about finding revenue growth, and their initiatives to improve the business. Considering slackening structural profit growth, management’s concerns about growth, and issues with senior management, there is reason to believe the market may need to continue to adjust expectations lower.

We’re Relaunching Our Portfolio Audit Review Offering – And Making A Special Offer

For our institutional clients, we don’t just provide access to our Valens Research app. We also do bespoke research. We produce one-off deep-dive company analyses using all our tools, including Uniform Accounting, credit work, and our management compensation and earnings call analysis. We monitor their portfolios for potential Uniform Accounting signals to alert them. We provide custom datasets for quantitative analysis, and provide aggregate analytics. We also help them create unique idea generation screens that are customized to their approach, using Uniform Accounting and our other analytics.

But for most of our institutional clients, the analysis that they find most useful, and almost universally ask for, is a quarterly portfolio audit and call with our analysts.

Our institutional clients pay a significant premium for all our bespoke research. Some of our institutional clients have paid well over $100,000 a year for our uniquely tailored Uniform Accounting research, because of the value it adds to their process.

Until Thanksgiving, we’re making a special offer.

For any investor that buys access to the Valens Research app ($10,000/year subscription), we will include an Institutional-level portfolio audit and call with our analyst team with no extra charge.

Also, for those people who sign up to the offer before end of day on November 15th, we’ll include one year of access to all of our newsletters, including our Market Phase Cycle™ and Conviction Long Idea List (a $6,000 value), for no extra charge.

We want to help show you how powerful Uniform Accounting research can be for your investment strategy.

If you want to hear more about this offer, or are interested in subscribing, feel free to reply to this email. I’ll forward your note to our head of client servicing. Or, feel free to reach out to Doug Haddad, the head of our client relations team, at doug.haddad@valens-securities.com or at 630-841-0683.

To read more about the offer and sign up, you can also click here.

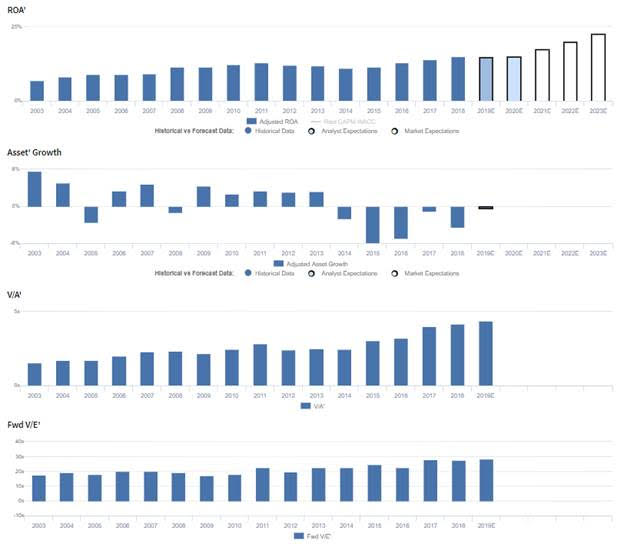

Market expectations are for record-high Uniform ROA, but management may be concerned about growth, innovation, and EOTF implementation

MCD currently trades at historical highs relative to UAFRS-based (Uniform) Earnings, with a 28.4x Uniform P/E. At these levels, the market is pricing in expectations for Uniform ROA to expand from 15% in 2018 to a peak of 23% in 2023, accompanied by immaterial Uniform Asset growth going forward.

However, analysts have less bullish expectations, projecting Uniform ROA to sustain 15% growth through 2020, accompanied by 1% Uniform Asset shrinkage.

Historically, MCD had seen relatively steady improvements in profitability, with Uniform ROA increasing from 7% in 2003 to 13% in 2011. However, Uniform ROA then gradually faded to 11% in 2014, before expanding to historical highs of 15% in 2018. Meanwhile, prior to 2013, MCD had grown its Uniform Asset base annually by 3%-8%, excluding shrinkage in 2005 and 2008. However, the firm has shrunk its Uniform Asset base in each of the past five years by 1%-7%, as they have sold off various underperforming international assets and moved to a franchising model to help improve capital efficiency and profitability.

Performance Drivers – Sales, Margins, and Turns

Improvements in Uniform ROA have been driven by expanding Uniform Earnings Margin, which grew from 13% to 22% between 2003 and 2010, before stabilizing at 20%-22% levels through 2015, and rising to peak levels of 31% in 2018. Meanwhile, Uniform Asset Turns have consistently ranged from 0.5x-0.6x since 2003. At current valuations, markets are pricing in expectations for the firm to continue divesting underperforming assets and expanding growth in its franchises, driving further improvements in Uniform Margins, coupled with expansion in Uniform Turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q3 2019 earnings call highlights that management is confident plant-based burger sales in Ontario reflect North American demand. However, they may lack confidence in their ability to drive franchise growth, and they may be concerned about the sustainability of McDelivery sales growth. Furthermore, they may lack confidence in their ability to sustain innovation, and they may be concerned about resistance to simplifying their menu. Finally, they may be concerned about the sustainability of franchise margin dollar growth, and they may be concerned about the rate of EOTF implementation.

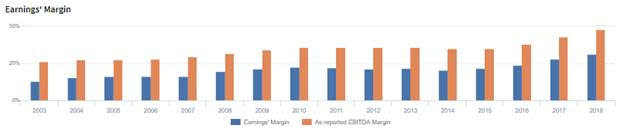

Uniform Accounting metrics also highlight a significantly different fundamental picture for MCD than as-reported metrics reflect. As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly overstate MCD’s margins. For example, as-reported EBITDA margin for MCD was 48% in 2018, substantially higher than Uniform Earnings Margin of 31%, making MCD appear to be a much stronger business than real economic metrics highlight. Moreover, as-reported EBITDA margin has been 1.5x-2.0x higher than Uniform Margin in each year since 2003, distorting the market’s perception of the firm’s profitability ceiling for over a decade.

Today’s Tearsheet

Today’s tearsheet is for Merck. Merck trades at a discount to market valuations. At current valuations, the market is pricing in Uniform EPS to barely grow, while the company is actually forecast to have EPS grow massively the next two years. The company’s earnings growth is at the high end of peers, while the company is trading at average valuations relative to peers. The company has healthy profitability and no risk to their solid dividend yield.

Regards,

Joel Litman

Chief Investment Strategist