Moody’s has gotten this company wrong for twenty years. They’re still massively overstating its credit risk, this time for a new reason

This company is considered a “moderate credit risk” by Moody’s. In their own words, it’s because of “(near-term) uncertainty around obligations”. But Moody’s has said the same thing about the company for 20 years, and looking at their cash flows, it’s hard to argue “moderate risk” is a fair assessment.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The CDC considers it an epidemic now.

It started in the early 90s with the first wave of opioid-related deaths. It evolved as manufacturers sold more and more pills with claims that the risk of addiction was low.

Drugs such as HUMIRA, SOVALDI, and Enbrel generate billions of dollars of revenue annually for the firms that created them. Their respective developers, Abbvie, Gilead, and Amgen, have even become household names. Moreover, their stocks have experienced meteoric rises as a result of their launches.

However, the development and launch of new treatments is long and hard.

Deaths have reached new highs as the crisis has evolved.

And now, there is a push to hold those responsible for it accountable. A massive legal battle has been brewing. The biggest cases include names like Purdue, who manufactured OxyContin, as well as names like CVS and Albertsons, for varying degrees of their role.

One of those companies that will likely be paying is McKesson. McKesson is one of three distributors of drugs, along with AmerisourceBergen and Cardinal Health.

These companies facilitated the drugs making it to customers and profited from the high volumes of opioids. The three companies are reported to be possibly approaching a settlement deal.

This deal would have them collectively paying $18bn over the next 18 years. Roughly $6bn would be McKesson’s share if split evenly.

In fact, the ratings agency Moody’s says “The comprehensive proposed opioid settlement would result in McKesson paying $6.86 billion of cash over 18 years”. They then add, “the company would also be responsible for providing product distribution and monitoring services over a 10-year period, valued at an additional $1.14 billion.”

If this settlement is reached, Moody’s research suggests roughly $500mn in annual payments for McKesson over the next few years. Even by Moody’s account in that same report, McKesson should have no issue servicing this payment.

However, Moody’s just reaffirmed McKesson’s rating as a Baa2. The same credit rating Moody’s has given McKesson for the past 20 years.

Their documentation says companies with this rating “are judged to be…subject to moderate default risk.”

The reason for a “moderate risk” even though McKesson has the cash flow to service obligations is “uncertainty as to whether this settlement will be finalized.”

Rather than come to a firm conclusion based on the actual cash flows of the company, Moody’s knocked them for “uncertainty”.

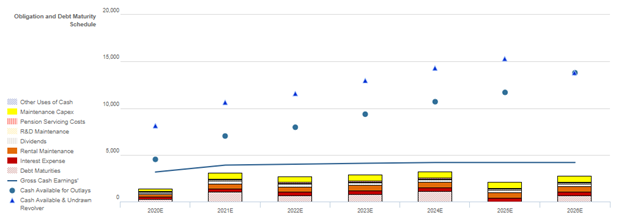

To reduce “uncertainty”, we looked at McKesson’s obligations and capital structure. The company has several billion dollars in cash, so they already have a buffer for when a settlement is finalized.

Second, when you clean up the accounting, the company is projected to have $1 billion to $2 billion in cash flows each year over all obligations other than settlement cash flows over the foreseeable future. If they were to reduce dividends, this number jumps even further.

Even if the settlement ends up three times higher than what is currently being discussed, McKesson should have little issue servicing that, and operations, and keep paying a dividend.

Moody’s says McKesson is a “moderate default risk” because of “uncertainty” in their business.

But using Uniform Accounting we can see why investors don’t seem to care about Moody’s Baa2 rating, and is pricing McKesson much safer, in line with Valens’ IG3- rating.

When investors pay more attention to economic reality as opposed to Moody’s distorted as-reported accounting analysis, they get a better understanding of where credit risk is heading.

Ratings Improvement Likely as MCK’s Robust Cash Flows Continue to be Overlooked

Credit markets are slightly overstating MCK’s credit risk with a YTW of 2.439% and a CDS of 85bps, relative to an Intrinsic YTW of 1.799% and an Intrinsic CDS of 16bps.

Fundamental analysis highlights that MCK’s cash flows should exceed operating obligations in each year going forward. In addition, the firm’s cash flows alone should be sufficient to service all obligations including debt maturities through 2026.

Furthermore, despite their nonexistent recovery rate, the firm has a sizable market capitalization and strong Uniform ROA levels, which would likely allow access to credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for creditors.

MCK’s management compensation framework should drive them to focus on all three value drivers: revenue growth, margins, and asset turnover, which should lead to Uniform ROA improvement and higher cash flows available for servicing obligations.

Furthermore, management members have low change-in-control compensation, indicating they are not likely to seek or accept a buyout or takeover, limiting event risk for credit holders.

However, none of the company’s NEOs are material owners of equity, indicating they might not be aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (10/30) highlights that management is confident they help independent pharmacists stay independent.

However, they may lack confidence in their ability to meet their EPS guidance, and they may be concerned about their positioning and outlook.

Furthermore, they may be concerned about the strength of the pharmacy market and their decision to exit from their stake in Change healthcare. Finally, they may lack confidence in their ability to drive European revenue growth and to improve EBIT and revenue.

MCK’s robust cash flows, expected cash build, and sizable market capitalization indicate that Moody’s and credit markets are overstating credit risk. As such, a tightening of credit spreads and a ratings improvement are likely going forward.

SUMMARY and McKesson Corporation Tearsheet

As the Uniform Accounting tearsheet for McKesson Corporation (MCK) highlights, the company’s Uniform P/E trades at 13x, which is below global average valuation levels and is in line with previous period valuation levels.

Low P/Es require low—or even negative—EPS growth to sustain them. That said, in the case of MCK, the company has recently shown 27% Uniform EPS growth, significantly above what is required.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, MCK’s Wall Street analyst-driven EPS growth forecast flipped from positive to negative.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $156 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for MCK, the company would have to have Uniform earnings shrink by -9% each year over the next three years.

What Wall Street analysts’ expectations for MCK’s earnings growth are below what the current stock market valuation requires in 2020, but is far above the requirement in 2021.

In addition to MCK’s valuations being low, its Uniform P/E and Uniform EPS growth are both below peer averages.

Meanwhile, the company’s earnings power is 4x higher than corporate averages, signaling very low risk to its dividend or operations.

To summarize, McKesson Corporation is seeing above average Uniform earnings growth, which is not expected to continue in 2020. Furthermore, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research